GCC hiring received a mixed boost for some GCC states and sectors in Cooper Fitch’s latest report for Q3 as the labour market remains firm albeit with significant variation between the UAE and the remaining five GCC economies.

The UAE’s success in GRC hiring is also a significant achievement of the Emirates in Cooper Fitch’s Q3 report.

GCC Recruitment Trends

Hiring rose 1.3% quarter-on-quarter, reflecting a stable market as organisations maintained operational focus.

Hiring Leaders

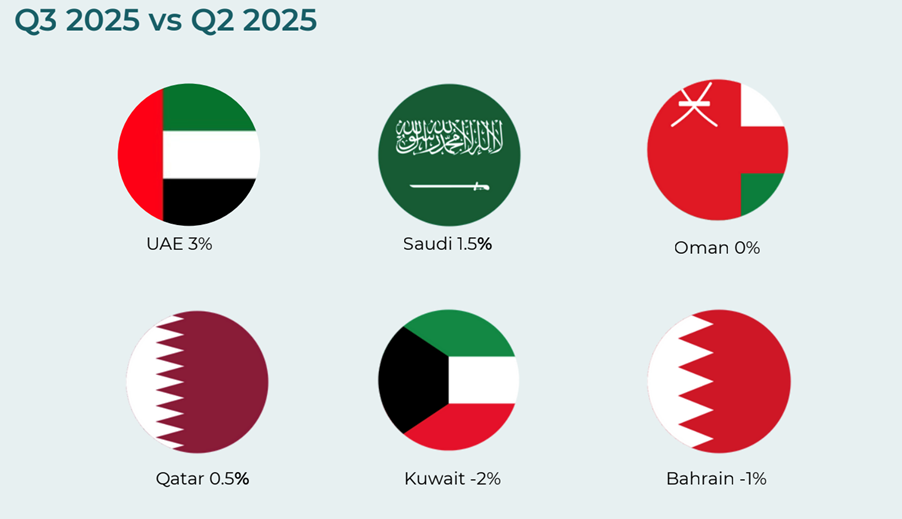

In first place, the UAE increased hiring across all sectors by 3% sustaining strong momentum as business activity picked up.

Coming in second is KSA, growing 1.5% because of steady project delivery and non-oil sector explanation whilst employers remain selective in adding headcount.

According to Dr Trefor Murphy, the CEO and Founder of Cooper Fitch, the “UAE and KSA are driving way ahead economically than any immediate Gulf countries. This was followed by Qatar despite a significant gap.

Dr Murphy went further: “Even with this gap between the UAE and KSA, Kuwait and Bahrain are quite a way from Qatar.” It comes as Qatari hiring stood at 0.5% in Q3: one sixth of the percentage increase on hiring than the UAE for Q3.

Omani, Bahraini, and Kuwaiti labour markets remained flat or contracted in Q3.

Cooper Fitch: GCC Hiring Rates (Q3 2025 vs Q2 2025)

Steady Contenders

However, Qatari and Omani firms held off hiring. Hiring plateaued at 0.5% as LNG projects are yet to translate into meaningful workforce demand.

Oman continues to see stable credit conditions and policy support yet there remains limited job creation.

Falling Hiring Rates

Softer business growth costed Kuwaiti and Bahraini firms with hiring cuts in Q3: hiring declined 2% in Kuwait whilst hiring also declined by 1% in Bahrain.

