Next week’s key economic developments will centre on policy decisions from the US Federal Reserve, the Bank of England and the Bank of Japan, alongside a series of data releases from China and several emerging markets. According to the latest S&P Global Economics Commentary, central banks are widely expected to hold rates steady, with headline inflation showing signs of easing. However, diverging growth trajectories and policy responses are likely to remain a defining theme through the second half of 2025.

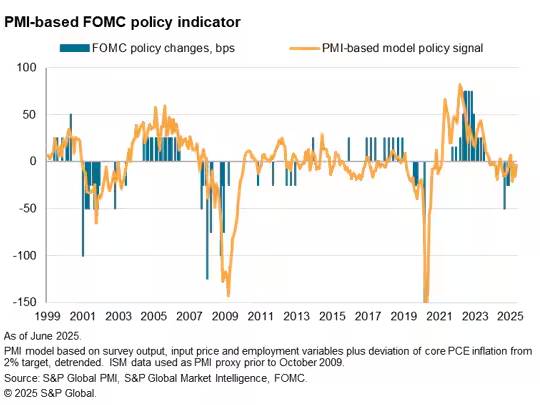

Fed expected to hold as markets watch for late-2025 cuts

The Federal Open Market Committee (FOMC) is expected to keep interest rates unchanged at its meeting next week. While May’s US CPI data surprised the downside, core inflation remains above target. Markets continue to price in a potential rate cut by Q4 2025, but S&P analysts note that any policy easing will remain contingent on sustained disinflation and labour market softening.

New US tariffs on Chinese imports, recently announced by President Biden, are expected to add fresh supply-side cost pressures, complicating the Fed’s outlook and delaying any near-term pivot.

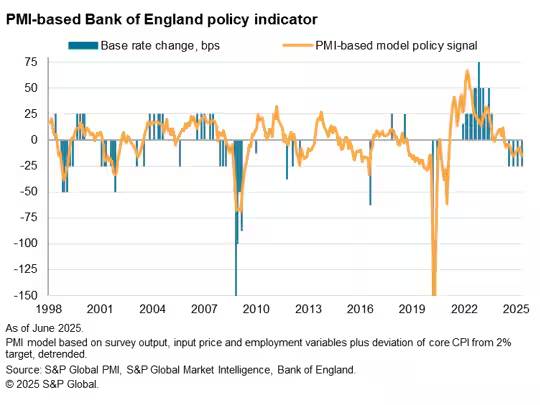

Bank of England likely to maintain hold ahead of CPI data

The Bank of England is also expected to keep rates on hold following its rate cut in May. Policymakers are watching services inflation closely ahead of new CPI data due next week. According to S&P, the BoE may consider further easing in August or November, depending on the persistence of inflation and wage dynamics.

With the UK economy showing limited momentum, the central bank will face pressure to balance inflation control with the need to support weak demand.

BoJ seen holding amid yen weakness and slow growth

The Bank of Japan is likely to maintain its current policy stance amid continued yen depreciation and slowing economic activity. Japan’s Q1 GDP contracted, and manufacturing PMI data has softened, pointing to declining export demand. While inflation is approaching the BoJ’s 2% target, the weak currency and external risks could delay any tightening until late 2025.

S&P highlights the dual challenge of currency stabilisation and policy credibility as central concerns for the BoJ in the coming quarters.

China data to signal direction of policy support

A wave of high-frequency data from China is due next week, including industrial output, retail sales, and unemployment figures. While services activity remains resilient, manufacturing continues to show weakness, driven by softer export demand and the impact of US tariffs.

S&P expects the People’s Bank of China to consider increased policy support in the second half of 2025 if consumption fails to rebound meaningfully.

EM central banks set to hold rates as inflation persists

Policy meetings are also scheduled next week in Brazil, Switzerland, Sweden, Indonesia, the Philippines and Taiwan. Most are expected to leave rates unchanged. In Brazil, persistent inflation and subdued growth reduce the likelihood of further easing.

Across emerging markets, soft manufacturing PMIs and rising input costs continue to squeeze production margins and limit monetary policy flexibility.

Key indicators to watch

- US: FOMC decision, retail sales, industrial production

- UK: BoE decision, labour market figures

- Japan: BoJ decision, exports, core inflation

- China: Retail sales, industrial production, unemployment

- Brazil: Selic rate decision, IPCA inflation

- Indonesia and Philippines: Rate decisions, trade and remittances

Policy to fragment further in H2

According to S&P Global Economics Commentary, inflation is easing across advanced economies, but structural risks, such as tariff shocks, political transitions, and fiscal tightening, will continue to weigh on global growth. Central banks are expected to remain cautious, guided by incoming data rather than forward guidance.

As G7 and emerging economies move along increasingly divergent paths, monetary policy fragmentation is likely to deepen across the remainder of 2025.