In September 2024, gold experienced notable growth, marking its third consecutive month of gains, according to the latest report by the World Gold Council. The metal posted a 4.6% increase, finishing the month at $2,630 per ounce. This surge in price followed similar strong performances in July and August, pushing gold to achieve new highs on eight separate occasions throughout the month, with the peak recorded on September 26. Despite a marginal decline toward the month’s close, gold maintained a robust upward trajectory.

Key to this rise was a combination of macroeconomic shifts and geopolitical events. The most significant influence came from the US Federal Reserve’s decision to cut interest rates by 50 basis points, an unexpectedly large reduction that triggered widespread movement across financial markets. A weaker US dollar, resulting from the Fed’s decision, amplified the attractiveness of gold as a store of value. In addition, ongoing geopolitical tensions created further demand for gold as investors sought safer assets amid rising uncertainty.

Price drivers

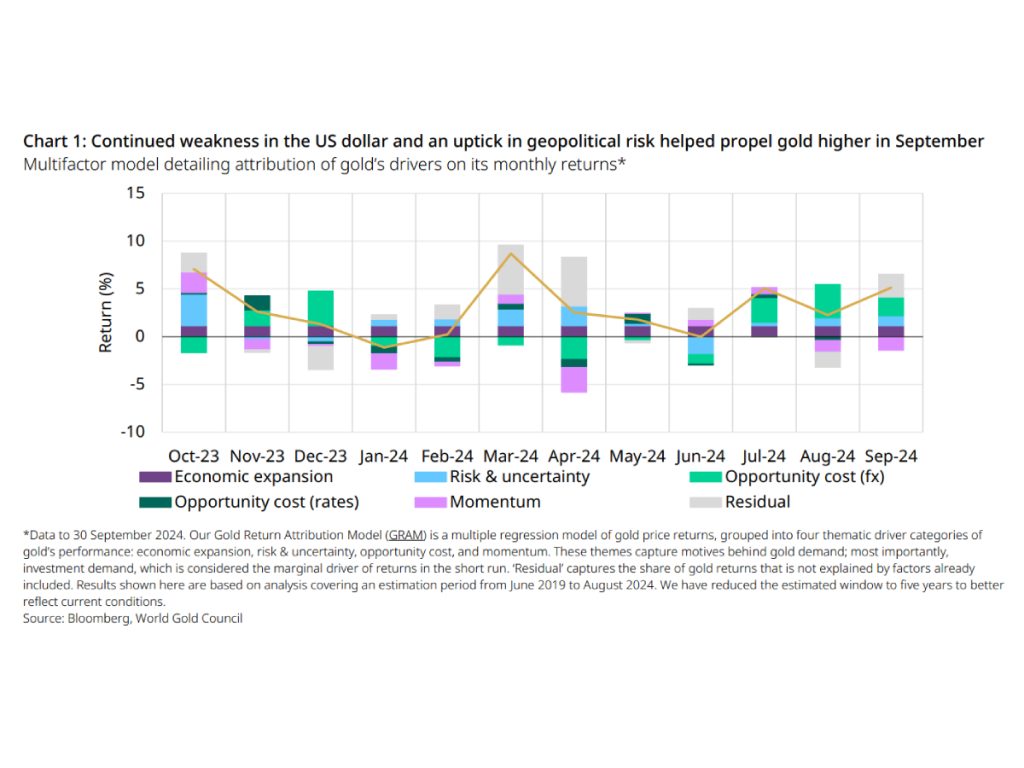

Gold’s price movements in September were closely analysed using the Gold Return Attribution Model (GRAM), which breaks down the factors influencing the metal’s returns. These factors fall under four main categories: economic expansion, risk and uncertainty, opportunity cost, and momentum. Each category reflects different elements of gold demand, but short-term movements are often driven by investment demand, which responds to shifts in these underlying themes.

A critical driver in September was the opportunity cost of holding gold. The 50bps rate cut by the US Federal Reserve directly impacted bond yields and reduced the opportunity cost of non-interest-bearing assets like gold. Lower yields on bonds make gold more attractive to investors, particularly those looking for a hedge against market volatility. This rate cut, coming earlier and more aggressively than many analysts anticipated, signalled a pivot by the Federal Reserve towards a more accommodative monetary stance. As a result, the US dollar weakened, providing further upward pressure on gold prices, as gold is priced in dollars and becomes more affordable for non-dollar buyers when the currency declines.

Additionally, geopolitical risk played a crucial role in pushing up gold prices. The ongoing instability in the Middle East throughout September, which escalated into October, increased demand for safe-haven assets. Historically regarded as a hedge against uncertainty, Gold saw increased buying from investors concerned about the broader impact of these geopolitical tensions on global markets.

Role of momentum and ETFs

Another important factor influencing gold’s performance in September was momentum. Momentum, in this context, refers to the tendency of past performance to influence current demand. According to GRAM, gold’s strong return in August exerted pressure on the market in September, creating a situation where the previous month’s high returns placed downward pressure on new investment. Historically, periods of strong returns often lead to a slight pullback in subsequent months, as markets tend to self-correct. However, this momentum effect was largely offset by the positive impacts of the weakening dollar and heightened geopolitical risk, allowing gold to sustain its upward trend.

