Debt is generally considered the fuel to grow in today’s capitalistic society. It provides relatively cheaper access to funds for businesses that can drive operations and expansion projects, capitalising on growth opportunities when they arise. Although life doesn’t work the same way, individuals often find themselves in need of debt to fund large purchases, such as a house or a car. At the same time, any personal emergencies might push an individual to seek debt to meet their needs.

Rather than taking a direct loan from the bank, customers can apply for various credit cards offered by local banks that let them borrow money to pay for goods and services. A customer can repay the borrowed sum by a specific due date without incurring any charges, or repay it gradually with interest, with monthly interest rates in the UAE ranging from 2% to 4%.

Navigating credit and maximising rewards

The reason to opt for credit cards becomes clear when looking at the benefits they offer. However, it’s essential to get the basics right first. If one cannot handle finances effectively, credit cards can often prove to be a risky option. Unless it is an emergency, a credit card should only be used to fund purchases that can be paid off at the end of the month, creating a sense of financial discipline and avoiding unwanted interest charges.

Funds can be generally borrowed up to a limit, based on several factors, including income, payment, and spending history on your existing cards, as well as your credit score.

Al Etihad Credit Bureau (AECB), a government-owned company, provides a three-digit credit score ranging from 300 to 900 that reflects an individual’s credit history and repayment ability in the country.

A higher score indicates lower risk, leading to faster approvals and better terms for financial products, while a lower score signifies higher risk, potentially resulting in loan rejections or less favourable rates.

With that in mind, let’s examine some cards offered by UAE banks that can help maximise benefits based on individual spending habits, subject to certain assumptions.

Set of assumptions made

- All numbers are denominated in AED.

- Spending is estimated for a family of four in the UAE.

- A cost of Dh55 per ticket is assumed for a standard theatre experience at Vox and Reel Cinemas.

- The benefits mentioned may not provide a comprehensive list of benefits offered by each of the cards. This could include additional cashbacks on other categories, discounts at domestic retail partners, and airport lounge access, among other benefits.

- Estimated savings do not consider any promotional offers going on at the moment.

- Eligibility of minimum salary requirements/credit scores.

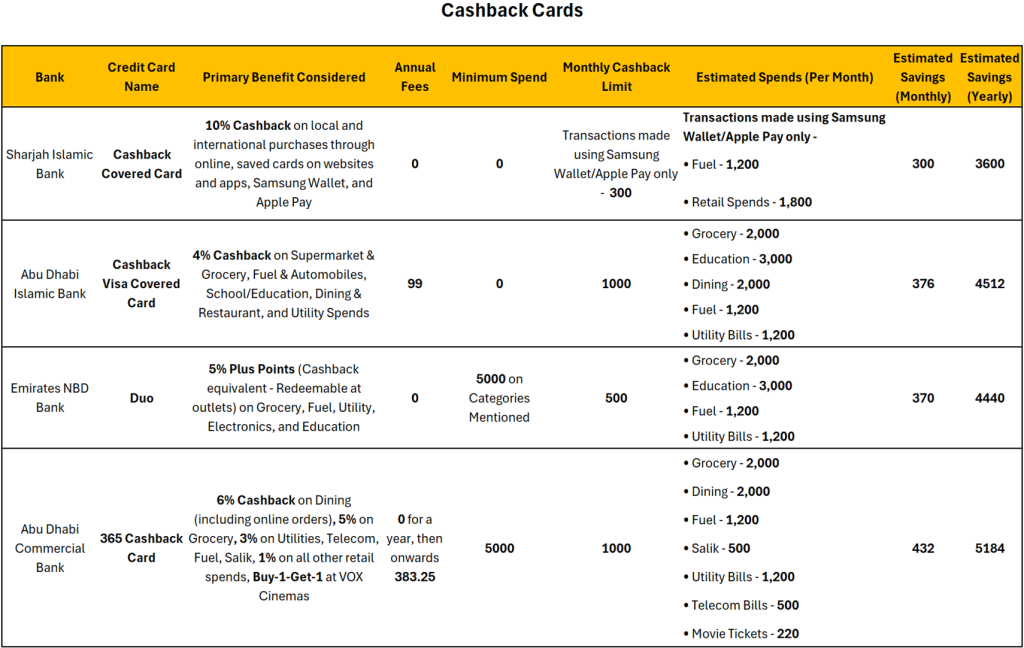

No minimum spend

The SIB Cashback card offers a 10% cashback benefit through payments made using Samsung Wallet or Apple Pay. Additionally, for a limited time only, the card is offering 100% cashback up to Dh1,000, making the deal even sweeter.

The ADIB Cashback card covers a wide range of daily expenses, offering a flat 4% cashback while charging an annual fee of only AED 99.

Dh5,000 minimum spend

The ENBD Duo card, exclusive to Abu Dhabi residents, offers 5% Plus Points on groceries, electronics, utilities, education, and fuel, which can be redeemed at various outlets across the UAE, subject to a minimum monthly spend on the categories.

