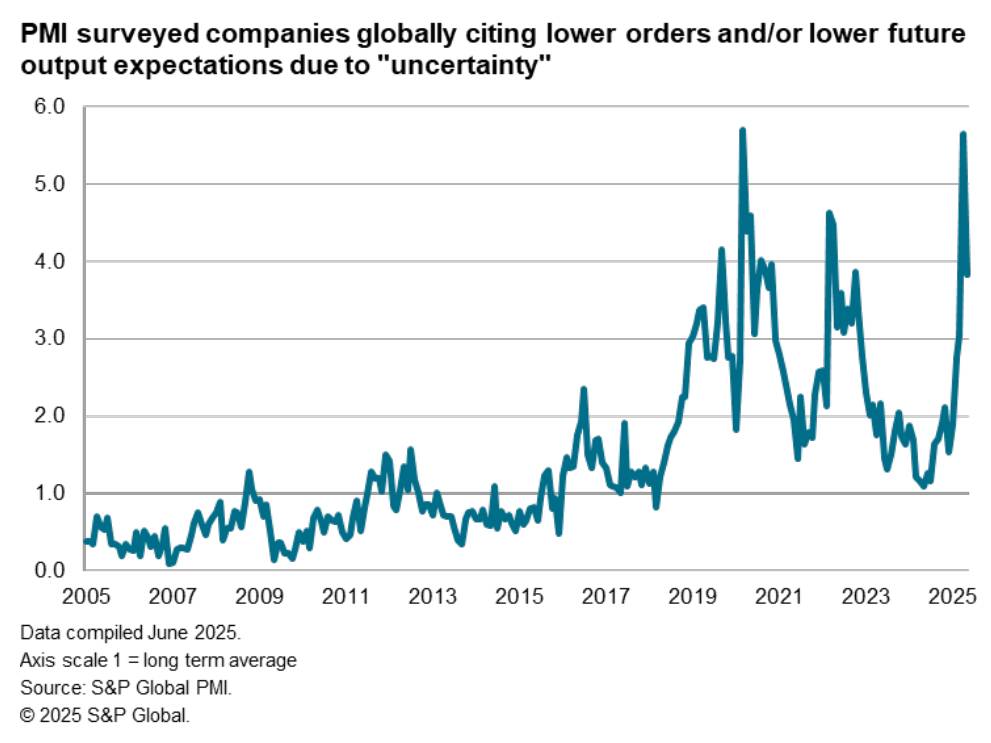

Global business sentiment will be under close scrutiny next week as flash PMI surveys are released for the US, eurozone, UK, Japan, Australia, and India. According to the latest S&P Global Economics Commentary, the data will offer a preliminary view of economic conditions in June, at a time when tariff-related uncertainty and rising geopolitical tensions have contributed to a volatile macro backdrop.

PMI figures for May had signalled a modest recovery in both current output and forward-looking expectations, mainly due to the temporary pause in US tariff hikes introduced in April. However, with those tariff suspensions due to expire in early July and with Brent crude up nearly 10% month-on-month, markets are looking to next week’s data to determine if April marked the low point for global business confidence or merely a pause in a broader downturn.

