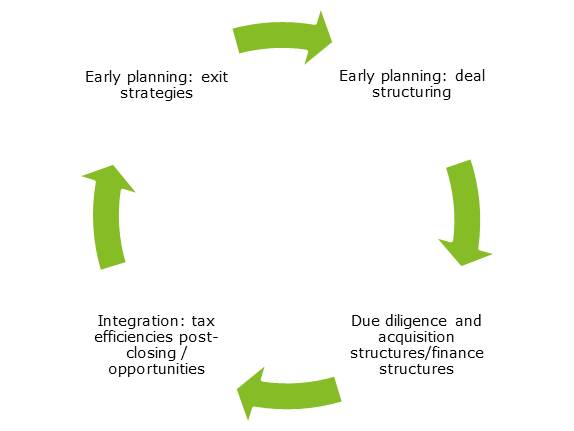

When investment teams evaluate the profitability of an investment in an M&A context, they use a key financial metric called the Internal Rate of Return (IRR). However, did you know that taxes can play a significant role in the factors contributing to this metric? From cash flows to net returns, tax considerations can impact various financial aspects of an investment.

Here’s a closer look at how tax may impact the IRR of an M&A transaction.

Asset purchase vs. share purchase

Structuring an investment as an asset purchase or a share purchase will have significant differences in the tax implications of the transaction.

An asset purchase provides the buyer with a basic step-up, enabling future depreciation deductions that can enhance post-tax cash flows and improve the investment’s internal rate of return (IRR). However, this approach often results in immediate tax costs for sellers (which is why they often prefer share sales), which conversely may drive up the purchase price.

Financing and interest deductibility

How you finance the acquisition can also affect the tax implications.

Interest in debt incurred to finance the acquisition is typically deductible for tax purposes, reducing taxable income and increasing post-tax cash flows. However, rules around limitations to interest expense deductions must be taken into account, as they can impact the benefit of leveraging transactions.

Where an acquisition is funded via equity financing, it is usually considered a more expensive financing option from a tax perspective compared to debt financing because dividend payments on equity are not tax-deductible.

Tax attributes

Acquiring a company with significant net operating losses (NOLs) can be advantageous as these losses can offset future taxable income, reduce tax liabilities and enhance post-tax cash flows. However, most jurisdictions (including in the UAE) have complex rules around the use of NOLs, and limitations might restrict the usage of NOLs after a change in ownership or business activities. This, in turn, may impact the value addition to the IRR.

Target companies with available tax credits (e.g., R&D credits) can offset future tax liabilities, thereby improving overall cash flow and the IRR.

Post-acquisition integration and restructuring

Effective post-acquisition integration can lead to operational efficiencies and synergies that are tax-deductible, such as restructuring costs and enhancing future cash flows.

Proper management of transfer pricing for intercompany transactions can minimise global tax liabilities, improving the profitability and the IRR of the multinational enterprise.

Exit strategy and capital gains tax

The taxation of exit proceeds (long-term capital gains vs. ordinary income) significantly affects the post-tax return on the initial investment. Structuring the deal efficiently during the acquisition phase can reduce exit tax liabilities, thereby enhancing the IRR.

Tax timing strategies

Deferring tax payments through methods such as instalment sales or reinvestment of proceeds in qualified opportunities can help in managing the timing of tax outflows, thereby optimising cash flows and improving the IRR.

Taking advantage of accelerated deductions for depreciation and amortisation can improve early cash flow, front-loading the benefits and enhancing the overall IRR.

What does this mean for your M&A strategy?

Tax considerations are integral to the financial modelling and valuation of M&A deals, directly affecting the IRR by influencing the cash flow generated from the investment. Understanding and strategically managing the tax impacts at each stage of the transaction—from structuring and due diligence to financing, integration, and exit—can optimise the after-tax returns and improve the IRR.

Considering these tax implications early in the deal process enables investment teams to make informed decisions and structure deals in a tax-efficient manner. This strategic approach not only enhances the IRR but also contributes to the overall success and profitability of M&A transactions.