Lower local currency issuances in core Islamic finance countries caused global sukuk issuance to drop by almost 15% in the first half of 2025 to $101.3 billion, from $119.0 billion at midyear 2024. We expect local currency issuance to remain subdued, mirroring the liquidity conditions in some core markets and lower financing needs due to good fiscal performance. In contrast, foreign currency issuance increased to $41.4 billion from $38.0 billion. Therefore, we continue to expect $70 billion-$80 billion in foreign currency-denominated issuances in 2025.

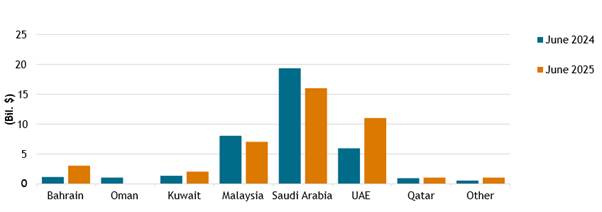

Foreign currency-denominated issuances increased by 9% in H1 2025. This was underpinned by strong issuances in the UAE, Bahrain, and Kuwait, while in Saudi Arabia (KSA) we observed a small decline in issuance (see chart 1). This increase is despite the volatility in international capital markets that followed the announcement of tariffs by the U.S. government and slower-than-initially-expected monetary easing. Significant financing needs in core Islamic finance countries supported sukuk issuances, as well as lower oil prices and fiscal deficits.

In H1 2025, issuers tapped into opportunities to go to market. In KSA, where issuers contributed 38.9% of market volume, we saw a lot of issuances from banks as they continue to support the financing of the government’s Vision 2030 initiatives. In the UAE, where issuance volume notably increased, banks and corporates tapped the market to finance growth amid a still-supportive economy. We expect performance in H2 2025 to depend on the evolving regional geopolitical landscape. However, since we don’t expect a full-scale regional war, resilient foreign currency issuance trends in the first half will likely continue, supported by the Fed’s expected reduction in interest rates. Therefore, we maintained our full-forecasts for foreign currency-denominated issuances at about $70 billion to $80 billion.

Chart 1: Foreign currency-denominated sukuk issuance increased by $3.4 billion

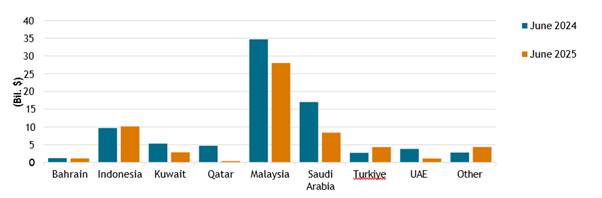

Local currency-denominated issuances plummeted in the H1 2025 to $59.8 billion, down from $81.0 billion a year earlier (see chart 2). This was neither directly related to U.S. tariffs, the global market volatility, nor the escalation in geopolitical risk in the Middle East. It was instead due to lower local currency issuances in some core Islamic finance countries, particularly Malaysia, KSA, Qatar, and the UAE, mirroring the liquidity in some core markets and lower financing needs due to good fiscal performance in others. For example, we have seen a significant drop in local currency issuances in KSA, where banks’ liquidity is being channelled into financing Vision 2030, leading to lower issuances from the government. We expect the drop in local currency issuances to continue.

Chart 2: Local currency-denominated sukuk issuance plummeted by $21.2 billion

The total volume of sustainable sukuk issuance increased by 27% in the first half of 2025, reaching $9.3 billion compared with $7.4 billion in 2024. Banks, including the Islamic Development Bank (IDB), accounted for almost 50% of this performance, followed by some Gulf Cooperation Council (GCC) and Malaysian corporates. It is also worth noting that Saudi Arabian issuers accounted for more than 60% of sustainable sukuk issuances in the first half of the year. This trend can be explained by the alignment between Islamic finance and sustainability, the significant role of IDB in Islamic sustainable financing, along with the high financing needs of Saudi banks.

Given the strong performance in the first half of the year, we have slightly revised upward our forecasts for the volume of sustainable sukuk issuance for the full year to $14 billion-$16 billion. We expect issuance to increase further if we see an acceleration in the climate transition journey of GCC issuers, as well as regulators offering incentives to go down the sustainable route.

In April 2025, the AAOIFI announced that its Sharia board will amend the proposed Standard 62 following industry comments. The key question remains whether Standard 62 will require asset ownership to effectively pass to investors, and if so, would this change sukuk holders’ mechanisms of recourse in a default. We continue to believe that the appetite for sukuk with real transfer and full asset recourse remains limited. In our view, if sukuk holders are given the option to register the asset in their name, this could lead to sukuk being considered as a secured obligation, reducing the protection of other unsecured creditors. This could lower the creditworthiness of unsecured instruments and leave them at a disadvantage.

The AAOIFI did not specify which changes the board intended to introduce or the timeline for the project, and the implementation process remains uncertain. This means that it is now difficult to determine the implications of adopting the new standard on market performance. The need to issue before its adoption may also abate since issuers and investors no longer perceive the disruption as imminent.