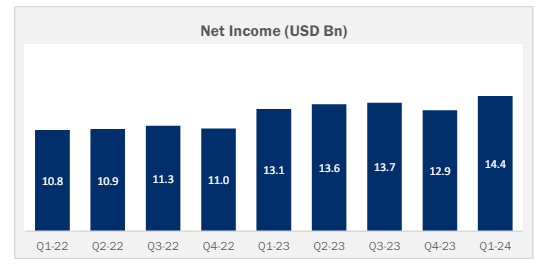

Gulf Cooperation Council (GCC) banks demonstrated a 10.5% annual growth rate in the first quarter of 2024 to reach $14.4 billion, according to the latest GCC Banking Sector Report released by kamco Invest.

The report examined the financial results of 57 listed banks in the GCC for the first three months of the year. Its findings revealed that UAE-listed banks recorded the biggest quarterly growth during Q1 2024, at 5.6%, with total customer deposits reaching $803.2 billion.

The strong growth came “despite a fall in revenues during the quarter and reflected a fall in total operating expenses coupled with a steep fall in quarterly impairments”, according to the report.

GCC banks booked $2.3 billion in loan loss provisions in Q1 2024, marking a five-year low. Total assets reached approximately $3.3 trillion, up from $3 trillion a year ago, while loans grew to $1.92 trillion from $1.8 trillion over the same period, according to the findings.

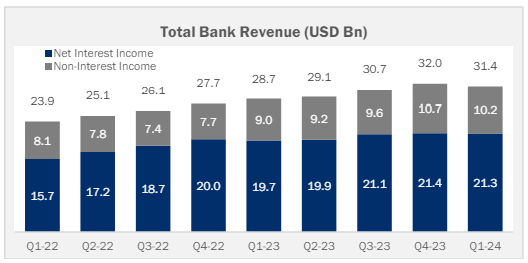

The impact of elevated interest rates was reflected in the quarterly revenue for the sector, which was down for the first time in 12 quarters.

Overall, revenues for the sector reached $31.4 billion, down from a record high of $32 billion during the previous quarter but higher than the $28.7 billion recorded in Q1 2023. The researchers attributed the quarterly decrease to the decline in net interest and non-interest income.

“The quarter registered flattish growth in total interest income that reached $50.5 billion with the yield on credit averaging at 4.3%, in line with the trend over the last three quarters, whereas a small increase in interest expense resulted in a marginal decline in net interest income,” the report said.

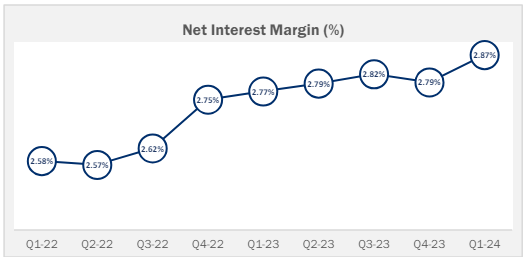

This was also reflected in the cost of funds that reached 4.5% at the end of Q1 2024, one of the highest on record for the GCC banking sector, from an average of 4.2% during

Q4 2023 and smaller 2.5% during Q1 2023.

The UAE ranked first in the region when looking at net interest margin (NIMs), amounting to 3.49% in Q1-2024. Saudi Arabian, Qatari and Kuwaiti banks followed, with a NIM of 3.18%, 3.06% and 2.87%, respectively.

“The higher margins as compared to Gulf peers reflect ample liquidity that allows UAE banks to capitalise on the tightening interest rate cycle with more modest asset growth,” the report noted.

Meanwhile, lending growth continued in the region.

Data from central banks in the GCC showed higher lending for all the GCC country

aggregates in Q1 2024, compared to the previous quarter. Saudi Arabia registered the strongest quarterly growth at 3.3% while UAE banks showed a growth of 1.1% during the first two months of the year.

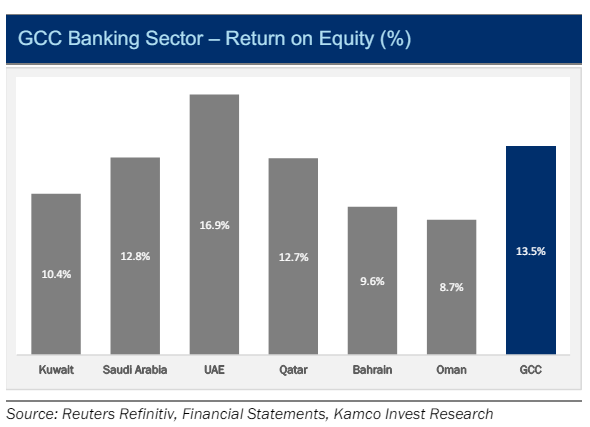

At the country level, UAE-listed banks topped the region with the highest return on equity (RoE) at the end of Q1 2024 at 16.9%, closely followed by Saudi Arabian and Qatari banks at 12.8% and 12.7% per cent, respectively.

The biggest yearly growth in RoE was also seen for UAE-listed banks at 280 bps, led by elevated profits and relatively smaller growth in total shareholders’ equity.