The gold market saw significant changes in the second quarter of 2024, driven by record-high prices, increased over-the-counter (OTC) investments and substantial purchases by central banks.

This period marked a notable phase in the history of the gold industry, with the average gold price reaching $2,338 per ounce, reflecting an 18% increase year-on-year and a 13% rise quarter-on-quarter. The gold price hit a new high of $2,427 per ounce in May. This surge was driven by several factors, including a robust OTC investment of 329 tonnes, which was a significant component of the total gold demand for the quarter. These factors and ongoing central bank purchases pushed the gold price to new heights. The demand for gold as a safe-haven asset amid economic uncertainties and geopolitical tensions also played a crucial role. Additionally, inflationary pressures and a weaker US dollar likely enhanced gold’s appeal as a store of value and an investment vehicle.

Supply and demand dynamics

Total gold supply in the second quarter of 2024 grew by 4% year-on-year to 1,258 tonnes, according to World Gold Council’s Gold Demand Trends Q2 2024. This increase was driven by record mine production of 929 tonnes for a second quarter and the highest recycling supply since 2012, responding to rising gold prices. Despite the high supply and demand dynamics varied across different regions and sectors. While the demand for gold bars, coins, and ETFs remained strong in the East, it saw a marked decline in the West. However, Western ETF investment flows began to return in the third quarter, suggesting a potential shift in investment patterns.

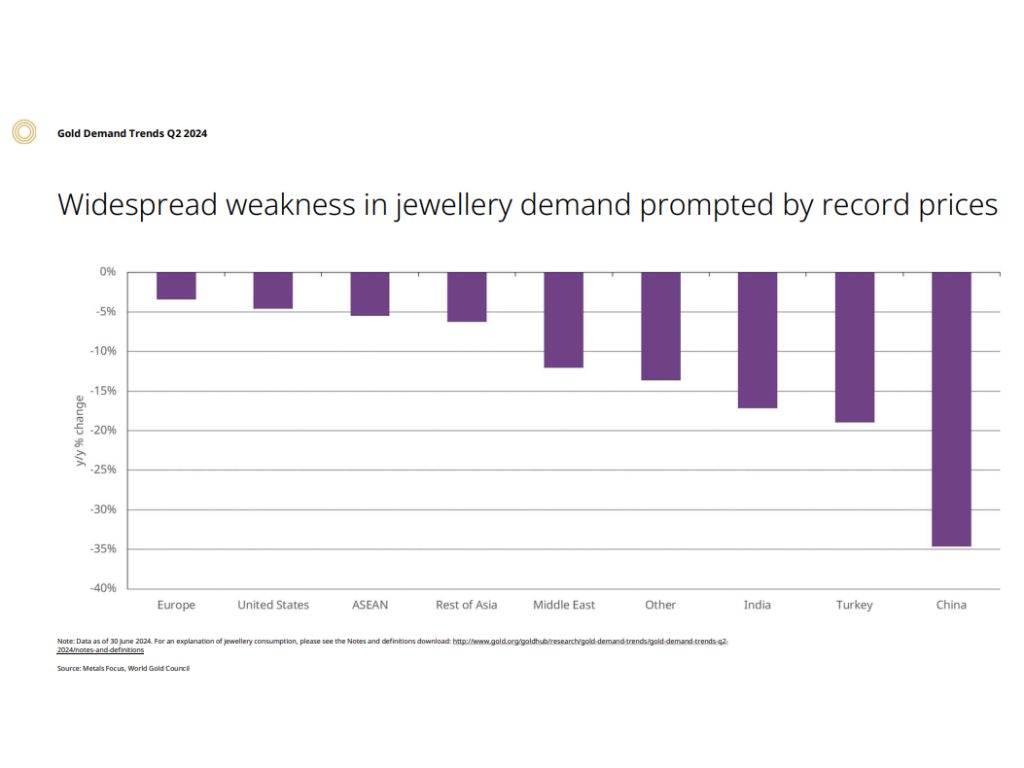

Decline in jewellery consumption

The record gold price environment had a notable impact on jewellery consumption in the second quarter of 2024, with volumes falling by 19% year-on-year to a four-year low of 391 tonnes. This decline was largely due to the high prices, which deterred consumers from purchasing gold jewellery.

“In value, Q2 jewellery demand measured $29 billion,” the report read. That was 4% lower year-on-year as the sharp rise in the gold price did not quite compensate for the decline in volumes.

“H1 demand, in value terms, was 2% above H1 last year at $61 billion—the highest H1 since 2013, when Q2 demand spiked to a record volume of 834 tonnes.

In China, jewellery demand dropped significantly due to the weaker domestic economic picture and record gold prices. The economic slowdown and rising gold prices created affordability constraints for consumers, leading to a sharp decline in demand during traditional peak buying periods.

The surging gold price and decelerating domestic economic growth were the two major reasons for sluggish gold jewellery demand in H1.

