Institutional investors have poured record capital into private markets in search of higher yields and lower correlations, but that shift has come with a cost: reduced liquidity, delayed valuations, and growing exposure to market stress with limited real-time pricing. As private credit and other alternatives grow into a $30 trillion asset class by the end of the decade, the need for reliable shock absorbers within these portfolios is becoming more urgent.

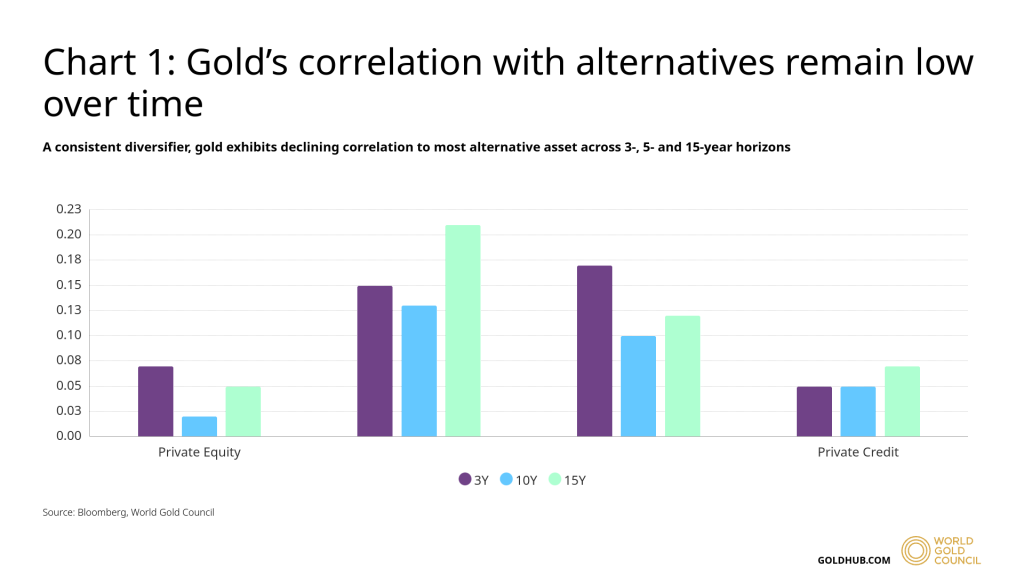

Gold, often overlooked in strategic allocations, is starting to find a more defined role alongside alternatives. While not always classified as an alternative asset, gold behaves like one when it matters most. It offers liquidity when private capital is locked, acts as a hedge during credit market dislocations, and remains lowly correlated with both traditional and alternative investments.

