Central banks worldwide expect to see a surge in global gold reserves over the next year, as a new report highlights increasing pessimism towards the US dollar.

Around 29% of central bank respondents plan to increase their gold reserves in the next twelve months, according to the 2024 Central Bank Gold Reserves (CBGR) survey. This is the highest level observed by the World Gold Council since the survey began in 2018. The planned purchases are motivated by a desire to rebalance gold holdings to a preferred strategic level, domestic gold production and financial market concerns, including higher crisis risks and rising inflation.

The ongoing geopolitical crises and volatile financial environment make gold reserves management more enticing than ever. In 2023, central banks added 1,037 tonnes of gold–the second-highest annual purchase in history–following a record high of 1,082 tonnes in 2022.

“The relatively small number of central banks (n=20) that told us they anticipate an increase in gold reserves in the next 12 months were asked about the factors influencing their decision,” the report read. “As this question has a very small number of respondents, percentages will not be meaningful. ‘Rebalancing of reserve allocations to a preferred strategic level’ is the top factor.”

These results come amidst ongoing geopolitical tensions. While global inflation is starting to cool, economic recovery is uneven, and concerns loom regarding underlying financial vulnerabilities. The report noted that interest rate levels, inflation concerns and geopolitical instability continue to be leading factors in central bankers’ reserve management decisions as they were last year.

In the UAE, the value of gold reserves of the Central Bank of the UAE (CBUAE) reached Dh17.86 billion by the end of February 2024, up 12.3% from Dh15.91 billion in February last year.

The UAE’s gold reserves significantly grew over the past years, hitting Dh12.86 billion by the end of 2020 from Dh4.04 billion by the end of 2019, and Dh1.13 billion in 2018.

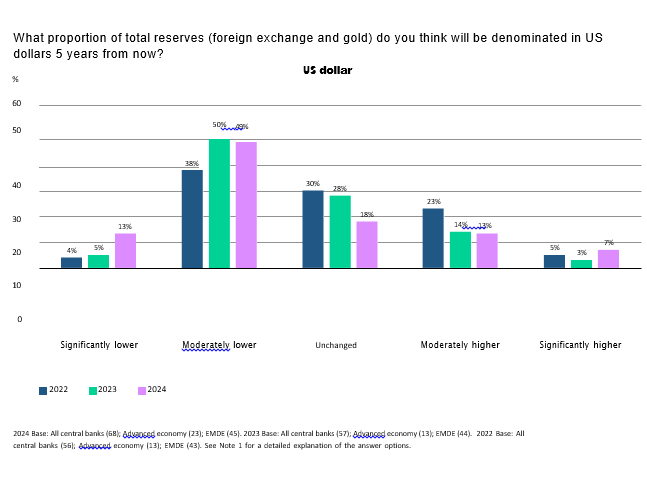

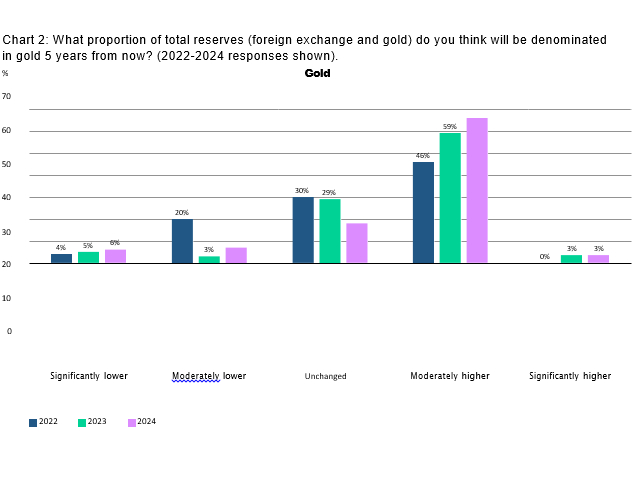

Gold’s future in global reserves

When asked about gold’s future share in global reserves, 69% of the 70 respondents surveyed, believed gold would occupy a higher proportion five years from now, up from 62% in 2023 and 46% in 2022. While 57% of advanced economy respondents think gold’s share will rise, 75% of Emerging market and developing economy (EMDE) respondents believe it will do so. Meanwhile, 35% of advanced economy respondents think it will remain unchanged five years from now, a view shared by only 9% of EMDE respondents.

A respondent was quoted saying, “Gold’s long-standing status as a reliable store of value and hedge against economic uncertainties suggests that its proportion within total reserves may remain relatively stable or experience modest fluctuations within the range of 17-25%. This dual perspective underscores the evolving landscape of reserve currencies and the enduring appeal of precious metals in safeguarding against market volatility.”

“Being a hedge against inflation, market volatility and geopolitical risks, the share of gold is expected to increase gradually if the current inflationary environment, financial uncertainty, and/or geopolitical tensions continue despite the rise in global rates.”

