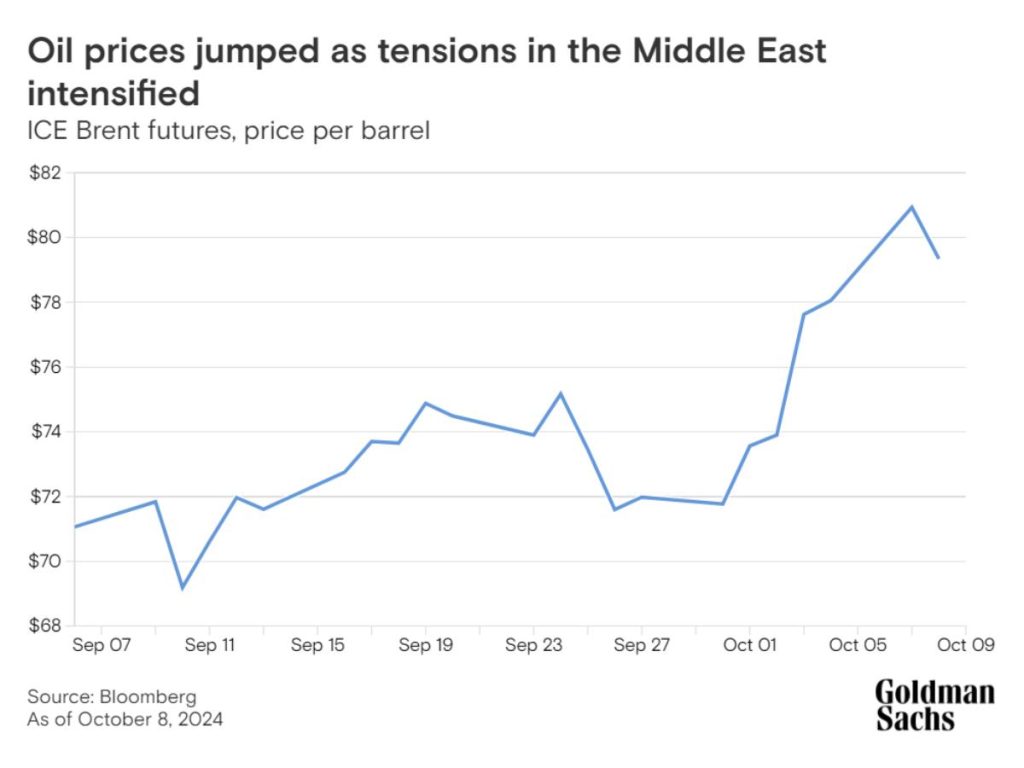

Goldman Sachs has projected a potential rise in oil prices, driven by escalating geopolitical tensions and broader economic shifts globally. The latest analysis highlights that geopolitical risks, supply disruptions, and economic factors could create significant upward pressure on oil, while gold is also positioned for growth amid central bank actions and macroeconomic uncertainties.

Middle East conflict heightens supply risk

The core concern in the oil market is the potential for supply disruptions following the recent missile attacks in the Middle East. According to Daan Struyven, Co-head of Commodities Research at Goldman Sachs, the oil market has not yet seen physical supply reductions despite the ongoing conflicts. However, the market is increasingly focused on the possibility of disruptions to key oil infrastructure, particularly in Iran.

“The big question is whether we are going to see any actual disruptions to supply in the Middle East,” Struyven noted. He added that while significant spare capacity exists, with six million barrels per day (bpd) of production shut in, any supply shock—especially from Iran—could lead to a substantial spike in oil prices. The report suggests that a disruption of two million bpd from Iran for two quarters could push Brent crude prices to between $85 and $95 per barrel.

The risk is amplified by the possibility of attacks on critical infrastructure like the Strait of Hormuz, which handles about 20% of the world’s oil supply. A blockage or significant disruption at the Strait could drive oil prices into triple digits. “If you cannot get the Saudi or Emirati barrels out of the Middle East to the rest of the world, then the upside is highly significant,” Struyven explained.

OPEC’s role in mitigating market tightness

OPEC’s ability to mitigate supply losses is a key factor influencing the oil market. An analysis from Goldman Sachs points out that countries like Saudi Arabia and the UAE, which hold more than four million bpd of spare capacity, have historically stepped in to offset supply disruptions. “Historically, they have offset about 80% of lost supply within two quarters, but the production recovery tends to be slower than the disruption,” Struyven said. This delay could lead to tighter market conditions and elevated prices until OPEC’s actions bring the market back into balance.

The analysis also highlighted the challenge of deploying spare capacity if the infrastructure that allows oil to be transported out of the region is compromised. Even with spare production capacity, logistical bottlenecks could prevent the market from being supplied adequately, exacerbating price volatility.

China’s economic stimulus

On the demand side, China’s recent economic stimulus package is seen as a moderating factor but not a major driver of oil demand. Historically, China has been a key driver of global oil demand growth, but Goldman Sachs expects a more subdued effect this time. “China’s stimulus is likely to boost oil demand by only 200,000 barrels per day next year, which is two to three times slower than the pre-pandemic growth rate,” Struyven said. The slow recovery in China’s demand and green policy initiatives aimed at reducing reliance on oil limits the upside for oil demand from the world’s second-largest economy.

In contrast, the US remains the largest oil consumer, and the ongoing strength of the US economy—evidenced by robust payroll data and GDP growth—continues to support global demand. Struyven pointed out that US growth is exceeding expectations, with GDP growth running at 3%, providing a constructive outlook for oil demand in the near term. This is further supported by expectations of interest rate cuts by the Federal Reserve, which could weaken the dollar and increase demand for oil in non-US markets.

Price outlook and market scenarios

Goldman Sachs projects that Brent crude will remain in the $70 to $85 per barrel range in the near term, though short-term risks are skewed to the upside due to potential supply disruptions. Struyven explained that current oil inventories are below historical averages, suggesting that prices could rise slightly even without a major disruption. “The fundamentals at the level of inventories are consistent with a price that’s a few dollars higher than what we currently see, even after the geopolitical-driven rally,” he said.

Looking further ahead, the outlook for 2025 could see oil prices in the low $60s if spare capacity is reintroduced into the market more aggressively than expected. However, Struyven noted that such scenarios depend heavily on OPEC’s willingness and ability to bring barrels back to market. Additionally, potential trade disruptions and their impact on global GDP remain downside risks to oil demand.

Gold prices positioned for growth

Gold is also expected to rise as central banks continue to diversify their reserves away from the US dollar. Goldman Sachs forecasts a 10% rise in gold prices, reaching $2,900 per troy ounce by early 2025. Struyven highlighted that the freeze on Russian gold reserves in 2022 has triggered a shift in how central banks view gold as a reserve asset. “We think that the sharp tripling in central bank purchases of gold is not going away anytime soon,” he said.

Gold is also likely to benefit from the global monetary easing cycle. As interest rates fall, the opportunity cost of holding gold decreases, making it a more attractive investment. The Federal Reserve is expected to cut interest rates by 150 basis points over the next year, while China is also easing its monetary policy. “The cyclical boost from Fed cuts and global rate cuts for gold is very significant and not yet fully priced in,” Struyven added.