Sectorial Growth

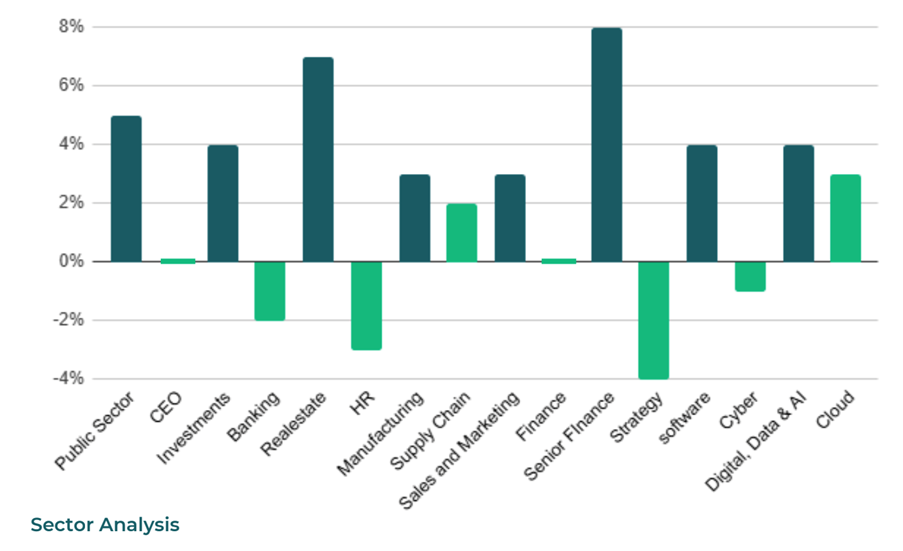

Despite the inter-state differences across the GCC labour market, there remains high growth across the bloc for ‘Investments’ and ‘Senior Finance.’

Employers concentrated on operational and leadership roles to support sustained growth across these key sectors especially in the UAE, KSA, and Qatar.

Cooper Fitch: Gulf Employment Index (Q3 2025 vs Q2 2025)

Dr Murphy contextualised this uptick for Investments despite the “softer investment deal environment” because of a “pick-up in the operational and governance side” in terms of hiring.

On Senior Finance specifically, Dr Murphy explained that “Senior Finance had a dogged year in 2025 but Q3 saw a pickup in FP&A roles and also treasury positions but they have had quite a tough previous two quarters.”

GCC Hiring Winners: Senior Finance & Investments

Senior Finance recorded the sharpest rise in hiring (+8%) as demand for FP&A and treasury talent intensified across the GCC. Demand for managing liquidity, working-capital exposure, and funding structures grew as interest-rate uncertainty persisted.

Analytics, forecasting, and risk performance management are in demand by financial firms operating across the GCC irrespective of country-to-country variations.

GRC Buoyant: Success in the UAE’s Regulatory Crackdown

Other sectors have seen sustained success in 2025 across the GCC.

Dr Murphy highlighted the hiring success in Governance, Risk, and Compliance (GRC) this year as we talk GRC across financial services and products which has seen “a lot of growth” and “mitigation” across both sectors. This comes off the back of a quiet 2024.

The UAE and other GCC economies have placed a firm emphasis on AML regulations this year with the EU’s removal of the UAE from the Financial Action Task Force (FATF) grey list in February last year, followed by the EU’s removal of the UAE from enhanced due diligence on EU-UAE business investment transactions in July 2025.

Regulatory changes include tougher penalties for non-compliant firms operating in the UAE and stronger enforcement via the Financial Intelligence Unit.

GCC Hiring Losers: Banking and Strategy

However, banking hiring eased as several UAE banks advanced M&As streamlining operations whilst advancing digitalisation programmes.

Cooper Fitch notes a potential “gradual pickup” in activity heading into Q4 as new mandates in credit, treasury, and risk demand hiring.

Outlook for GCC in 2026

2026 is the million-dollar question.

“It is quite difficult to say right now, but I think you are looking at continual job growth in the UAE between 4-6% whilst it is hard to predict in KSA because of a lot of uncertainty on fiscal spending across the public sector despite buoyant private sector spending,” said Dr Murphy.

In Oman, there are “no expected changes despite better government policy in investment” in 2026. On Bahrain and Kuwait, they remain “solid” but no significant growth here, similarly in Qatar remaining pretty flat.

Together the labour market remains firm across the GCC, specifically the UAE, whilst KSA hiring remains the bigger question right now.

Stay Up to Date with the Latest Analysis at Finance ME!

Saudi 2026 Budget Pitch to Investors: Less Neom, More AI

S&P GCC Banking Outlook 2026: Stable for Now Pending Oil Assumptions

Inside the 2025 Wealth Shift: New Billionaires, New Power Shifts