Policy uncertainty builds

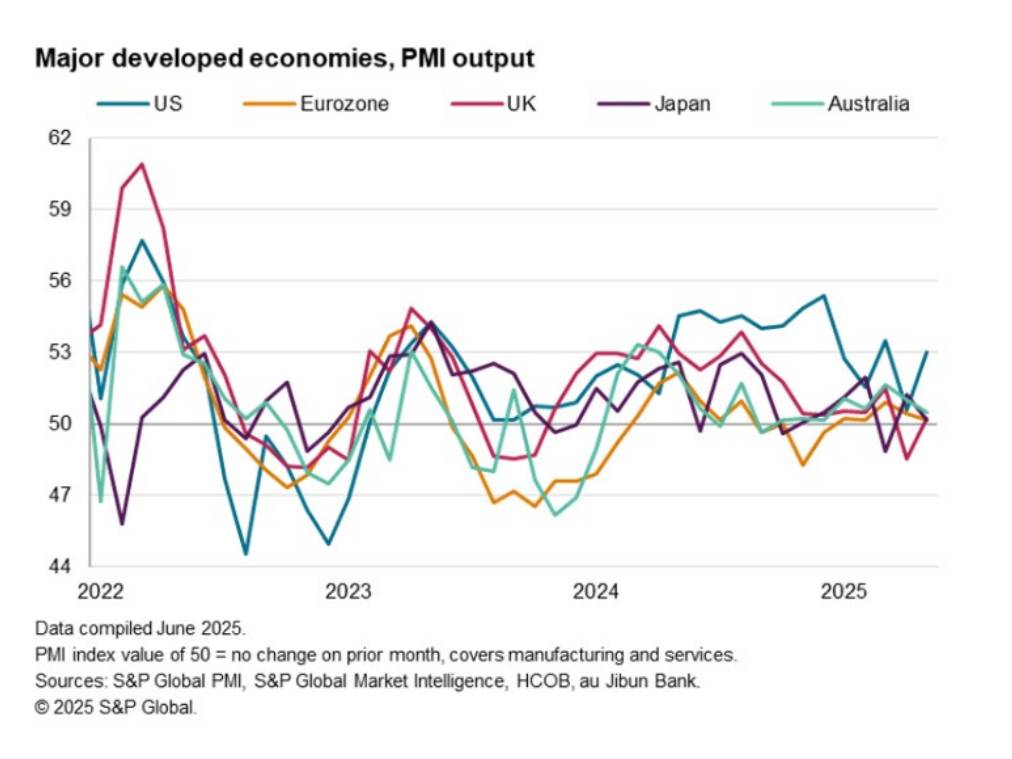

S&P expects the US flash PMI will be watched for further divergence between services and manufacturing. May data showed strong growth in services, but manufacturing output was under pressure from rising input costs. New tariffs and a potential resumption of higher levies on Chinese goods could distort near-term sentiment.

In the eurozone, German manufacturing may benefit from anticipated fiscal expansion, while recent fluctuations will test broader regional sentiment in oil prices. The UK’s PMI data will be assessed for early signs of economic impact from April’s tax increases and the recently concluded US-UK trade deal. Q1 GDP and current account data, due later in the week, will provide further details on underlying demand.

APAC data to gauge trade fragility

Japan’s au Jibun Bank PMI, as well as employment and retail data, will provide further insight into the economy’s weak performance in Q1. The Bank of Japan’s summary of opinions from its June meeting, also due next week, will be reviewed for signs of concern around yen depreciation and limited export growth.

India’s HSBC flash PMI will provide one of the earliest snapshots of South Asia’s economic momentum for June. Industrial production in Taiwan and Singapore will also be monitored as manufacturers contend with falling new orders and slowing global trade.

US inflation, spending, and confidence data to shape Fed expectations

Beyond the PMI figures, markets will closely follow the US core PCE price index, durable goods orders, and personal spending and income data for May. While core CPI for May had surprised to the downside, the PCE index is expected to confirm that disinflation remains gradual. Consumer sentiment reports from the Conference Board and University of Michigan will also be released, alongside trade and housing market data.

Canada will publish its inflation data, with policymakers likely to track cost pressures linked to cross-border trade and tariffs. The S&P Global Canada PMI has already highlighted input price pressures in the past month.

Europe’s inflation path in focus

France and Spain will release preliminary June inflation data at the end of the week, with flash PMIs expected to preview broader price trends. Germany’s Ifo Business Climate and GfK Consumer Confidence reports will shed light on sentiment ahead of Q3. In the UK, final Q1 GDP and current account figures are scheduled for release on Friday.

EM central banks watch inflation, hold policy

Thailand’s central bank meets next week, with analysts expecting a dovish tone following two recent rate cuts. Inflation reports are also expected from Singapore and Malaysia, while Mexico’s central bank is set to announce its policy decision on Thursday amid ongoing concerns over core inflation and weak industrial growth.

While PMIs may show isolated pockets of resilience, particularly in US services and Southeast Asian exports, S&P noted that the global business sentiment remains constrained by uncertainty around trade policy, oil prices, and geopolitics. The coming week’s data will be critical in gauging whether firms are preparing for stabilisation or further deterioration into Q3.