Private equity dealmaking slowed in the second quarter of 2025 as tariff-related uncertainty disrupted the momentum built in early 2024. Fund managers are facing rising pressure to exit assets, return capital to investors, and secure new commitments amid volatile market conditions and a shift in global trade patterns.

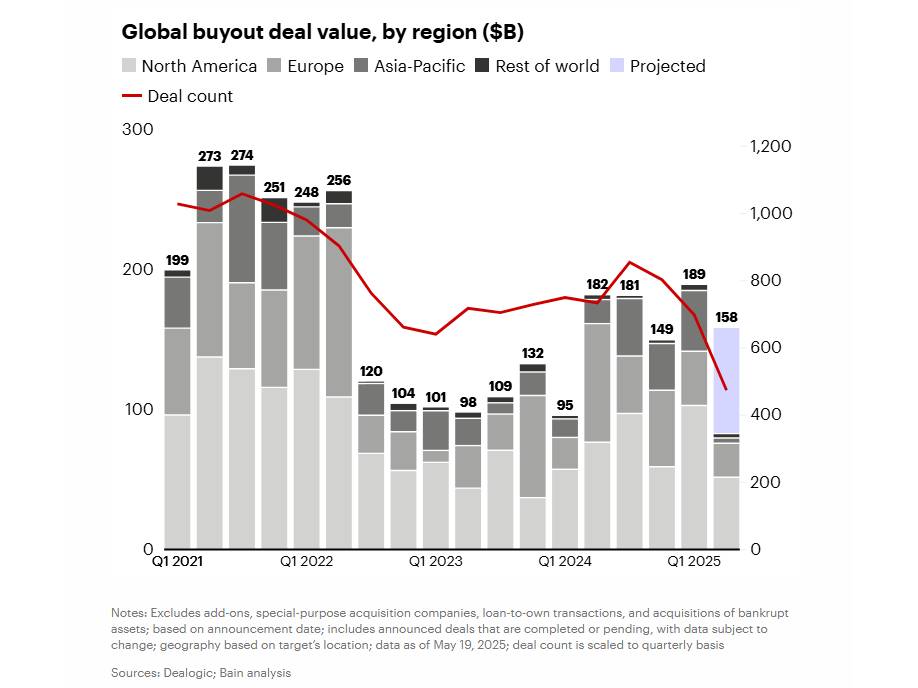

According to Bain & Company’s midyear report, global buyout deal value declined 24% in April compared to the first-quarter monthly average, while deal count fell by 22%. The IPO market, already subdued, stalled further, with several high-profile offerings—including Swedish fintech Klarna—delayed or paused.

The report highlights that the first quarter showed positive signals. Credit markets were accessible, debt costs were lower, and interest rate expectations had improved. The largest deals in the quarter included Sycamore Partners’ $23.7 billion acquisition of Walgreens Boots Alliance and Mubadala’s $13.4 billion sale of Nova Chemicals to OMV and ADNOC. But a policy shift on April 2, when the US announced sweeping tariffs, triggered renewed volatility in global capital markets.

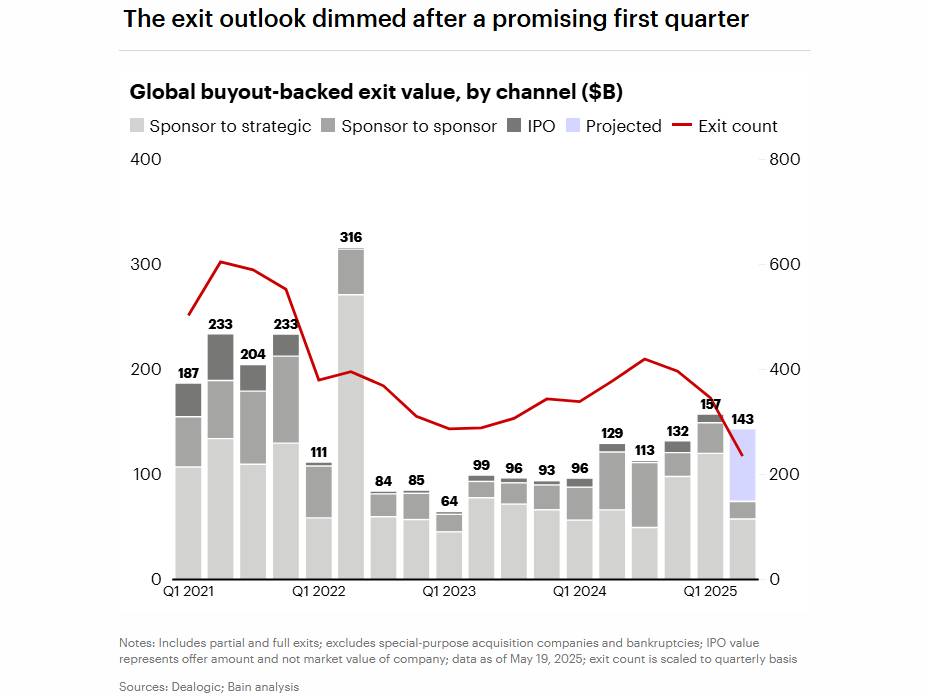

Exit activity also declined. LPs are calling for full, traditional exits to regain liquidity, even at lower valuations. A March 2025 Institutional Limited Partners Association poll found more than 60% of LPs prefer conventional exits over dividend recaps or minority sales. Limited partners have increasingly turned to the secondaries market, with notable examples including Yale University’s endowment and a $5 billion transaction by New York City’s pension funds, with Blackstone as lead buyer.

Despite strong growth in secondaries, they account for less than 5% of global private equity assets under management. With roughly $1.2 trillion in buyout dry powder, 25% of which has remained undeployed for more than four years, pressure to deploy capital is mounting.

Fund-raising remains weak. No buyout funds that closed in Q1 2025 exceeded $5 billion, marking a ten-year low. Bain estimates that over 18,000 private capital funds are seeking a combined $3.3 trillion in commitments, while actual available capital is about one-third of that target.

Tariff-related uncertainty has prompted one-third of LPs to reduce or pause private market investments. A growing number are reallocating to private credit and infrastructure. North American private equity (PE) assets remain dominant, but some European and Canadian limited partners (LPs) are reconsidering their allocations amid cross-border trade tensions with the US.

Operationally, GPs are being encouraged to refresh their value-creation strategies and enhance EBITDA performance, particularly as portfolio holding periods lengthen. Productivity gains driven by generative AI and cost control are being explored to counteract margin pressures.

Despite current headwinds, dealmaking has continued to occur. In May, 3G Capital announced a $9 billion acquisition of Skechers, just two weeks after the US shoe company withdrew guidance due to trade volatility.

The report noted that delayed exits, strained liquidity, and uncertain capital flows are expected to persist. Those that move early on exits, focusing on profit growth and reassessing portfolio strategies, will be best positioned to navigate the remainder of the year.