In addition to these factors, global demand for physically-backed gold exchange-traded funds (ETFs) contributed significantly to the metal’s rally. September marked the fifth consecutive month of inflows into gold ETFs, with North American funds accounting for the largest share of these investments. This sustained inflow of institutional money into gold funds reinforced the metal’s position in global portfolios, particularly as investors sought to protect against inflation, currency risk, and the uncertain geopolitical landscape.

Macroeconomic environment

The broader macroeconomic environment in 2024 has been conducive to gold’s strong performance. Over the past two years, bonds and equities have become increasingly correlated, a trend that diminishes the traditional diversification benefits of these asset classes. Historically, bonds and equities have moved in opposite directions, allowing investors to balance risk across their portfolios. However, as correlations between the two asset classes increase, the overall risk in portfolios rises, making alternative assets like gold more attractive as hedging tools.

According to the Gold Market Commentary, the rise in equity-bond correlations and lower yields suggest that a “gold-friendly” environment is emerging. Lower bond yields make holding gold more appealing, while the rising risk associated with equities and bonds encourages investors to seek safer assets. This macroeconomic backdrop has led to a growing interest in gold as a diversifier and a hedge against market instability.

Outlook

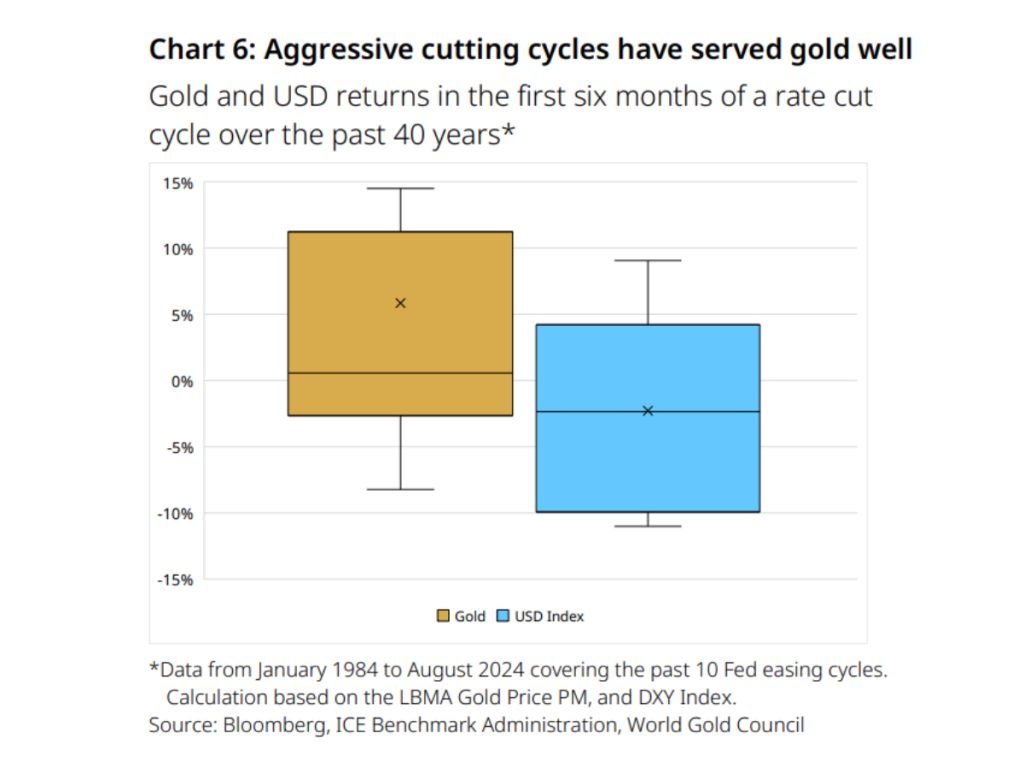

Looking at historical data, aggressive rate-cutting cycles have often been beneficial for gold. In the past ten easing cycles initiated by the Federal Reserve, gold has seen average returns of 6% in the six months following the start of rate cuts. September’s jumbo 50bps rate cut was the first in the current cycle, and if historical patterns hold, gold could see further gains in the coming months as the full impact of lower rates becomes apparent across global markets.

In addition to favourable interest rate conditions, gold’s position is strengthened by central bank purchases. Over the past several years, central banks, particularly in emerging markets, have increased their gold reserves, seeking to diversify their holdings away from traditional currencies and other financial assets. Central bank buying acts as a stabilising force for the gold market, providing sustained demand even when other sources of demand, such as jewellery or industrial uses, may fluctuate.

Another important factor is the return of Western ETF investors, who have been steadily increasing their exposure to gold. This renewed interest, combined with rising demand from key markets like India and ongoing geopolitical risks, suggests that gold is well-positioned to benefit from evolving market conditions in the near future.