In an age where digital transformation dictates the pace and direction of the banking industry, understanding the journey and the inherent challenges becomes crucial. Finance Middle East recently sat down with Jouk Pleiter, CEO of Backbase, to discuss the evolving landscape of digital banking, as he reveals both the hurdles and the high stakes involved in modernising banking practices.

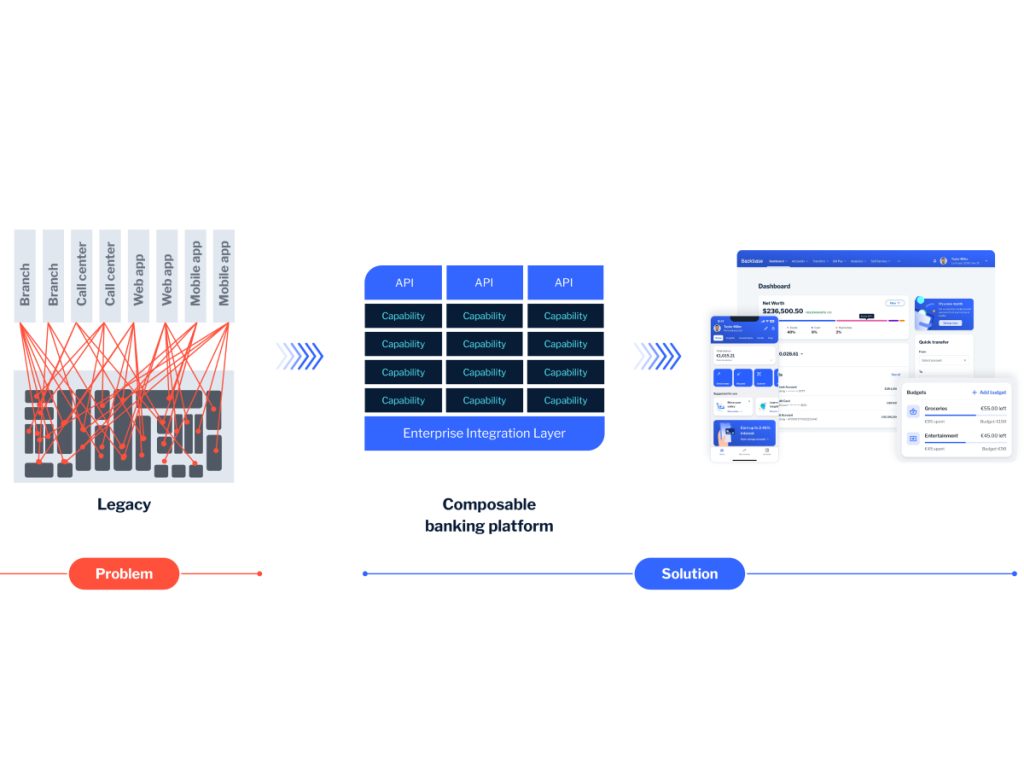

Pleiter begins by painting a bleak picture of the traditional banking model, which he believes is on the brink of collapse. “The traditional banking operating model, with its complex monolithic IT setups, is bound to crash,” he asserts. As banks have tried to integrate digital capabilities—such as online banking, mobile payments, and digital documents—into their existing structures, he states that they’ve created a tangled web or “spaghetti” rather than a seamless platform, powered by intricate integrations of systems, technologies and third parties

This approach, according to him, leads to “friction across digital and physical channels, causing frustration for customers and employees alike,” who find themselves navigating between disjointed functionality for basic banking needs. The result? “High customer servicing costs, slow response to inquiries, and prolonged time-to-market have become the trademarks of the traditional banking system,” says Pleiter.

Highlighting a McKinsey report, Pleiter notes that “only 30% of banks have successfully implemented their digital strategy, while 70% fail to achieve their objectives.” His solution to this dilemma is a shift towards progressively modernising existing tech stacks rather than throwing away investments made by banks over the years. “It’s not about fixing old systems; it’s about adopting a fresh and sustainable strategy,” he explains, advocating for a shift from channel-centric to customer-centric, which involves re-architecting banking around the customer.