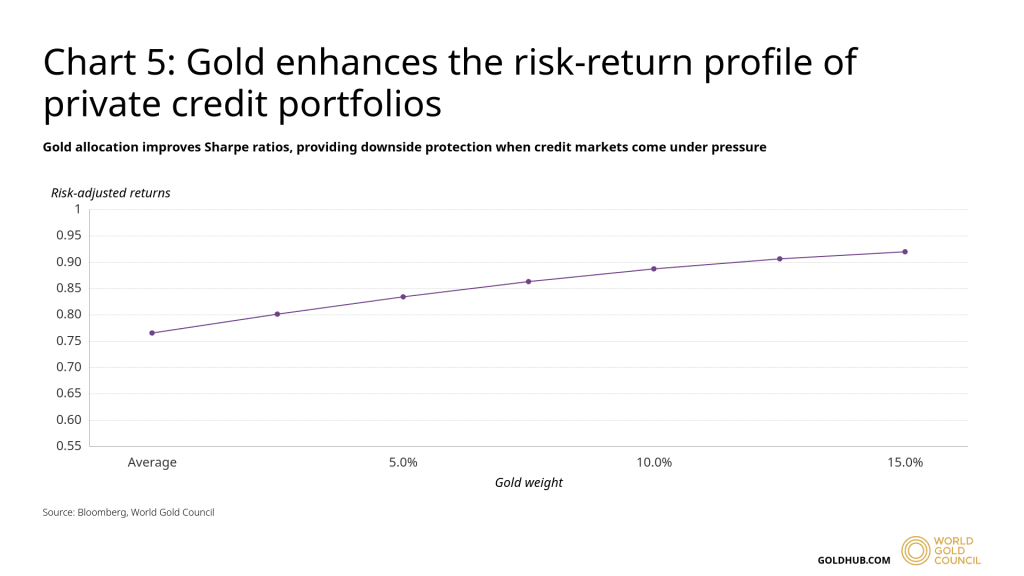

Recent stress scenarios, from the global financial crisis to Covid, revealed the limitations of private markets when liquidity dries up and exit timelines stretch. In each of those episodes, gold maintained its value and remained accessible, while private equity and credit faced markdowns and delayed realisations. New data from the World Gold Council and Bloomberg suggests that a strategic allocation of just 5–8% gold in a diversified alternatives-heavy portfolio improves risk-adjusted returns and cushions drawdowns by up to 90 basis points.

Now, as regulatory changes like Basel IV push more credit risk out of the banking system and into private lenders, and as general partners turn to continuation funds and secondary sales to navigate exit slowdowns, investors are increasingly reassessing their liquidity buffers. For some, gold is becoming the asset that fills that gap, a defensive anchor that can trade in size when other assets can’t.

Correlation drift and the liquidity gap

Over the past decade, the correlation between equities and bonds, the foundation of the traditional 60/40 portfolio, has started to break down. Since 2022, those correlations have turned positive, weakening their diversification effect. In response, institutions have shifted further into private equity, private credit, hedge funds, and real assets to stabilise returns.

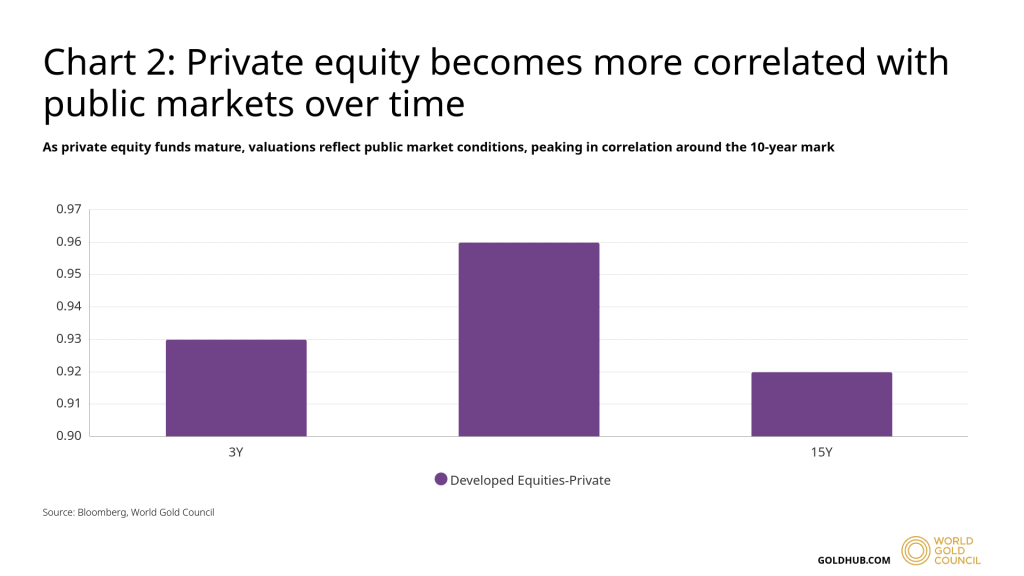

But alternative assets come with liquidity constraints. Private credit, for instance, locks capital for five to ten years, and valuation marks often lag economic reality. During periods of stress, such as Q4 2018 or the early months of the pandemic, exit windows shut, fundraising slowed, and managers had to rely on mechanisms like continuation vehicles to extend holding periods.

