Tokenisation of real-world assets (RWA) could redefine global capital markets, capturing up to 10% of the world’s financial assets, or $867 trillion, by 2050, according to a joint report from crypto exchange OKX and Blockworks. This projection suggests tokenisation is entering a long-term structural phase, beyond early-stage hype cycles and experimental pilots.

The report, which analysed 40 real-world asset tokenisation projects across capital markets, funds, lending, and payments, outlines how tokenised instruments could migrate $13 trillion in value on-chain over the next five years. That includes $2.3 trillion in tokenised short-term treasuries and $2 trillion in stablecoins. While this would still represent less than 1.5% of the $867 trillion global total, analysts see it as a foundational shift toward programmable financial infrastructure.

Next 5 years

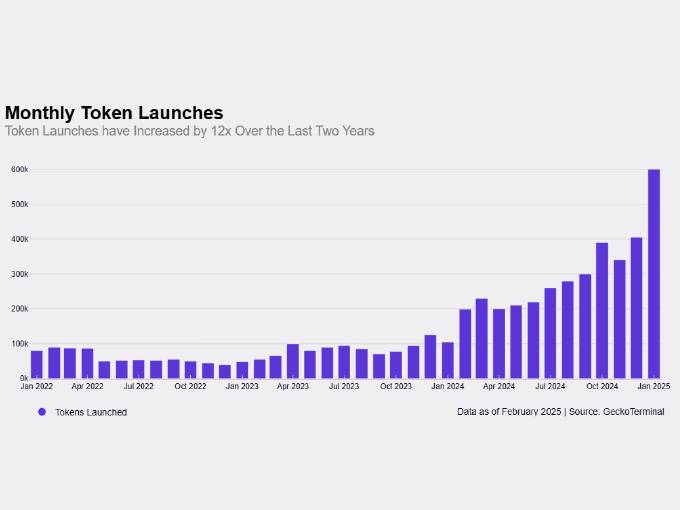

The near-term focus is expected to remain on liquid, low-risk instruments, particularly US Treasury bills, private credit, and fiat-backed stablecoins. Since 2023, tokenised US T-bills have surged 1,000% to $1.29 billion, led by players like Franklin Templeton, Ondo, and OpenEden. Meanwhile, tokenised private credit volumes grew 128% year-on-year, outpacing other sectors.

Stablecoins remain the largest segment of the on-chain RWA ecosystem, with a circulating supply of over $160 billion as of April 2024. These tokens are increasingly used not only in decentralised finance (DeFi) but also by emerging market businesses for cross-border transactions and by fintech platforms for remittance and e-commerce.

Tokenisation unlocks infrastructure efficiency

Beyond asset digitisation, the report highlights how tokenisation enables programmable compliance, 24/7 settlement, and atomic clearing. This shift allows for reduction in intermediaries, instant auditability, and streamlined corporate actions. In lending, on-chain RWAs are powering decentralised credit pools and collateralised debt obligations that operate globally and natively on blockchain.

For institutional adoption to scale, infrastructure standardisation remains critical. While public blockchains offer cost efficiency and global access, enterprise adoption is more likely to begin with permissioned networks and hybrid models. Leading protocols such as Centrifuge, Clearpool, and Maple are already offering institutions tools to access real-world yields while maintaining compliance frameworks.

Jurisdictional arbitrage and regulation as catalysts

The report notes that the tokenisation ecosystem is being shaped by regulatory clarity, or lack thereof. Jurisdictions like the UAE, Singapore, and Hong Kong are emerging as early leaders, offering sandbox regimes and regulatory frameworks tailored for digital assets. Meanwhile, slow progress in US policy continues to be a barrier for wider institutional adoption.

In markets with regulatory clarity, new products are emerging, including tokenised money market funds, synthetic fiat currencies, and stable-value funds that mirror traditional instruments but operate on-chain. Platforms like JPMorgan’s Onyx and BlackRock’s BUIDL fund are cited as early examples of how traditional finance is experimenting with blockchain rails.

Over the next 25 years, tokenisation is expected to reshape global asset management and transaction settlement. From public equities and real estate to art and carbon credits, virtually all asset classes are expected to see tokenised formats. According to the report, the long-term bet is not just on asset digitisation but on transforming capital formation, governance, and financial access through programmable finance.