Can technology reshape banking?

With a background in software development and web consultancy, Pleiter is uniquely positioned to comment on how technology reshapes banking. “Banks often focus on reaching the next level of excellence by leveraging existing tools and technologies,” he observes, noting that this process involves identifying and addressing gaps systematically.

However, he warns that this inward-focused approach can be a double-edged sword. “Attaining excellence demands a thorough comprehension of user requirements,” he says, stressing the importance of building a lean and agile architecture to meet these needs effectively. Yet, he acknowledges the difficulty of effecting change within a complex landscape without causing substantial disruptions, emphasising that “modernisation is not a sprint but a marathon.”

When discussing the drivers behind the demand for seamless digital banking experiences, Pleiter emphasises the importance of flexible and scalable banking architecture. “However, to do this, you will need to reduce dependency on your core banking systems,” he advises, suggesting the movement of additional logic from the legacy core into the engagement and integration layers.

He explains that Backbase facilitates this with a holistic architecture that decouples capabilities into generic modular platform services, encompassing everything from identity and entitlements, customer experience, omnichannel banking, human assistance, and process orchestration to customer data and artificial intelligence. “The Backbase suite… works in tandem with all capabilities, giving a strong foundation to run with on Day 0 or customise at speed,” he asserts.

The future of banking

Looking towards the future, Pleiter touches on the significant trends shaping banking and the increasing collaboration between fintech companies and traditional financial institutions. He views seamless banking integrations as crucial for operational efficiency, allowing banks to connect various channels seamlessly and streamline operations.

He argues that this strategic adoption is pivotal for navigating the dynamic financial landscape, ensuring synchronised efficiency across systems, and driving sustained growth.

Continuing, Pleiter emphasises the critical role of adopting a customer-centric approach for financial institutions striving to enhance customer engagement. “We offer banks the opportunity to break free from the constraints of legacy IT systems and embrace a new-generation engagement banking platform,” he explains.

By decomposing disparate legacy systems, Backbase enables the construction of a modern customer engagement orchestration architecture. This strategic shift, according to Pleiter, allows banks to “prioritise essential customer journeys across all touchpoints,” thus eliminating silos and empowering both customers and bank employees.

He highlights transforming from a point-to-point journey model to a fully integrated channels model. This shift not only reduces communication gaps that impact service costs and operations but also allows banks to offer innovative and personalised experiences. “Achieving this involves leveraging a robust system of engagement across all channels, fostering increased satisfaction, streamlined operations, optimised investments, heightened productivity, increased revenues, and accelerated growth,” Pleiter adds.

Regulatory compliance is another cornerstone for financial institutions. Pleiter discusses how Backbase supports its clients in this complex landscape. “Our platform is secure by design, built using zero-trust principles,” he states, which enhances the bank’s cyber resilience and risk management. This design allows financial institutions to bolster their defences and effectively detect breaches, ensuring they remain compliant and secure amidst evolving regulatory challenges.

Continuing, Pleiter cites the example of MCB’s modernisation journey in 2018 using Backbase’s ENgagement Banking Platform for an omnichannel approach, significantly accelerating MCB’s innovation and product development. “MCB’s story is a masterclass in achieving rapid modernisation,” Pleiter remarks, noting their impressive achievements such as the launch of a new mobile app in just 11 months, 70% increases in customer satisfaction, 50% year-on-year increase in transaction volumes, as well as taking only two-three months to introduce new features n the SME app.

Looking ahead, Pleiter identifies the blend of cloud technologies, big data, and AI as crucial ingredients for future banking innovations. “Industrialised platforms like lean cores and engagement banking platforms like Backbase are here,” he observes, emphasising that these technologies enable banks to transcend outdated, siloed systems. He asserts that platforms like Backbase provide comprehensive solutions that meet all customer needs in one unified space, guiding banks through modernisation one step at a time.