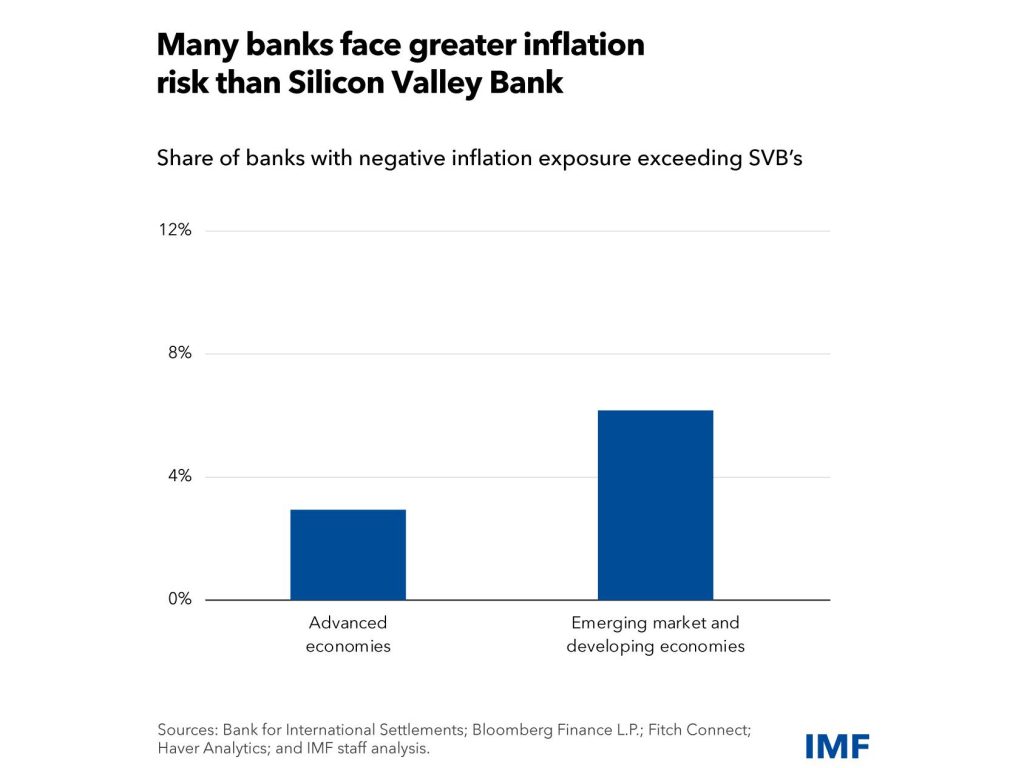

The International Monetary Fund (IMF) has warned that rising interest rates could destabilise banks, with 3% of lenders in advanced economies and 6% in emerging markets facing significant financial risks. The findings, published in an IMF blog post, highlight central banks’ challenges in balancing inflation control with financial stability.

Banks and inflation exposure

The IMF research analysed data from 6,600 banks across nearly three decades and found that most financial institutions are structurally hedged against inflation. Their income and expenses adjust with inflation, largely insulating them from its direct impact. However, some banks remain vulnerable due to their business models and risk management practices.

These exposures become particularly dangerous when inflation forces central banks to raise interest rates rapidly. When rates increase, the value of long-term securities held by banks declines, eroding capital buffers. This risk materialised in 2023 when Silicon Valley Bank (SVB) collapsed after its bond-heavy portfolio lost value as the Federal Reserve hiked rates. The bank’s failure triggered broader panic, prompting emergency regulatory measures to contain the fallout.

The IMF found that a similar proportion of banks in both advanced and emerging markets are as vulnerable to interest rate shocks as SVB was before its collapse. In emerging economies, the risks are further amplified by direct inflationary exposure, often due to more frequent price indexation in loan and deposit contracts.

Financial stability vs. inflation control

The IMF findings pose a dilemma for policymakers. Raising interest rates remains the primary tool for curbing inflation, yet aggressive hikes could weaken some banks, triggering instability. Financial contagion could spread if depositors lose confidence in vulnerable institutions, as seen in previous banking crises.

Central banks must now assess whether continued tightening of monetary policy could pose systemic risks. The failure of SVB, followed by the forced takeover of Credit Suisse in 2023, revealed weaknesses in liquidity and risk management across the sector. The speed at which depositors withdrew funds, amplified by digital banking and social media, made traditional crisis-management tools less effective.

A key challenge for regulators is ensuring that monetary policy does not unintentionally push already vulnerable banks into distress. The IMF suggests that financial stability considerations should be incorporated into interest rate decisions. However, this approach introduces trade-offs: easing up on rate hikes to protect banks risks prolonging inflation, while tightening too aggressively could lead to bank runs.

The role of regulation

To mitigate risks, the IMF recommends strengthening banking supervision and regulation. This includes:

- More rigorous stress testing to identify banks that are highly exposed to inflation and interest rate hikes.

- Enhanced capital and liquidity buffers for institutions carrying large portfolios of fixed-income securities.

- Better transparency in risk disclosures to help markets differentiate between strong and weak banks.

- Granular risk assessments that consider different business models, funding structures, and regional economic conditions.

The IMF’s recommendations align with the Basel Committee on Banking Supervision calls, which has urged regulators to update global liquidity rules in response to recent bank failures. These failures exposed weaknesses in how banks hedge interest rate risks and manage deposit volatility.

The speed at which recent crises unfolded suggests that regulatory frameworks must evolve. Unlike previous banking failures, which developed over weeks or months, the SVB crisis escalated within days as depositors withdrew billions through online transfers. Traditional tools such as deposit insurance and emergency liquidity measures struggled to keep pace with the rapid spread of panic.

Lessons from recent bank failures

The IMF’s analysis places recent banking turmoil in a broader historical context. While the 2008 financial crisis was driven by credit risk and subprime lending, the current challenges stem from interest rate risk and deposit flight. The collapse of SVB and other regional banks in 2023 highlighted how well-capitalised institutions can struggle if their assets lose value too quickly.

One key lesson is the need for proactive regulatory intervention. The IMF suggests supervisors should closely monitor banks’ exposure to interest rate risk and intervene before market stress escalates. This could involve stricter limits on long-duration asset holdings, mandatory hedging strategies, or targeted liquidity support for institutions showing early signs of distress.

Another lesson is the growing influence of digital banking and real-time information flow. Social media-fuelled bank runs, such as the one that hit SVB, highlight the importance of monitoring depositor sentiment and adapting crisis-response mechanisms to faster-moving financial markets.

What comes next?

The IMF’s findings will be discussed at the IMF/World Bank Spring Meetings in April, where policymakers will weigh the risks of continued monetary tightening against the need for financial stability. With inflation still above target in many economies, central banks face difficult choices in the months ahead.

For financial institutions, the focus will be on shoring up risk management practices. Banks with heavy exposure to long-term assets or weak liquidity positions may face further pressure as rates stay elevated. Investors and depositors, meanwhile, are likely to scrutinise bank balance sheets more closely, increasing the risk of capital flight from institutions perceived as vulnerable.

Policymakers will need to navigate these risks carefully. A misstep—whether in monetary policy or regulatory oversight—could trigger further instability, undoing progress made in stabilising inflation and financial markets.