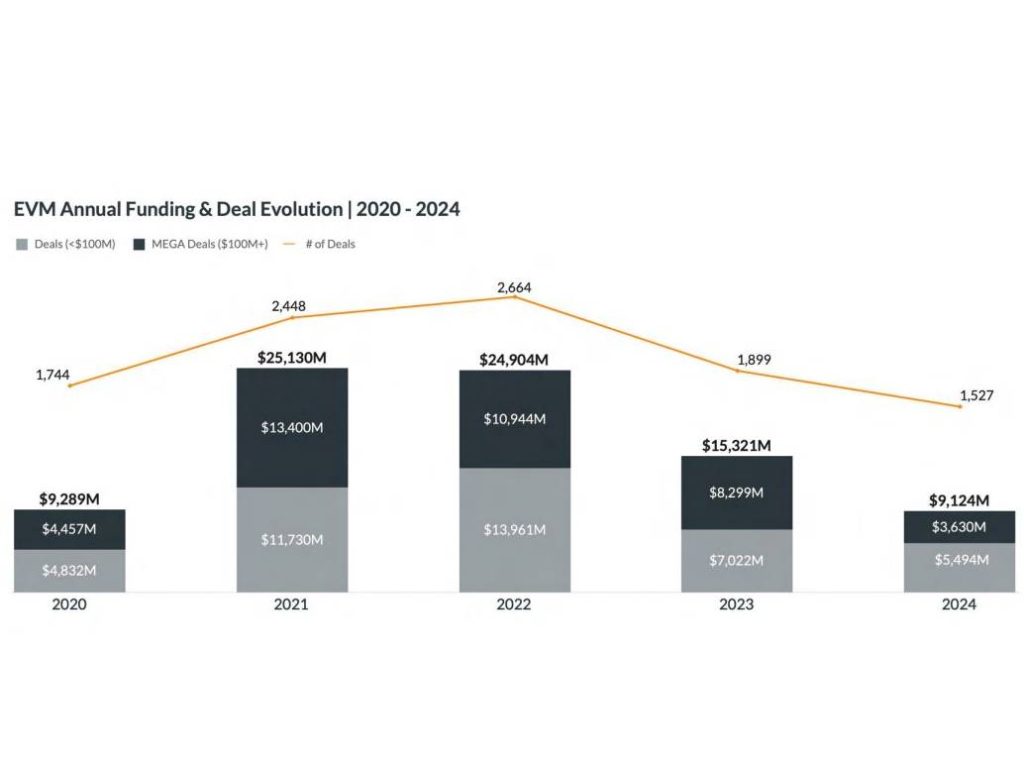

The Emerging Venture Markets (EVM) spanning the Middle East, Africa, Southeast Asia, Türkiye, and Pakistan faced a turbulent year in 2024, with total funding plummeting by 40% to $9.1 billion compared to 2023, according to MAGNiTT’s FY2024 Venture Investment Summary. The total number of deals fell by 20% to 1,527, reflecting the lowest levels recorded since the pre-pandemic period in 2020. This sharp contraction is in line with global trends, as venture capital markets worldwide grapple with rising interest rates, geopolitical tensions and cautious investor sentiment that curbed late-stage funding.