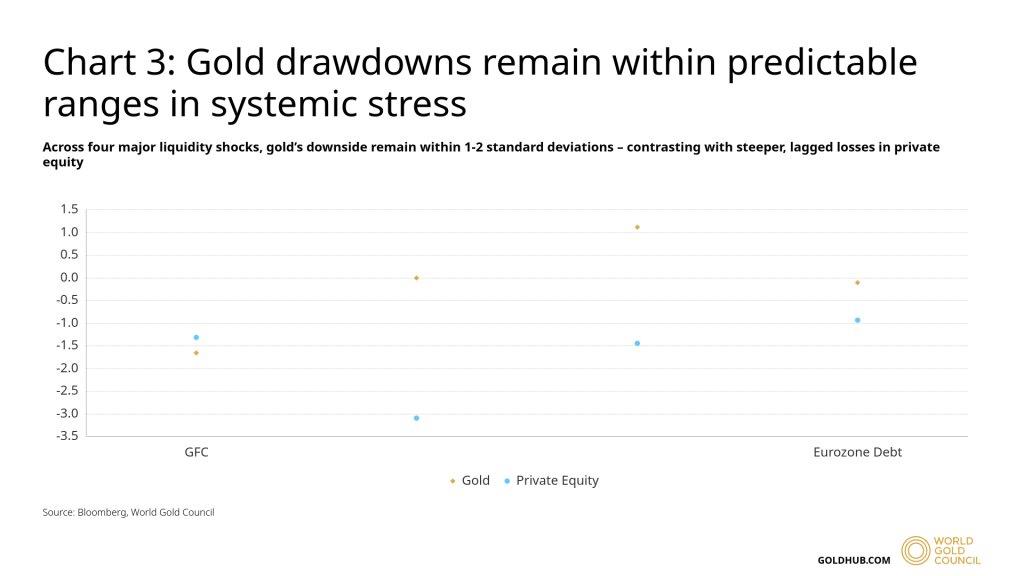

Gold, by contrast, remained liquid and responsive across each of those periods. World Gold Council data show that during four major systemic shocks, the global financial crisis, the Eurozone debt crisis, the Fed’s tightening in 2018, and the 2020 Covid crash, gold’s returns stayed within one to two standard deviations of its historical range. Private equity returns, on the other hand, were more volatile and took longer to reflect the stress.

Optimising for resilience

In a Monte Carlo simulation based on 20 years of historical data, a diversified portfolio with an 8% allocation to gold yielded higher risk-adjusted returns and lower maximum drawdowns compared to a gold-free equivalent. Across 20-, 15-, and 5-year timeframes, gold reduced annualised volatility by roughly 80 to 120 basis points while marginally improving returns.

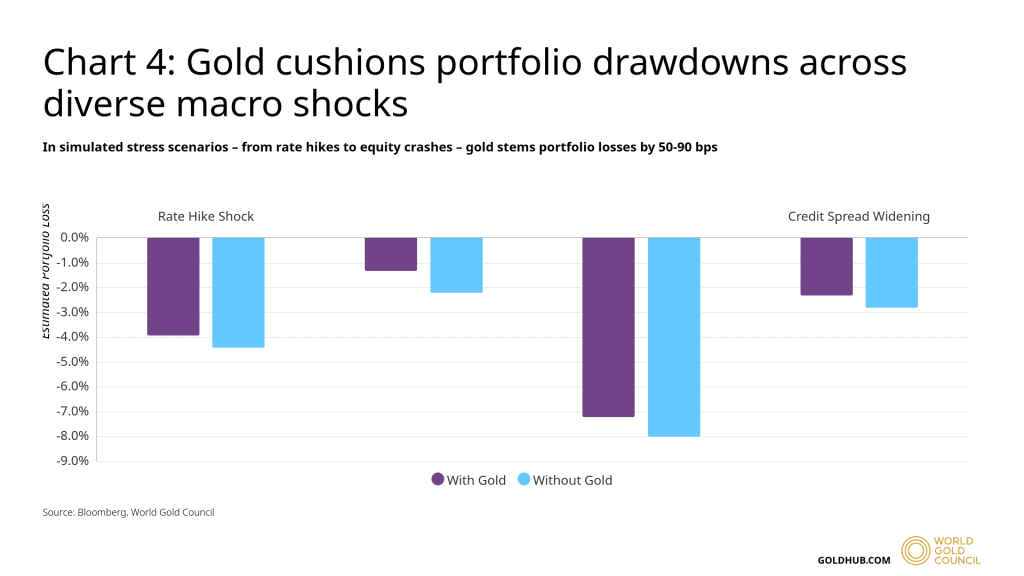

The effect was most pronounced in scenarios involving liquidity stress or macroeconomic shocks. When modelled against four simulated events, equity crash, inflation spike, rate shock, and credit spread widening, gold improved downside protection by 50 to 90 basis points across each case.

