The year 2023 posed significant challenges for Sovereign Investors as the macroeconomic landscape made it increasingly difficult for them to thrive, according to the latest report from Global SWF. Despite controlled inflation and anticipated drops in interest rates, financial markets reflected geopolitical uncertainties, hinting at a potential economic crisis in the coming months.

The World Bank’s estimation of a meagre 2.1% global GDP growth in 2023, with a modest recovery to 2.4% in 2024, further underscored the challenges. Amid this backdrop, climate change and the rise of AI continued to exert considerable influence on global dynamics.

The recovery of financial markets and sustained high oil prices significantly boosted the industry’s Assets under Management (AuM). Sovereign Wealth Funds (SWFs) experienced a marked recovery, reaching a peak of $11.2 trillion, while Public Pension Funds (PPFs) increased their assets to $23.1 trillion. However, Central Banks (CBs) remained almost flat at $15.4 trillion. Global SWF anticipates a combined $50 trillion among these groups again, surpassing the 2021 peak, potentially in 2024.

Financial markets, despite volatility, saw a robust performance throughout 2023. Most global indices showed positive growth, barring China’s Hang Seng and SSE, which experienced declines for the second consecutive year due to economic uncertainties and growth deceleration in the country.

Cautious approach

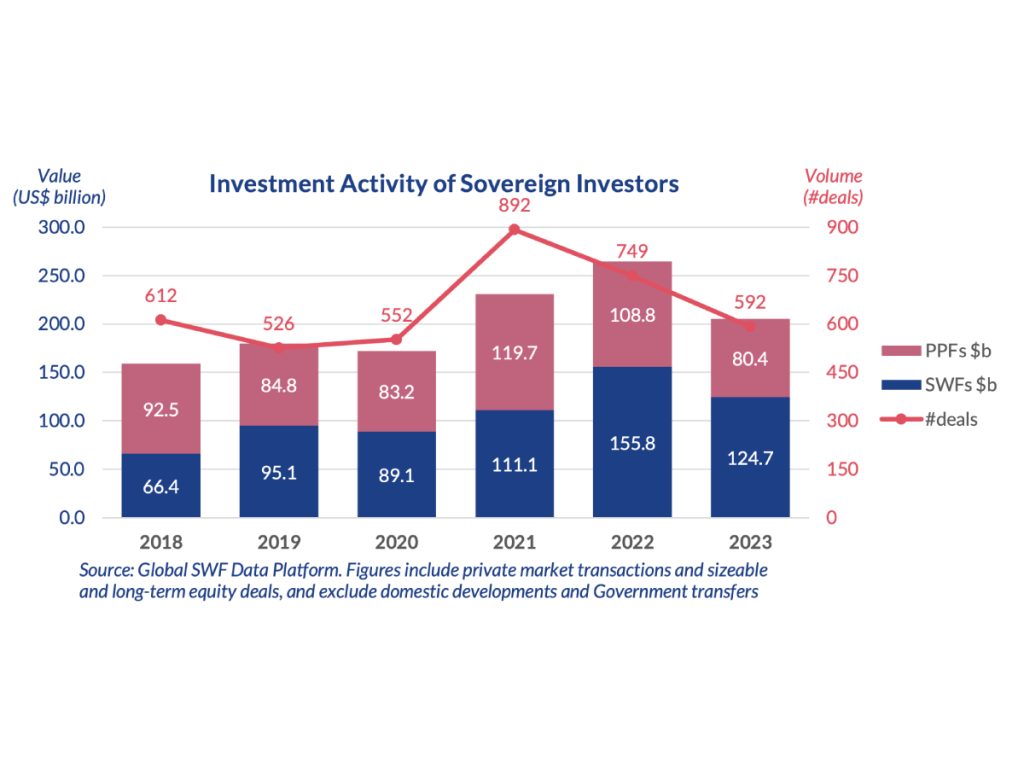

Sovereign investors demonstrated a cautious approach in 2023, investing less frequently than the previous year. While there was no shortage of capital among these institutions, SWFs decreased their investments by 20% to $124.7 billion across 324 transactions. Similarly, PPFs reduced their investments by 26% to $80.4 billion in 268 deals.

The Public Investment Fund (PIF) emerged as the lead investor, deploying $31.6 billion in 49 deals, signifying a 33% increase from 2022.

“In a short span of eight years since its reformulation, the Saudi institution has become a powerhouse both at home and overseas, to advance Vision 2030 and become the world’s largest SWF by 2030,” the report stated.