The ADCB 365 Card is another excellent option, offering benefits across a wide range of expenses and providing the highest cashback among all the cards on the list. The annual fee from the second-year option does impact the total cashback slightly, but it still beats out any other card.

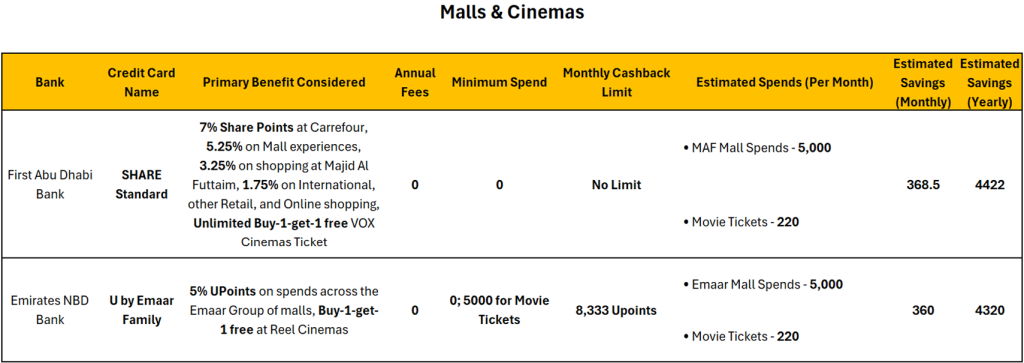

The FAB Share and ENBD U by Emaar are two of the best cards to use for spending at most malls managed by Majid Al Futtaim and Emaar in the UAE. Both cards are free for life and offer great reward points that can be redeemed in mall stores.

The key difference between the two lies in the movie ticket offers, where one requires a minimum monthly spend of Dh5,000 with the U by Emaar card to receive complimentary tickets. In contrast, no spending requirement is listed for the FAB Share Card. Therefore, benefits are calculated based on Dh5,000 to present both cards in an equal light.

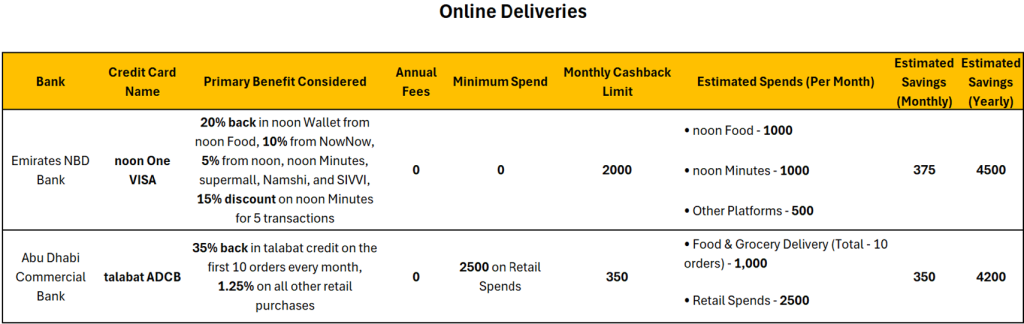

The ENBD noon One card offers a significant number of benefits on food and grocery deliveries, along with shopping on various websites, providing an all-around solution for online purchases, without any annual fees or minimum spend.

For Talabat users, the Talabat ACDB card remains the only option that provides any benefit, albeit for the first 10 orders only, capped at Dh35 per order. This comes with a minimum monthly retail spend of Dh2500, with a total cashback limit of Dh350.

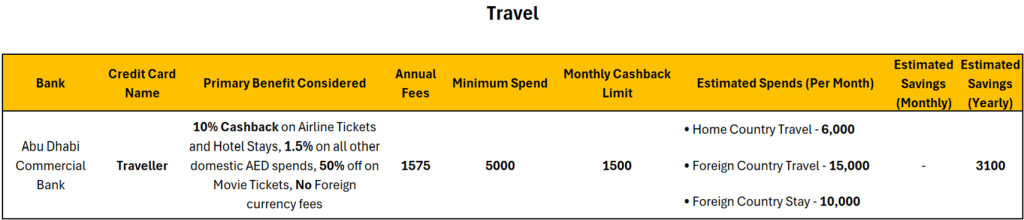

Lastly, the top travel pick is the ADCB Traveller card. Although other cards, such as the RAK World or the FAB Travel, could be included in the list, their high minimum monthly spend or complex terms of eligibility for cashbacks make them undesirable. Air miles cards are also excluded from the list; however, they could provide significant benefits for travellers loyal to an airline.

The ADCB Traveller is the only card on the list that charges a significant annual fee of Dh1,575; however, the benefits could outweigh the costs. The estimated savings are calculated based on just two trips per year and may vary significantly depending on the number of trips and their associated costs. The maximum monthly cashback of Dh1,500 means that there are no benefits to travel costs exceeding Dh15,000. Therefore, each travel expense is assumed to be incurred in a separate month to optimise cashback benefits.