With global debt levels reaching record highs, concerns are mounting about whether we are on the precipice of a debt crisis. According to studies, the global debt level in 2023 stands at $313 trillion, significantly higher than the $210 trillion recorded a decade ago. Countries like Lebanon, Russia and Sri Lanka have already defaulted on their debts, while major economies such as the US and the UK are grappling with burgeoning debt burdens.

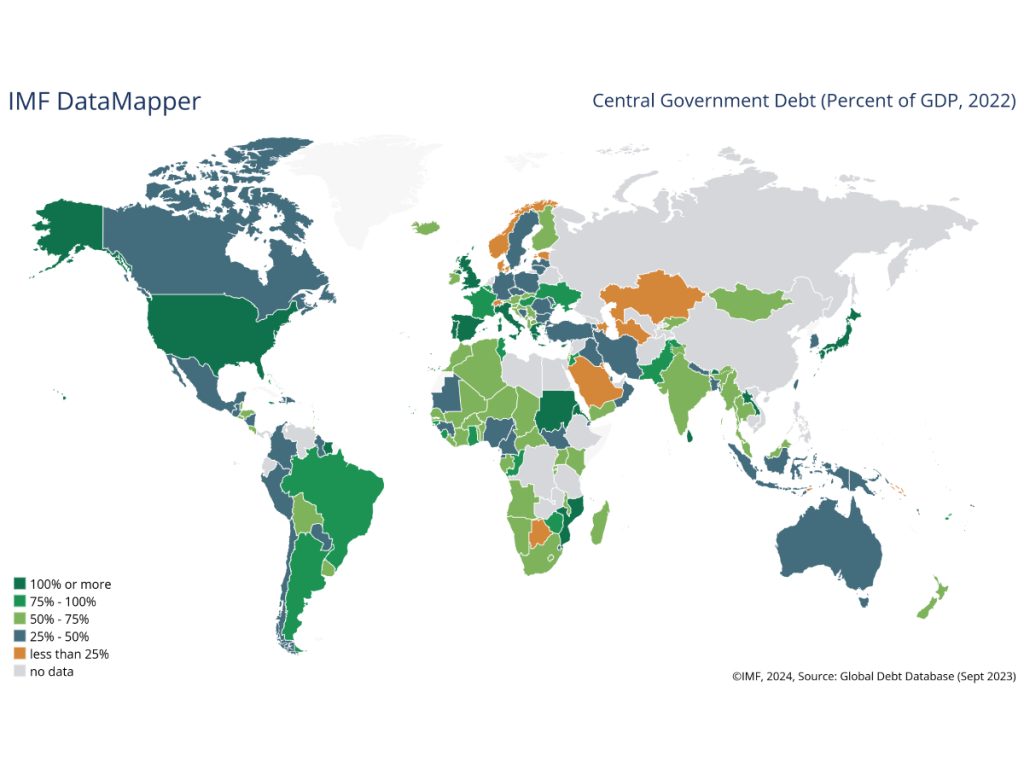

For instance, the US accumulates debt at an alarming rate of $1 trillion every 100 days, with the total debt surpassing $34 trillion as of January. Similarly, the UK’s public debt is nearing 100% of its GDP, with tax burdens at their highest since World War II. These figures paint a grim picture, raising questions about the sustainability of current debt levels.

Understanding the crisis

The origins of the current debt crisis can be traced back to the 2008 financial crisis. In response to the economic downturn, governments worldwide increased borrowing to stimulate their economies. The pandemic exacerbated the situation, forcing countries to borrow heavily to finance health infrastructure and sustain their economies. The ongoing geopolitical crises have further strained economies, leading to price inflation and rising interest rates. The combination of these factors has created a perfect storm, pushing global debt to unsustainable levels.

The burden of debt is hefty on developing countries. Unlike developed economies, which can manage their debts through domestic resources, developing countries often rely on foreign currency-denominated debt. This reliance creates a “debt trap,” where countries struggle to service their debts due to insufficient foreign currency reserves.

As a result, countries must make difficult choices between investing in essential public services and repaying their debts. For example, Nigeria spends nearly 90% of its government revenues on servicing debt, while Pakistan allocates over half of its revenues for the same purpose. This situation leads to a loss of economic and societal value as public infrastructure and services suffer due to the prioritisation of debt repayment.

