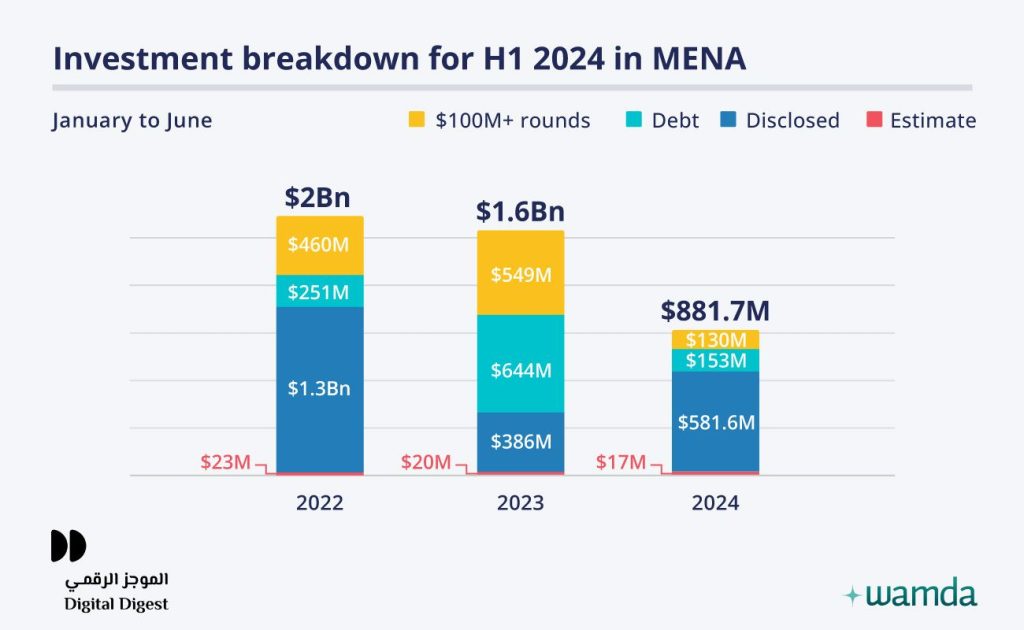

Investment activity in the Middle East and Africa (MENA) startup space slowed down in the first six months of 2024, as the region reported a 46% decrease in total funding to $882 million, down from $1.6 billion in H1 2023.

Excluding the $644 million of debt financing in H1 2023, the decline drops to 12%, according to the latest data published by Wamda.

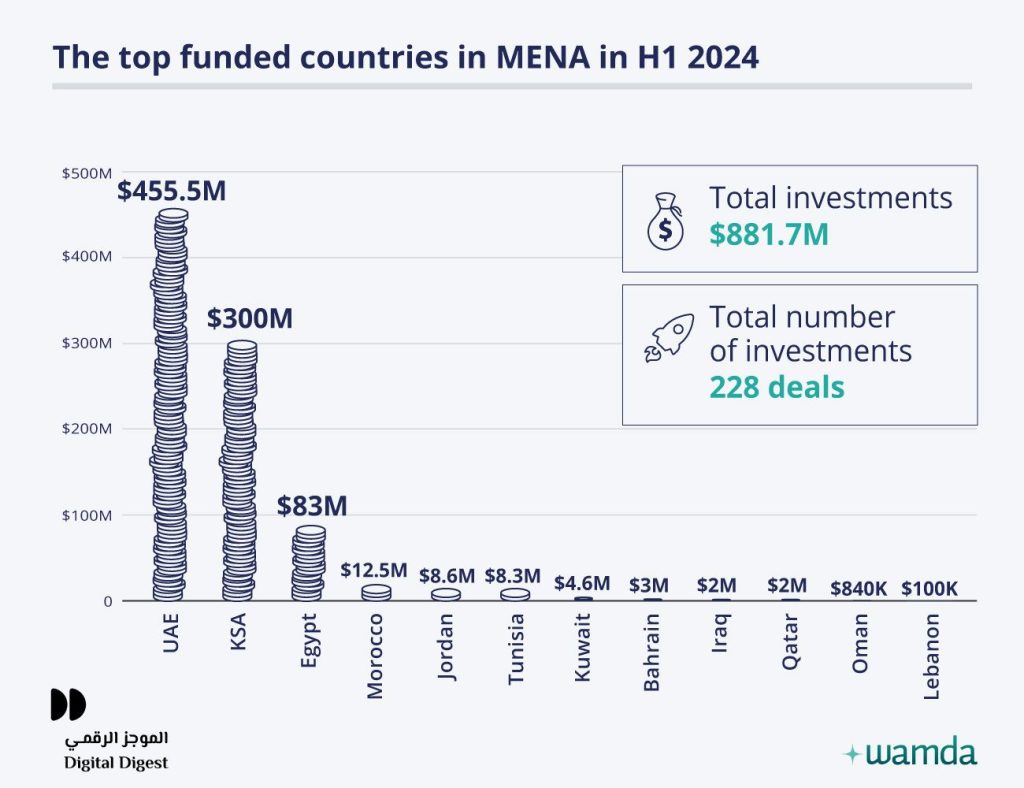

The UAE maintained its top spot as the leading ecosystem in the region, with 91 startups raising $455.5 million in the first six months of the year, though down from $604 million in H1 2023. Saudi Arabia followed, attracting $300 million, down from $554 million last year.

The Egyptian startup ecosystem saw a drastic decline, with just 33 startups raising $83 million, an 80% drop from the same period last year. In contrast, the Moroccan ecosystem is gaining momentum, with six startups raising $12.5 million.

In Q2 2024, funding saw a slight rise, with 98 startups raising $453 million, a 5% increase from Q1’s $429 million, but a 9% decrease compared to Q2 2023. Despite the lower numbers, Wamda researchers expect investment to increase in H2 2024.

“The first half of the year saw a slowdown in the investment landscape, however, it is not an indication of the performance of the rest of the year,” the report stated. “We can consider it a needed consolidation to assess the market sentiment toward each sector, or a halftime pause, so that VCs can close their funds, and investors can consider diversifying their investment portfolios based on the US Federal Reserve’s interest rate.”

June performance

Looking at June 2024, 38 tech startups raised $116 million. The amount amounted to a 59% month-on-month decline but rose 182% when compared to the same period was year. The biggest ticket size was Tenderd’s $30 million deal.

UAE-based startups led the region, securing $82.5 million across 15 deals. Egyptian startups followed with $15 million raised by four companies, while seven Saudi startups raised $13.5 million. Notably, six Iraqi startups raised an estimated $1.2 million.

Fintech was the top-funded sector in June, securing $38 million over 10 deals, followed closely by contech, as a result of Tenderd’s deal. Three proptech startups raised $19.6 million, reversing their lead from May.

The majority of investments in June went to the pre-Series A stage, with four startups receiving $45 million. The seed stage saw five startups raising $27.3 million. Early-stage startups also attracted attention, with eight pre-seed startups garnering $3 million and eight others receiving $140,000 in grants.

The report showed that business-to-business (B2B) startups dominated funding, raising $66.4 million across 18 deals and accounting for 74% of the total investment. In contrast, 20 business-to-consumer (B2C) startups raised $49.5 million.

In terms of gender distribution, male-founded startups received the majority of funding, securing $103.4 million or 89% of the total, while only two female-led startups raised $200,000.