The United Nations has approved a major overhaul of the global statistical framework used to measure economic activity, incorporating digital technologies, artificial intelligence, and crypto assets for the first time. The sixth revision of the System of National Accounts (SNA) was adopted unanimously by the UN Statistical Commission in March, despite rising geopolitical tensions. It will guide how countries report key metrics such as output, income, investment, and national wealth.

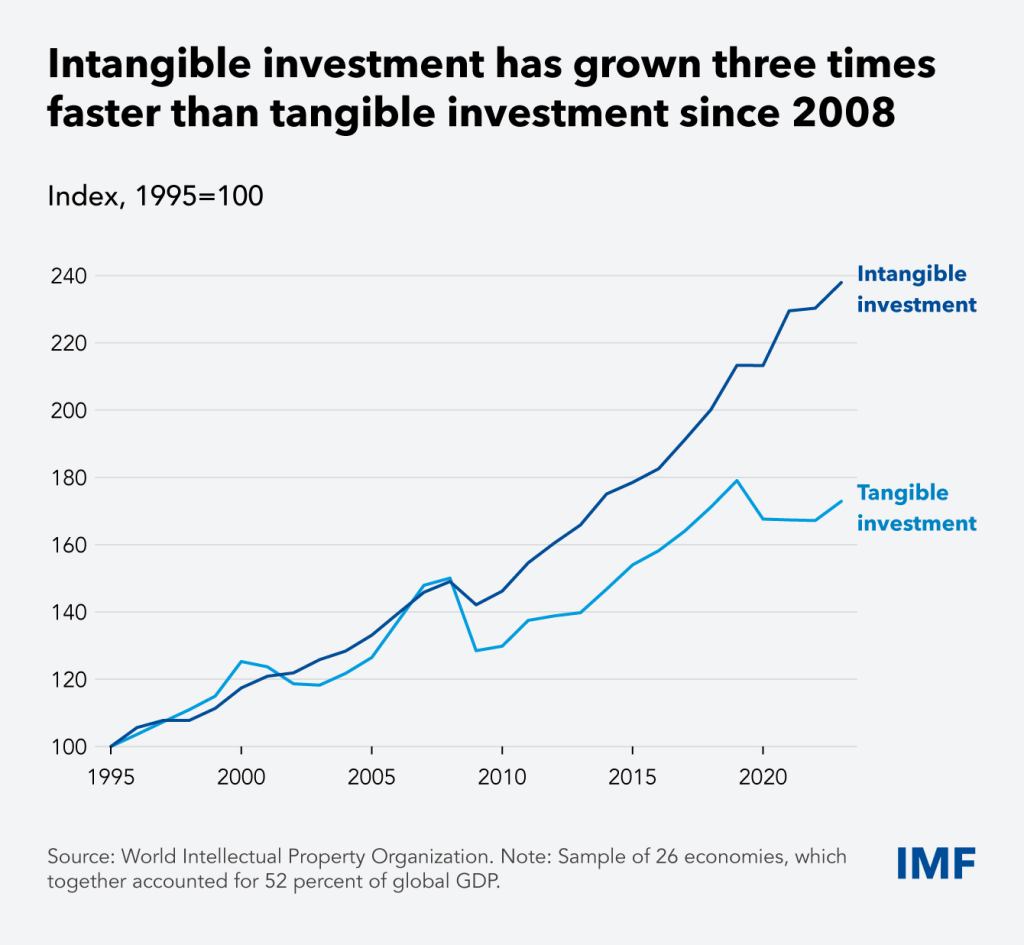

Led by the IMF, UN, World Bank, European Commission, and OECD, the update brings the nearly 90-year-old framework in line with modern economies increasingly driven by intangible and digital assets. The revision reflects concerns that the current system is lagging behind the rapid transformation of the global economy, which now includes $114 trillion in GDP and a growing share of digital activity that was previously underreported or misclassified.