World Gold Council

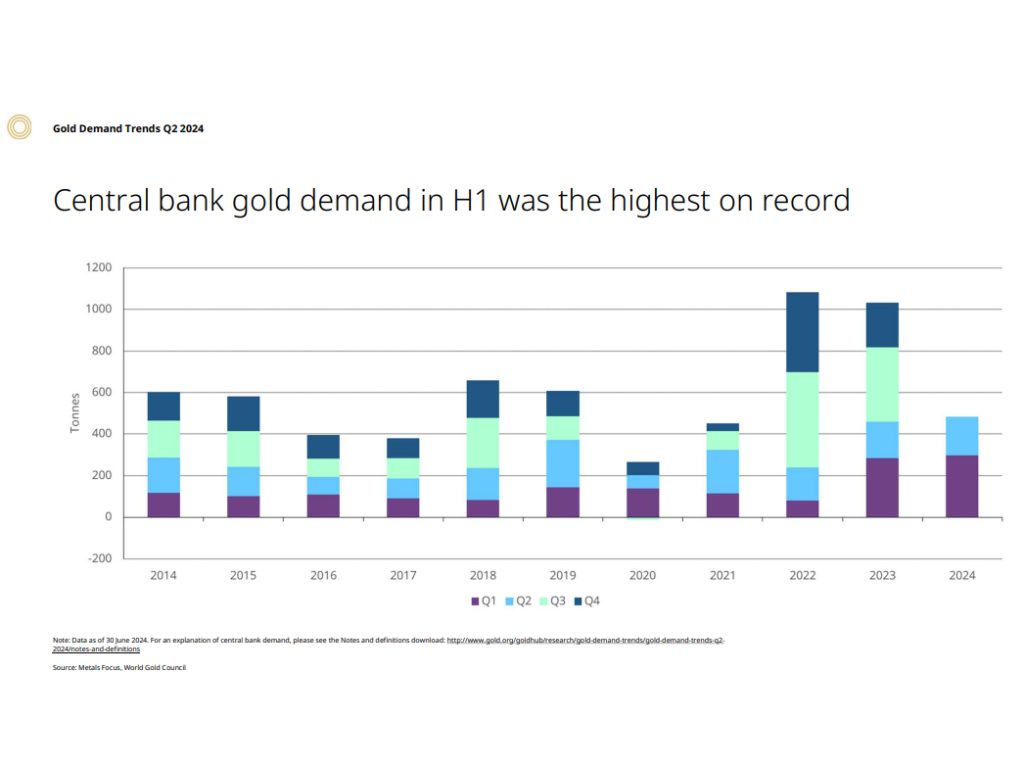

Central bank purchases

Central banks remained major players in the gold market, with net gold buying increasing by 6% year-on-year to 184 tonnes. This trend was driven by the need for portfolio protection and diversification amid global economic uncertainties. The second quarter also saw a minor decline of 7 tonnes in global gold ETF holdings, which compared positively with the 21-tonne drop in the same period the previous year. Early outflows in the quarter were followed by nascent later inflows, indicating a renewed interest in gold investments.

The National Bank of Poland (NBP) became the joint largest buyer in Q2. The bank’s first purchase since Q4 2023 added a net 19 tonnes to its gold reserves and lifted its total gold holdings to 377 tonnes, accounting for 13% of total reserves. At a news conference in early June, Governor Adam Glapinski reiterated his plan to increase gold’s share of total reserves to 20%.

Outlook for H2 2024

Looking ahead, the gold market is expected to maintain its strong performance in the second half of 2024. According to the report, several factors will influence the gold market in the coming months. The potential for lower policy rates in major economies, high fiscal deficits and increased market volatility are expected to drive demand for gold investments. Central bank buying is also expected to remain strong, although there are some downside risks, such as a possible pull-back in central bank purchases and weaker retail investment in emerging markets. Conversely, a more significant economic slowdown in developed markets and lower policy rates could increase interest in gold investment products. Geopolitical uncertainties could also increase market volatility, further boosting gold demand.

Supply considerations

On the supply side, mine production is poised to surpass previous records, supported by output from several regions, including Africa. Record all-in-sustaining cost (AISC) margins are also favourable for increased production. However, the downward revision to first-quarter output makes this target more uncertain. While significant, recycling was lower than anticipated in the second quarter due to a decline in India, where gold-for-gold exchanges and loans were more prominent. Europe’s response to high prices and economic uncertainty could lead to increased recycling in the year’s second half.

Regional investment trends

Regional investment trends continued to diverge in the second quarter of 2024. In the East, demand for bars, coins, and ETFs remained robust, driven by economic uncertainty and underperformance of domestic assets. Indian bar and coin demand responded positively to rising prices, with expectations of further gains encouraging investment. Healthy monsoon rainfall supported rural incomes, sustaining investment demand. Additionally, the recent cut in import duty on gold in India can potentially boost retail demand significantly. In contrast, Western markets saw a decline in retail bar and coin investment, although ETF investment flows began to show signs of recovery in the third quarter.

The second quarter of 2024 was marked by significant developments in the gold market, driven by record-high prices, increased OTC investments, and substantial central bank purchases. While the high gold prices negatively impacted jewellery consumption, they spurred investment demand and technological use of gold. As the market moves into the year’s second half, the outlook remains positive, supported by ongoing economic and geopolitical uncertainties. The balance of supply and demand will continue to shape the gold market, with regional trends and sector-specific dynamics playing crucial roles in determining the overall direction.