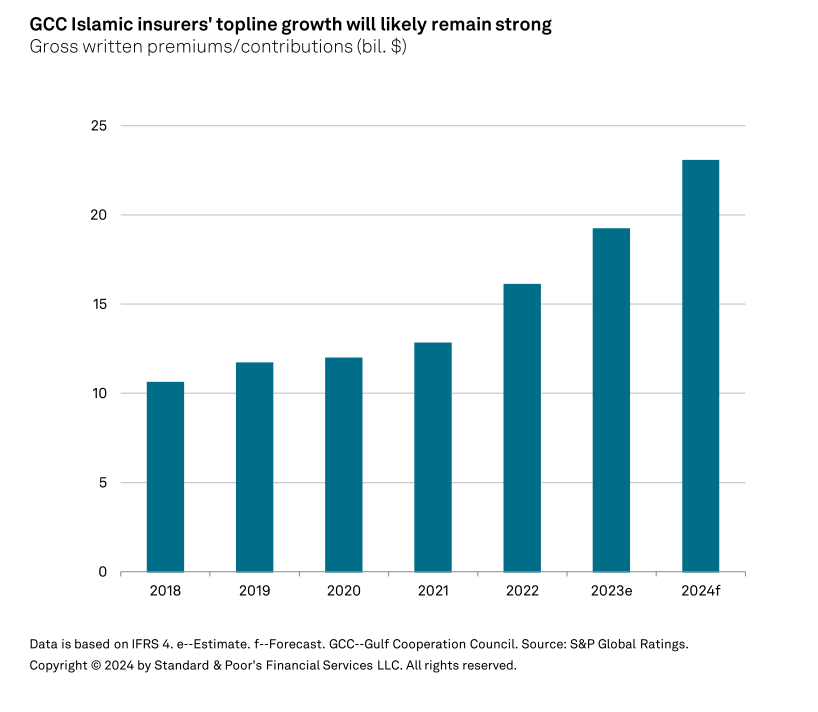

Islamic and Takaful insurers in the Gulf Cooperation Council (GCC) region can expect to see continued growth in 2024, with experts pointing towards an expansion of 15 to 20%.

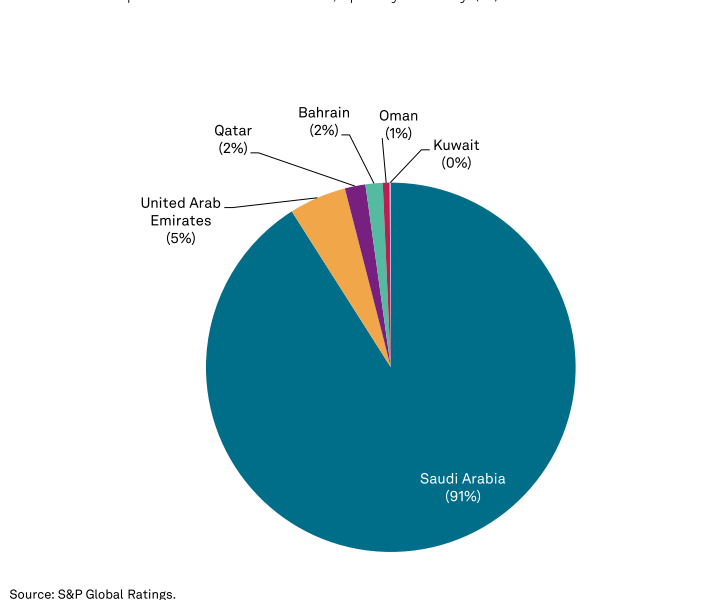

A recent S&P Global report has highlighted higher insurance demand in Saudi Arabia, the largest Islamic insurance market in the region, as the main driver of the sector’s growth.

The Islamic insurance sector had a very profitable year in 2023, with total net profits nearly crossing the $1 billion mark, mainly due to rate adjustments in previously underperforming lines and higher investment returns. S&P Global expects this trend to continue, as the Saudi market continues to expand and authorities further their efforts to reduce the number of uninsured vehicles and introduce new mandatory medical covers, leading to additional insurance demand and premium income.

In 2023, all of Saudi Arabia’s 25 listed insurers reported a net profit

“That said, we expect competition will pick up in some markets.,” the report stated. “This, together with anticipated interest rate cuts starting from September and potentially more volatile capital markets, could lead to a sharp decline in earnings in 2025 if Islamic insurers fail to maintain their underwriting discipline.”

Set for success

During the past five years, the Islamic insurance sector in the GCC region has greatly expanded. This growth was particularly noticeable in the period between 2022 and 2023, when the sector increased by about 20% to 25% annually, reflecting the significant growth experienced by the Saudi Arabian market, which expanded by about 27% in 2022 and another 23% in 2023.

The publication of half-year 2024 results suggests that net profits could further improve this year. The aggregate net profit in the sector improved to about $967 million in 2023, from about $100 million in 2022. In 2023, for the first time, all of Saudi Arabia’s 25 listed

insurers reported a net profit, in contrast to previous cycles in which about half reported a net loss.

Despite the Kingdom’s growth, S&P pointed out that Islamic insurers’ topline in GCC countries outside of Saudi Arabia cumulatively declined by almost 3% in 2023. The main reason for the decline was the decrease in premium income in the UAE, the region’s, primarily due to consolidation in the industry and rate pressure. Nonetheless, researchers expect the UAE Takaful sector in the UAE to turn this trend around, predicting growth of between15% and 20% in 2024

At the same time, Takaful players in Bahrain, Kuwait, Oman, and Qatar are expected to report moderate growth rates of about 5% to 10%.

Top risks

Although GCC Islamic insurers are set to continue to benefit from several tailwinds

over the next six to 12 months, increasing competition and declining investment returns could weigh on the industry’s earnings.

One of the key aspects highlighted in the report is geopolitical risks. A regional escalation of conflicts could impair business sentiment in the wider Middle East, including the GCC region, reduce growth prospects and impair GCC insurers’ investment portfolios.

Moreover, consolidation will likely continue to stay relevant as many smaller and midsize Islamic insurers report relatively weak earnings. Over the past five to six years, the number of listed Saudi insurers declined by about 20% to 27, from 34. This trend is expected to continue, as several Islamic insurers “still fail to meet the required solvency capital

requirements”, as reported by S&P.