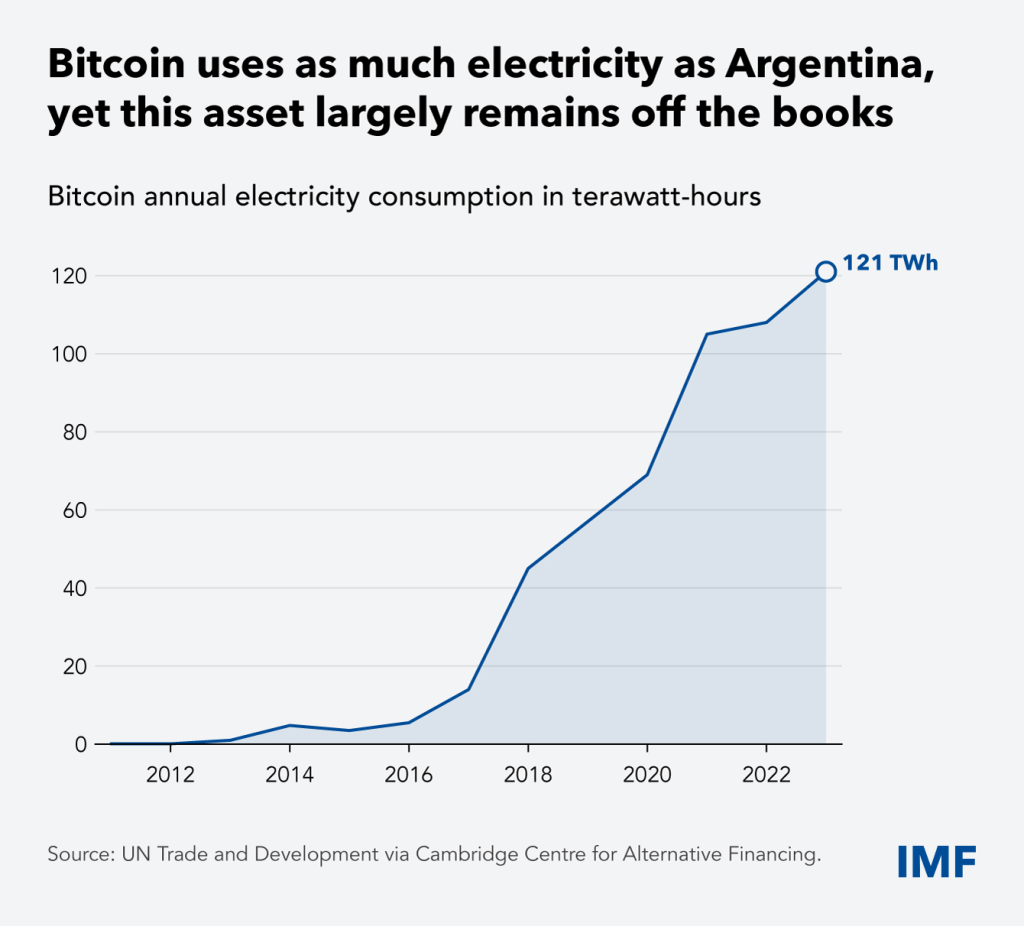

Among the most significant additions is formal guidance on how to classify and record crypto assets. Bitcoin and similar tokens have had a measurable economic impact, particularly in terms of energy use, but have historically fallen outside traditional measures like GDP. The updated framework now defines certain crypto assets as “non-produced nonfinancial assets” and includes them in national wealth calculations.

The revision also addresses other digital sectors. It recommends that countries report new indicators on AI, cloud computing, e-commerce, and digital platforms, and introduces a standard definition of artificial intelligence to ensure consistent measurement across national accounts. The aim is to capture economic contributions that have previously been missed or underestimated, particularly relevant given weak productivity growth in some economies despite widespread digital adoption.

Another major element of the update is a deeper focus on financial risks and cross-border corporate activity. In response to lessons from the 2008 global financial crisis, the new standards call for improved classification of financial instruments and liabilities, especially among non-bank financial institutions. They also aim to better account for multinational firms’ production and profit allocation, particularly where design, branding and IP are held in one country while manufacturing is outsourced elsewhere.

The IMF said these changes are intended to future-proof economic data, making it more relevant for fiscal and monetary policy. For instance, measuring net domestic product (NDP), which subtracts both depreciation and natural resource depletion, offers a more sustainability-focused metric. In resource-rich economies, the impact on reported national output could be significant.

Implementing the updated standards by 2029–2030 will require substantial resources from national statistical offices. The IMF plans to provide guidance, technical assistance and training to help countries align their systems with the new framework.

The overhaul comes at a time when governments face growing pressure to track digital, intangible, and cross-border economic activity more accurately. Without these updates, policymakers risk making decisions based on incomplete or outdated information.