The Gulf Cooperation Council (GCC) insurance industry is expected to experience a slowdown in growth across certain markets as insurers navigate a changing economic landscape, intensifying competition, and regulatory challenges. According to S&P Global, while economic stability in the region is projected to continue over 2025-2026, factors such as market saturation, underwriting pressures, and regulatory interventions could impact the sector’s expansion.

Despite ongoing geopolitical tensions and trade disruptions, economic conditions in the GCC remain conducive to insurance demand, supported by infrastructure development and population growth. The insurance sector has benefited from mandatory coverage schemes and rate adjustments, particularly in Saudi Arabia and the UAE, where the size of insurance markets has doubled since 2020. However, increasing competition and volatile financial markets pose risks to profitability, particularly for smaller and midsize players.

While underwriting results remain broadly stable, and higher interest rates have provided a buffer for insurers’ earnings, a widening gap between larger and smaller companies is becoming evident. In the UAE, the top five listed insurers accounted for 81% of total earnings as of December 2024, reflecting a concentration of profitability among a handful of firms.

A similar trend is seen in Saudi Arabia, where the top five players generated 82% of industry earnings in the third quarter of 2024. Smaller insurers, in contrast, face higher operating costs, weaker earnings, and capital constraints that could limit their ability to compete effectively.

Stricter regulations are accelerating industry consolidation, particularly in markets like Saudi Arabia, where competitive pressures and weak capital buffers have prompted mergers and acquisitions since 2018. A comparable shift is emerging in the UAE, where regulatory scrutiny is increasing for insurers operating below the minimum solvency capital requirements. Approximately 20%-25% of listed insurers in the country are at risk of regulatory intervention unless they can restore capital buffers. The ongoing push for market stability through consolidation is likely to continue into 2025.

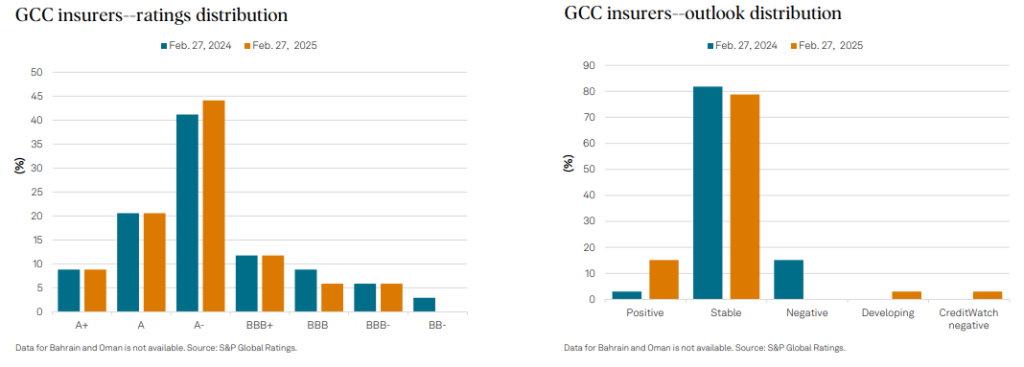

Despite these challenges, the credit outlook for the region’s largest and most well-capitalized insurers remains stable. Around 90% of rated insurers hold capital at the highest level under risk-based capital adequacy models. However, for smaller and unrated companies, financial pressures are likely to mount if competition continues to intensify, potentially leading to weakened credit profiles and solvency concerns.

In Saudi Arabia, the market remains dominated by a few large insurers, with the top five firms accounting for nearly three-quarters of total revenues and earnings. The intense competition in motor and medical insurance has resulted in cyclical pricing, further squeezing margins for smaller players. In the UAE, premium growth is expected to be driven by rate increases in the property and casualty segment, but rising reinsurance costs may erode earnings, particularly for smaller and midsize insurers. Additionally, a significant number of firms in the UAE operate at or slightly above the minimum solvency capital requirements, increasing the likelihood of regulatory action.

Qatar’s insurance sector remains highly profitable, outperforming other GCC markets in underwriting performance and return on equity. However, growth prospects are more subdued, with limited new government-backed insurance schemes. High exposure to equity and real estate assets also raises concerns over potential earnings volatility. In Kuwait, infrastructure projects continue to drive moderate growth of 7%-10% annually, but the market remains highly competitive, especially among insurers offering Sharia-compliant products. Economic uncertainties and institutional constraints further add to the sector’s challenges.

While the GCC insurance market continues to expand, the pace of growth is uneven across countries and segments. Insurers must adapt to evolving regulatory frameworks, competitive pressures, and capital requirements to sustain profitability and market positioning. The industry’s ability to navigate these headwinds will determine its long-term stability and growth trajectory.