The international community has recognised the severity of the debt crisis and is taking steps to address it. Initiatives such as the G20 Common Framework and the Global Roundtable for Debt aim to provide relief and find sustainable solutions to the debt problem. However, the effectiveness of these measures remains to be seen as the debt burden continues to grow.

The impact of rising interest rates

One of the most significant challenges in managing the global debt crisis is the rise in interest rates. Central banks worldwide have been forced to raise interest rates to combat inflation, making debt servicing more expensive for governments and businesses. Higher interest rates mean higher borrowing costs, which can lead to a vicious cycle of increased debt and financial instability. This is particularly concerning for developing countries, which may need help to meet their debt obligations due to rising interest rates.

According to a Brookings Institute report, the interest cost on external borrowing is, on average, three times more for developing countries than for developed countries. The think tank notes that developed countries have borrowed at interest rates of around 1% in recent years, while the least developed countries have borrowed at rates ranging from 5 to 8%. The disparity results in developing countries using a far greater percentage of their domestic revenue on interest payments.

Food inflation

Rising food prices have also contributed to the global debt crisis. The pandemic disrupted supply chains, leading to shortages and price increases for essential goods, including food. The Ukraine-Russia war has further exacerbated this issue, as both countries are major grain exporters and other agricultural products. The resulting food inflation has strained household budgets, leading to increased borrowing and debt accumulation. This has severely impacted low-income countries, where food security is already a significant concern.

A food crisis is devastating by itself: the 2008 food crisis, for example, spurred a surge in malnutrition, particularly among children. It prompted families to sell household valuables to buy food in poor countries. It prompted the poorest families to pull their children out of school, precipitating drop-out rates of as much as 50% among children from these households. But when a food crisis coincides with a debt crisis, the effects are magnified: the high debt paralyses local governments, and international assistance becomes the only way out.

Geopolitical tensions

Geopolitical tensions have also played a crucial role in the global debt crisis. The ongoing wars have disrupted global trade and led to economic sanctions, further straining the economies of the countries involved. The resulting economic uncertainty has led to increased borrowing and debt accumulation as countries seek to stabilise their economies. The impact of geopolitical tensions is not limited to the countries directly involved in conflicts; it also affects global markets and economies, leading to broader financial instability.

Solutions and future directions

Addressing the global debt crisis requires a multifaceted approach. One potential solution is debt restructuring, where countries renegotiate their debt terms to make them more manageable. This can involve extending repayment periods, reducing interest rates, or even forgiving part of the debt. International financial institutions, such as the International Monetary Fund (IMF) and the World Bank, can play a crucial role in facilitating debt restructuring and providing financial assistance to struggling countries.

The IMF and World Bank announced significant progress in global debt management at a Global Sovereign Debt Roundtable held in April 2024. They highlighted agreements on restructuring timelines and fair treatment, citing specific cases like Zambia and Ghana, with ongoing talks for Sri Lanka and Suriname. Key goals include clearer creditor coordination, faster restructuring processes, and workshops on debt sustainability and liquidity concerns.

Another potential solution is implementing economic reforms to stimulate growth and reduce dependence on borrowing. To address the debt crisis, countries must focus on both short-term and long-term solutions. Emphasising economic growth, revenue mobilisation and efficient government spending is crucial. Countries must grow their GDP faster than debt levels, raise more revenue through taxation and other means, and cut inefficient government spending. Additionally, improving debt management systems and leveraging fintech can play a crucial role in addressing the crisis.

Industry experts reckon that fintech can help by bringing more people into the formal economy, increasing the tax base and providing innovative solutions for debt management. The UAE, for example, has created a supportive ecosystem for fintech startups, which has driven economic growth and innovation. Regulatory sandboxes and open API regulations have enabled fintech companies to thrive, attracting talent and investment to the region.

The global debt crisis is a complex issue with far-reaching implications. While the situation is dire, potential solutions can help mitigate the impact of rising debt levels. Countries can navigate the challenges of the debt market by focusing on economic growth, revenue mobilisation, efficient government spending, and leveraging fintech.

As global debt continues to rise, governments, international organisations and the private sector must work together to find sustainable solutions. The future of the global economy depends on our ability to manage debt effectively and create a stable financial environment for all.