Notably, the Gulf region’s presence in global investments remained strong, with the five significant Gulf funds, including the Abu Dhabi SWFs (ADIA, Mubadala, ADQ), and Qatar’s QIA, among the top 10 most active dealmakers globally.

Preferences of top investors

Regional preferences of top investors witnessed a shift towards emerging markets. According to the report, half of the leaderboard increased their investments in emerging markets. India rose in popularity as a favoured destination, surpassing the UK and China and trailing only behind the US.

Regarding industries, real estate attracted over a quarter of investments, a proportion not seen since 2014. Financials and infrastructure remained popular, with industrial conglomerates experiencing increased investment due to Gulf investors’ domestic interests.

Co-investments exceeded $30 billion for the first time, with Gulf and Canadian funds actively participating. Furthermore, State-Owned Investors engaged in significant divestment activity, including IPOs that allowed Middle Eastern funds to monetise their domestically grown assets.

Most sovereign investors witnessed growth in their US Equities portfolios while maintaining interest in Indian stocks but diminishing interest in European and Chinese equities.

The report also highlighted significant developments in the industry, including establishing five new SWFs – Maharlika, HKIC, Pakistan, Kosovo and Mozambique – and progress towards ten potential new funds. Additionally, nine representative offices were opened overseas, predominantly in New York, London, and Singapore, with expectations of three more in Q1 2024. Notably, 32 CEOs and 21 top investment executives were appointed during the year, indicating a significant churn rate within the industry.

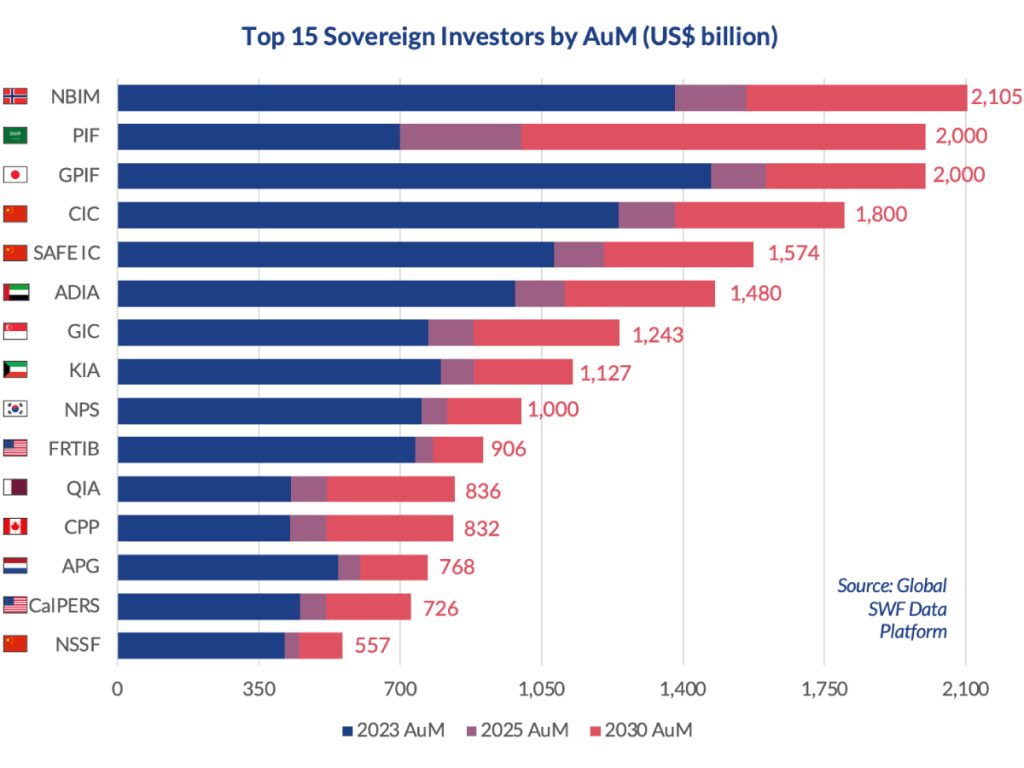

Global SWF revised projections suggesting a considerable increase in assets of State-Owned Investors, anticipating $54.9 trillion by 2025 and $71.0 trillion by 2030. The predictions hint at potential industry leaders, including Norway’s NBIM, Saudi’s PIF, and Japan’s GPIF, possibly reaching over $2 trillion in AuM by 2030.