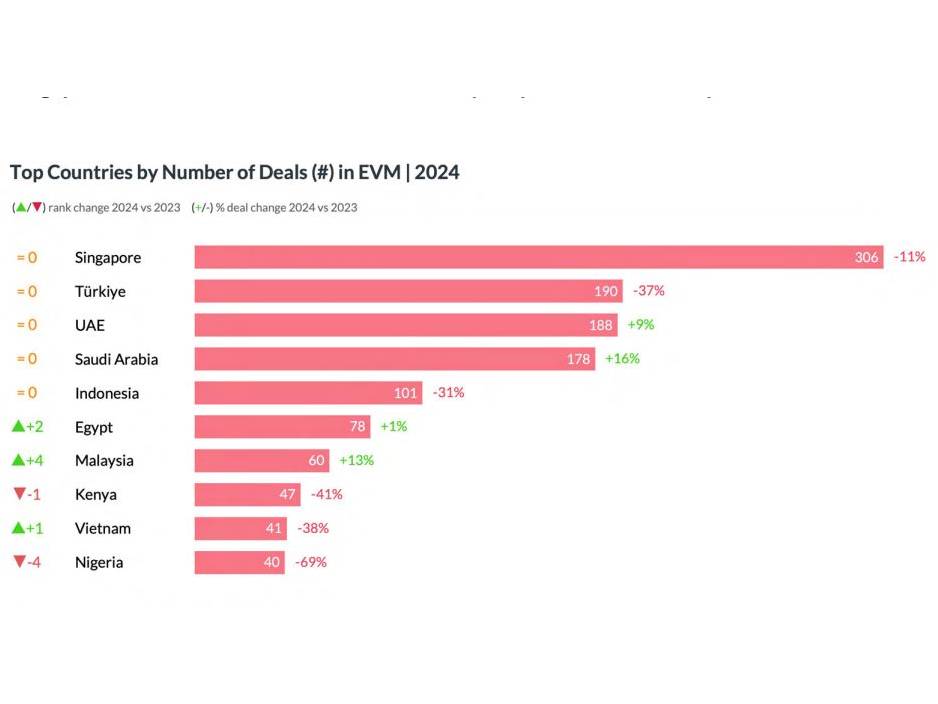

Southeast Asia remained the most active region in the EVM landscape, accounting for 43% of the total activity. However, funding in the region shrank by 45% to $5.6 billion, with the number of deals falling by 14% to 564. Singapore, the region’s most significant player, witnessed a 53% decline in funding to $3.4 billion. Meanwhile, the Middle East showed relative resilience, with funding declining 29% to $1.5 billion but deal activity rising by 10% to 461. The UAE led the region in the number of deals (188), though Saudi Arabia secured the highest funding at $750 million, despite a 44% drop year-on-year.

Africa, by contrast, recorded the steepest drop in performance, with total funding down 44% to $1.07 billion and deal volume plunging by 39% to 294. Egypt emerged as the continent’s top recipient of venture funding, securing $329 million, though this marked a 21% decline compared to the previous year.

Fintech’s continued dominance

Fintech remained the dominant sector across EVMs, attracting $3.98 billion across 322 deals. However, this represented a 7% decline in funding and a 20% drop in deal count. The performance varied significantly across regions—Southeast Asia, for instance, recorded a 39% increase in fintech funding, signalling sustained investor interest in digital financial services amid economic headwinds.

In contrast, the e-commerce and retail sectors saw a dramatic contraction, with funding levels collapsing by 81% year-on-year. Yet, in the Middle East, these sectors maintained relevance due to notable deals, such as investments in platforms like SallaApp and eyewa.

Funding dynamics

One of the most notable trends of 2024 was the continued decline in large late-stage deals, with “mega-deals” (those valued at over $100 million) down by 56% compared to 2023. Late-stage funding was disproportionately affected by the tightening of global liquidity. Meanwhile, early-stage funding rounds—particularly those between $1 million and $5 million—saw increased activity, indicating a shift in investor strategy towards nurturing nascent startups.

This shift highlights a broader recalibration in investor priorities, as early-stage investments are often seen as a hedge against the high valuations and risks associated with later-stage funding in uncertain markets.

Exits and liquidity

Exits across EVMs fell for the second consecutive year, dropping by 32% to 94 in 2024. Southeast Asia experienced the steepest decline, with exits falling by 35%, while the Middle East increased its share of exits to 30%, its highest proportion in four years. The median time to exit in the Middle East also improved, dropping from 7.4 years in 2023 to 6.2 years in 2024.

This reduction in exit timelines suggests that Middle Eastern startups are securing quicker routes to liquidity, although the overall number of exits remains subdued due to broader macroeconomic challenges.

Top performers

Among the notable country performances, the Philippines recorded the largest deal of the year—a $786 million investment in Mynt, driven by backers including MUFG Bank and Ayala Corporation. This deal contributed to a 721% year-on-year increase in funding for the country, making it a significant outlier in an otherwise bearish market.

Türkiye also secured a landmark transaction with a $500 million investment in Insider, an advertising technology firm. This deal was pivotal for the region’s overall performance and reinforced the appetite for high-growth tech investments despite tightening global conditions.

While the venture capital ecosystem across EVMs has faced a significant correction, early-stage investments remain critical for potential recovery. However, macroeconomic pressures, including inflation and rising borrowing costs, will likely persist in 2025, making it challenging for late-stage startups to raise funds.

Investor sentiment remains cautious, but there are pockets of optimism tied to high-growth sectors such as fintech, enterprise software, and artificial intelligence. The evolution of these markets will largely depend on regional policy decisions, geopolitical developments, and the stabilisation of global financial markets.

The report stresses the importance of targeted investments and the need for adaptability in the face of evolving market conditions. As funding flows adjust to the realities of 2024, the recovery of EVMs will hinge on the resilience of key industries and the ability of startups to leverage early-stage capital efficiently.