It is most likely that gold prices will continue their upward trajectory over the next decade due to the continued fragmentation of the world economy and expectation that the USD will weaken

World Gold Council

The World Gold Council Report noted that EMDE central banks—which have been the primary driver of gold buying since the 2008 global financial crisis—appear more pessimistic about the US dollar’s future share of global reserves and more optimistic about gold. The percentage of advanced economy respondents who believe gold’s share of global reserves will rise increased from 38% in 2023 to 57% in 2024.This highlights the trend of gold’s growing role in global reserves.

The report stated, “While EMDE central banks exhibit stronger optimism about gold’s future share of global reserves (and corresponding stronger pessimism about the US dollar’s future share), there is a notable shift in advanced economy central banks towards the same perspective.”

Overall, central banks view gold’s prospects as a reserve asset over the next twelve months slightly more favourably than last year, with 81% saying that global central bank gold holdings will rise in the next twelve months compared to 71% last year.

Contrary to the previous year, a slightly higher proportion of respondents (29%) say they have plans to increase their own gold holdings in the next twelve months. Both of these responses represent the highest level of positivity towards gold.

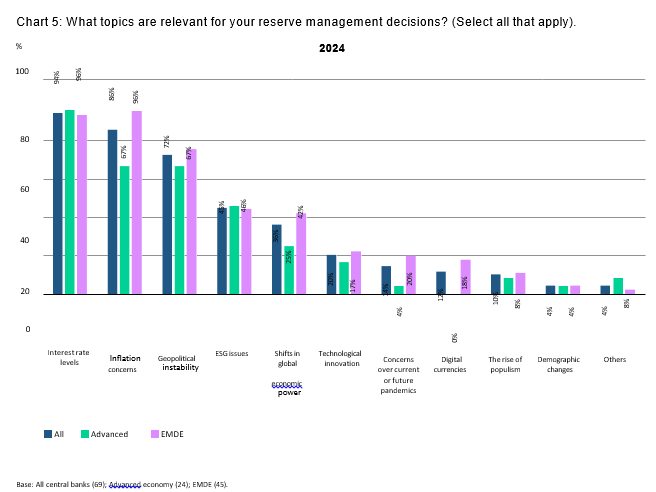

Key considerations

In 2024, 71% of respondents reported higher total reserve levels than five years ago, little changed from 69% last year. Among the factors influencing reserve management decisions, interest rate levels, inflation concerns, and geopolitical instability remain the top three factors.

A dichotomy of attitudes persists between advanced economy and EMDE central banks. While both groups were aligned on the top factor, interest rate levels, other factors resulted in split opinions. This year, 96% and 76% of EMDE central banks rated inflation concerns and geopolitical instability as relevant, while only 67% of their advanced economy counterparts did. Compared to their advanced economy peers, EMDE central banks are more concerned about shifts in global economic power.

Central bank gold holdings

The 2024 CBGR survey revealed that 83% of central banks surveyed hold gold as part of their total international reserves, consistent with previous results. While gold’s “historical position” was the top reason for holding gold in prior years, this factor dropped to fifth this year. The top reasons for holding gold are now long-term store of value/inflation hedge (88%), performance during times of crisis (82%), effective portfolio diversifier (75%), and no default risk (72%).

A higher proportion of EMDE central banks viewed the following factors as more relevant: concerns about systemic financial risks, lack of political risk, concerns about sanctions, policy tool and anticipation of changes in the international monetary system. No advanced economy respondents rated these latter three reasons as relevant. However, there is a notable convergence between EMDE and advanced economy respondents’ views towards gold. The divergence in views on factors like effective portfolio diversifier, performance during times of crisis, and highly liquid asset has narrowed significantly this year. Advanced economy central banks appear to value gold’s financial role more than in previous years.

Technical and operational considerations

Among survey respondents, 67% manage gold separately from other reserve assets, down from 83% last year. There was a corresponding increase from 8% last year to 23% this year in respondents managing gold in the investment tranche. Regarding the reasons for managing gold separately, 79% of advanced economy respondents chose “it is a historical legacy asset” as a relevant reason. 71% of both advanced economy and EMDE respondents chose “it is a strategic asset.” Meanwhile, 21% of EMDE respondents chose “different accounting regimes compared to other asset classes,” while no advanced economy respondents chose this factor. In contrast, 32% of EMDE respondents chose “liquidity requirements,” while only 7% of advanced economy respondents chose this factor.

The 2024 Central Bank Gold Reserves Survey found that 19% of central banks had used derivatives in the last year, compared to 21% last year. 29% of respondents engaged in securities lending, compared to 27% last year. In the last 12 months, 12% of central banks increased their use of derivatives, compared to 17% last year. None of the advanced economy respondents increased their use of derivatives, while 18% of EMDE respondents did so.

As central banks ramp up their gold purchases amid global economic uncertainty, the precious metal has soared to unprecedented heights, surpassing $2,400 per ounce. This surge emphasises gold’s appeal as a safe haven asset in turbulent times. For individual investors, these developments highlight gold’s potential to provide stability and preserve wealth amidst ongoing financial and geopolitical challenges. As such, the current environment makes a compelling case for considering gold as part of a diversified investment strategy aimed at weathering uncertain market conditions effectively.