Global harmonisation of Islamic finance principles could smooth the process of issuing sustainable sukuk to fund climate change mitigation measures in core markets.

While Islamic and sustainable finance have common features, they are distinct. There are parallels between the objectives of sustainable finance and some of the underlying principles of Sharia, particularly with respect to climate transition and sustainable development. The core principles of Islamic finance call for the creation of a sustainable, stakeholder-focused, and socially responsible financial system. Islamic finance must abide by the objectives (Maqasid) of Sharia, which broadly revolve around the protection of faith, life, mind, wealth, and dignity.

In many respects, we believe these overlap with sustainable finance’s focus on integrating sustainability objectives into investment decision-making. They also consider the longer-term economic sustainability of the organisations being funded. Furthermore, they help show the role and stability of the overall financial system in which they operate as defined by the International Capital Market Assn. (ICMA).

Both Islamic and sustainable finance include principles to review the allocation of proceeds from issuance. Tracking the allocation of proceeds to eligible projects is a principle we also observe for sustainable bonds and loans, specifically use-of-proceeds ones. Sharia requires that tangible and identifiable assets back Islamic finance transactions.

There are different approaches to developing Islamic sustainable finance in different markets. The GCC’s development is rather bottom-up, particularly from leading regional financial institutions and corporates. First Abu Dhabi Bank, for example, aims to facilitate up to $135 billion of sustainable financing by 2030. We also saw an increase in conventional and Islamic sustainable bond issuances—mostly green issuances—by GCC issuers in 2023. This trend is supported by local regulators. For example, in June 2023, the UAE’s Securities and Commodities Authority announced an exemption from registration fees for companies that list their sustainable bonds or sukuk in the local market during 2023.

We expect the Islamic finance industry to continue expanding through 2024. In our view, the GCC countries, particularly Saudi Arabia, will support industry growth in the next 12-24 months. This is partly thanks to the implementation of Vision 2030, which will likely create additional growth opportunities for the Saudi banking system and the sukuk market.

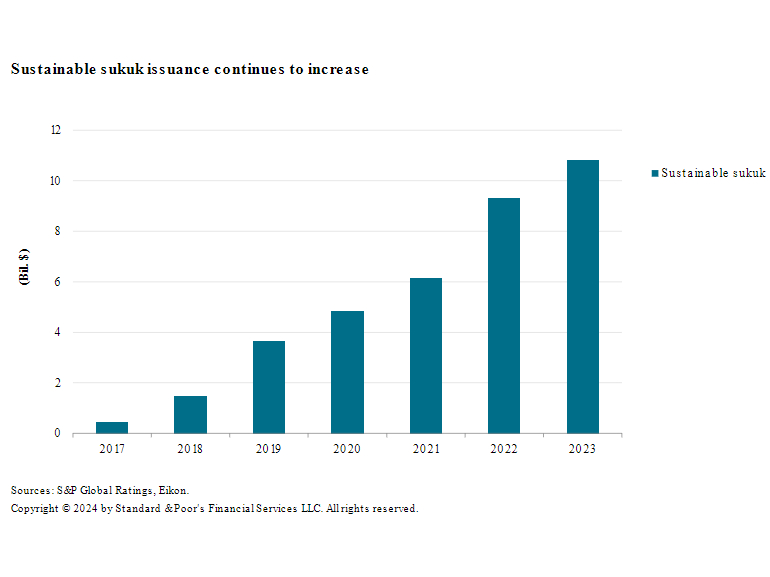

Sustainable finance issuance is increasing in the core Islamic finance countries. In these core countries, the volume of sustainable sukuk reached $10.8 billion at year-end 2023, compared with $8.0 billion for the same period in 2022.

Islamic finance is concentrated in oil-exporting countries, many of which have established strategies to diversify their economies and reduce their carbon footprints. As such, opportunities are significant and could take the form of sustainable finance issuance (both conventional and sukuk) and financial products offered by financial institutions. We expect that climate transition and similar sustainability objectives will be the primary focus of these instruments.

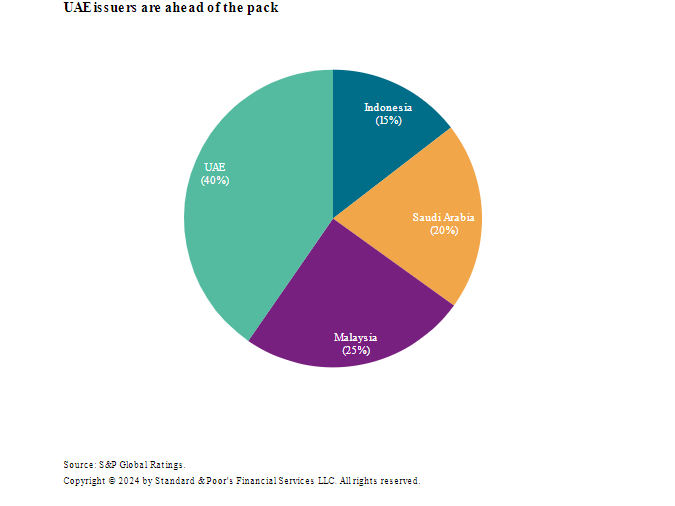

Issuers in Saudi Arabia and UAE contributed around 60% of sustainable sukuk issuance in the industry’s core countries in 2023. We expect to see more issuance from these two countries because of the implementation of Saudi Vision 2030 and, more generally, GCC governments’ commitments to diversify and enhance the sustainability of their economies, which will create opportunities to tap into the sustainable bond and sukuk markets. Therefore, Islamic finance will play an important role in the climate transition, in our view, despite the small size of the industry overall.

We believe that one of the main factors holding back sukuk and Islamic finance is the increased complexity compared with conventional instruments. The sukuk issuance process is more time-consuming than bonds, and differences in the interpretation of Sharia can add to the complexity.

In late 2023, the AAOIFI published its exposure draft of Sharia standard 62 on sukuk. If it is adopted, Sharia standard 62 could have a significant effect on the sukuk market. Among others, the standard requires that the ownership and the risks related to the underlying assets are transferred to sukuk holders. This could weaken sukuk sponsors’ contractual obligations if repayments become dependent on the performance of the underlying assets, their market value, or the sukuk holders’ decision to sell these assets to third parties. As a result, some conventional fixed income investors might shy away from the sukuk market, which could change the pricing dynamics of such transactions to account for potential additional risks.

At this stage, it is hard to tell whether Sharia standard 62 will be revised and how countries that adopted AAOIFI standards may react to the potential disruption of their sukuk markets. Another potential outcome of Sharia standard 62 could lead to a higher fragmentation of the sukuk market and a more pronounced difference between adopters and non-adopters of the standard. Even if the standard is approved this year, its implementation may be deferred to the following years, which could cause a rush into sukuk before the standard’s adoption.

Overall, harmonisation could make the issuance of sustainable sukuk more straightforward and available as a potential financing option for investors less familiar with Islamic finance. Robust oversight of the final use of proceeds raised from sustainable sukuk may strengthen the integrity of this small but expanding market. Leveraging technology could also play a role.