The Organization of the Petroleum Exporting Countries (OPEC) released its Monthly Oil Market Report (MOMR) for January 2025, detailing trends in crude prices, supply and demand balances, economic forecasts, and refinery operations. The report highlights stability in oil demand growth, with sustained contributions from non-OECD countries and steady economic growth globally.

Crude oil prices

In December 2024, the OPEC Reference Basket (ORB) marginally increased by $0.09, averaging $73.07 per barrel, while ICE Brent and NYMEX WTI averaged $73.13 and $69.70 per barrel, respectively. GME Oman crude rose by $0.68 to $73.16 per barrel, reflecting regional demand in Asia-Pacific. Backwardation deepened in futures markets, signalling near-term optimism among traders, driven by reduced US stock levels and speculative activity.

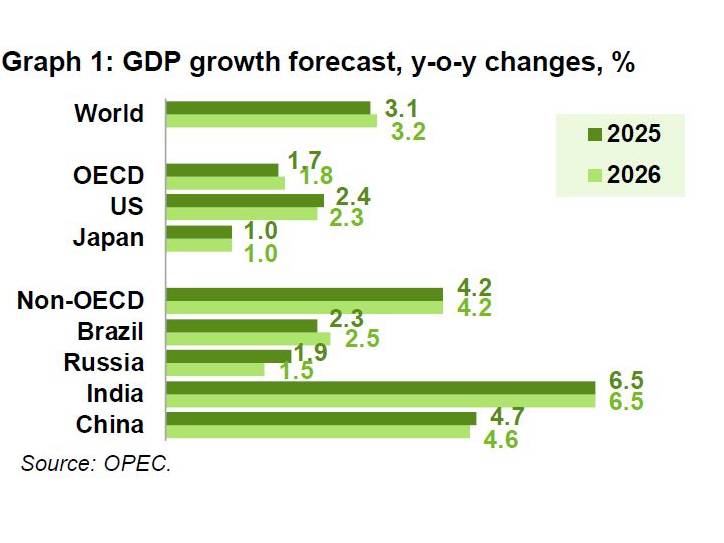

Economic outlook

OPEC projects global economic growth to reach 3.1% in 2025, slightly increasing to 3.2% in 2026. Growth drivers include inflation normalisation and adjusted monetary policies in key economies. India and China remain pivotal, with expected growth rates of 6.5% and 4.7% in 2025, respectively. Advanced economies such as the US and Eurozone are forecast to grow modestly, while Brazil and Russia show improved projections due to recovering industrial and export sectors.

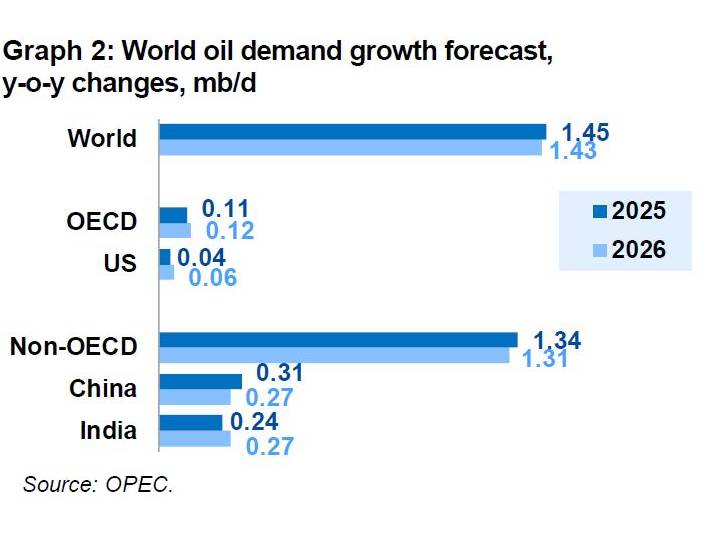

Oil demand and supply dynamics

Global oil demand is set to grow by 1.4 million barrels per day (mb/d) annually through 2026. Non-OECD countries, led by India, China, and the Middle East, will contribute approximately 1.3 mb/d annually, with OECD regions accounting for an additional 0.1 mb/d.

Non-Declaration of Cooperation (DoC) countries are forecast to increase liquids production by 1.1 mb/d annually through 2026, with the US, Brazil, and Canada being the primary contributors. Meanwhile, crude production by OPEC members participating in the DoC saw a marginal decline of 14 thousand barrels per day (tb/d) in December 2024.

Refinery operations and product markets

Global refinery intake reached 82.2 mb/d in December 2024, marking a 1.1 mb/d increase month-on-month. While US Gulf Coast refining margins weakened, improvements were observed in Europe due to higher seasonal travel and strong demand for gasoline and jet fuel. Asia-Pacific refiners also supported demand, particularly for middle distillates and naphtha.

Trade and tanker market trends

Crude imports into the US fell slightly to 6.5 mb/d in December, while exports hovered near 4 mb/d. Product trade flows saw US exports reaching a record high of 7.01 mb/d. In China, crude imports surged to a 13-month high of 11.8 mb/d, reflecting increased industrial activity.

Tanker freight rates exhibited mixed trends. While VLCC rates declined on routes to Asia, Suezmax rates on US-Europe routes rebounded, and Aframax routes saw notable gains, particularly in the Atlantic Basin.

Stock movements and balance outlook

OECD commercial oil stocks fell by 8.4 million barrels in November 2024, standing 171 million barrels below the 2015–2019 average. Demand for OPEC DoC crude is forecast to average 42.5 mb/d in 2025, a slight increase from 2024, with projections for further growth in 2026.