After three years of stagnation, global mergers and acquisitions (M&A) are showing signs of a turnaround in 2025, with Bain & Company projecting a rebound driven by easing interest rates, shifts in regulatory scrutiny, and companies adapting to new deal dynamics. Although global deal value reached $3.5 trillion in 2024—on par with mid-2010s levels—strategic players and financial investors are poised to drive renewed activity.

“Dealmakers who successfully navigated the recent headwinds are now better equipped to unlock value and secure growth, leveraging their refined M&A strategies,” said Les Baird, Bain’s M&A Practice Leader.

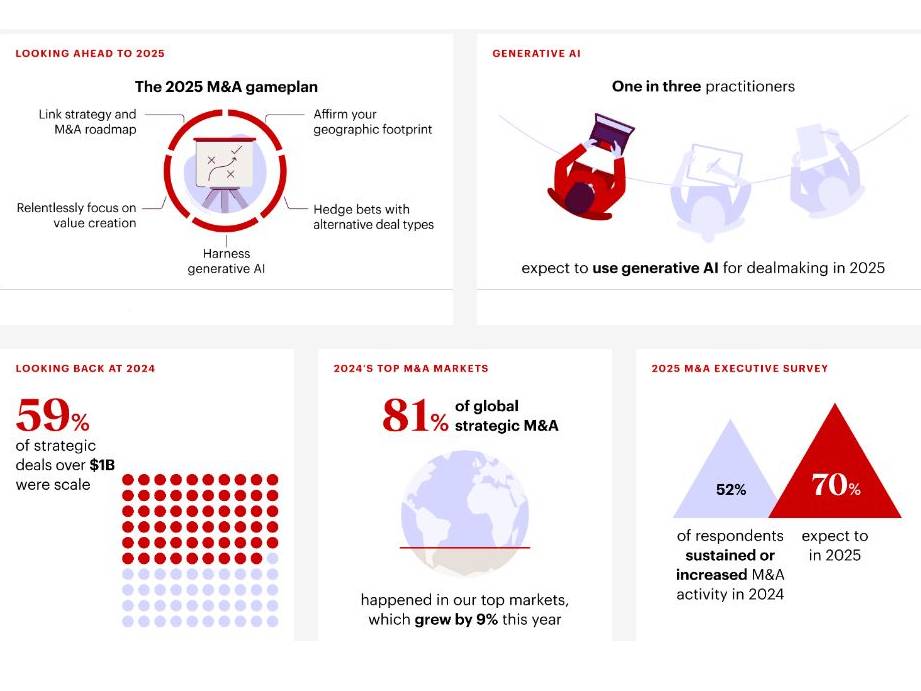

2024 in review

The past year presented significant challenges as high interest rates and stricter regulatory regimes shaped deal dynamics. Strategic M&A valuations remained low, at 10.4 times EBITDA, compared to public market valuations that hit record highs.

Despite challenges, corporate deals saw a 12% increase, and financial investors led a 29% rise in deal value year-on-year. The year also marked a return to scale deals, with 59% of strategic M&A activity focused on acquisitions that delivered both revenue and cost synergies—an adjustment driven by high fixed costs in sectors such as energy, telecommunications, and financial services.

One notable example of this shift was the $35 billion Capital One-Discover merger, which combined scale efficiencies with new revenue streams. Similarly, the proposed $14 billion Juniper Networks deal by HPE highlighted the demand for top-line and bottom-line growth.

Energy leads, technology lags

Energy and natural resources outperformed, with more than 10 megadeals valued above $5 billion in 2024, including notable transactions like ONEOK’s $2.6 billion acquisition of Medallion Midstream. In contrast, technology—a traditional M&A powerhouse—remained subdued due to elevated valuations and regulatory constraints.

Healthcare and life sciences also underperformed compared to their pre-pandemic highs, as companies in these sectors struggled with tighter financing conditions and ongoing regulatory hurdles.

Regulatory challenges shift deal strategies

Nearly 50% of global executives cited regulatory scrutiny as a major factor influencing deal strategies in 2024. Companies employed different tactics to address this, including pre-emptive antitrust evaluations and alternative deal structures. This led to the barbell effect: small, under-the-radar deals thrived, while megadeals above $5 billion dominated the upper end of the spectrum.

Bain’s survey of 300 M&A practitioners highlighted that smaller deals accounted for 95% of total activity. However, megadeals like Mars’ $36 billion acquisition of Kellanova in consumer products and the $34 billion Synopsys-Ansys combination in technology propped up overall deal value.

Generative AI in M&A

The report stressed the growing role of generative AI in dealmaking, with early adopters using AI to improve sourcing, screening, and due diligence processes. One in five companies reported using generative AI in their M&A workflows, with 60% of private equity firms deploying AI tools to streamline decision-making and integration.

Companies leveraging generative AI saw faster deal closures and higher-value outcomes, positioning them ahead of competitors that are slow to adopt these tools. “Those that fail to integrate AI risk losing out on good deals and misjudging valuation opportunities,” the report noted.

2025 outlook

The report identifies three primary forces that will shape M&A activity in 2025:

- Technology disruption: Generative AI, automation, and quantum computing will drive non-tech and tech companies to acquire innovation capabilities.

- Post-globalisation dynamics: With shifting trade policies and supply chain realignments, companies are expected to pursue strategic deals to secure market access and operational resilience.

- Shifting profit pools: Media companies, for instance, will continue acquiring content to compete against tech giants, while consumer product leaders will divest non-core brands to focus on scalable, profitable segments.

Game plan for companies

Bain recommends that companies focus on pressure-testing their M&A roadmaps against market realities, leverage AI for faster deal execution, and explore alternative deal structures like joint ventures and minority stakes when outright acquisitions are not feasible.

Strategic dealmakers will need to act decisively. As Baird stated, “The winners in 2025 will be those who seize the opportunity to deploy capital at scale while others remain cautious.”

With an easing of macroeconomic constraints, M&A practitioners are optimistic that deal activity will return to historical highs, fueled by a more favourable environment for value-driven transactions.