These results underline a structural point: gold is less about return enhancement, and more about portfolio resilience. As private market exposures rise, investors are using gold to maintain flexibility, especially when other hedges, such as government bonds, underperform.

Private credit meets Basel IV

Private credit, once a niche allocation, is now a core holding for pension funds, sovereign wealth funds, and insurance companies. As banks face stricter capital requirements under Basel IV, more lending activity, particularly in SMEs, real estate, and special situations, is shifting into private hands.

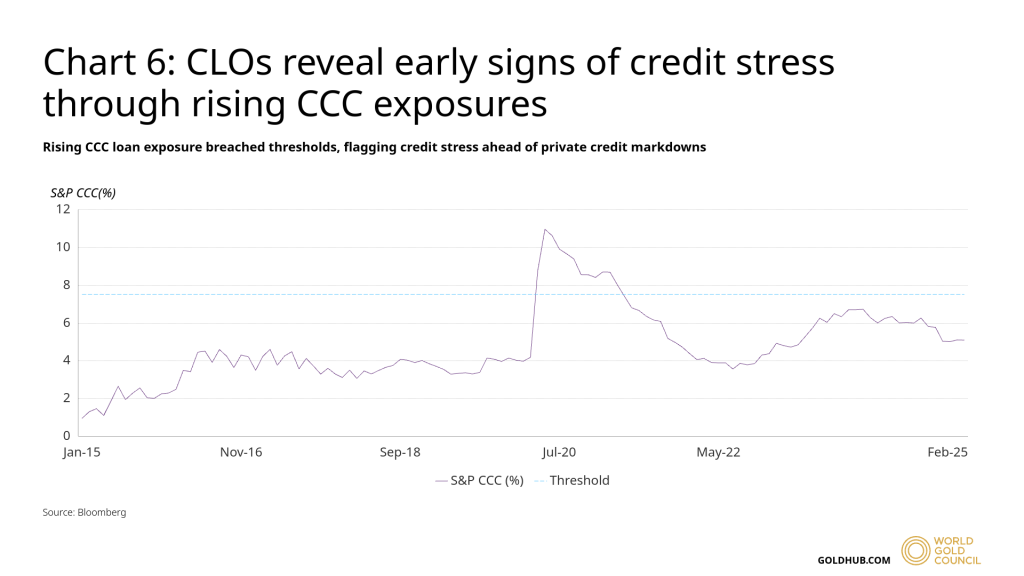

But with that growth comes higher sensitivity to credit cycle dynamics. Pricing lags, quarterly NAVs, and limited transparency can obscure stress signals. To bridge that gap, some investors are tracking indicators from public leveraged credit markets, including CLO metrics such as CCC-rated exposures and junior overcollateralization, as proxies for early warnings.

During the Covid-19 sell-off in 2020, CCC exposures in CLOs spiked before private credit funds marked down values. PitchBook data shows private lending strategies posted a 6.2% drop in Q1 2020, the steepest quarterly decline since 2008. Yet even that lagged public credit losses by weeks, reinforcing the role of gold as a source of immediate liquidity when redemptions or capital calls arise.

Bridging public and private with gold

Investors are no longer separating public and private markets, they’re viewing them along a continuum of liquidity, return, and volatility. In that framework, gold is becoming a bridge asset. It doesn’t behave like private equity or credit, but it helps address the liquidity gap that those assets create.

In 2024, GP-led secondaries accounted for 46% of total secondaries volume, up from 24% in 2016. These continuation funds offer breathing room, but they don’t eliminate the pressure to return capital. In a slower exit environment, gold is emerging as a buffer that buys managers time, avoids forced sales, and preserves long-term investment strategies.

As portfolios grow more complex and liquidity premiums stretch further, gold offers a practical utility: real-time pricing, deep liquidity, and historical performance that holds up under stress. For asset owners balancing return goals with drawdown management, that role is likely to expand.