The weaker US dollar in anticipation of swift Fed rate cuts leads many to believe that we have arrived at a ‘dollar smile’. However, this is not necessarily the case.

The USD is trending weaker, bringing the EUR/USD close to 1.12 and the US Dollar Index near 100. Despite the increasing anticipation for a September rate cut, the US economy is not significantly underperforming, suggesting that the USD is driven by interest rates rather than the smile, said David A. Meier, Economist at Julius Baer.

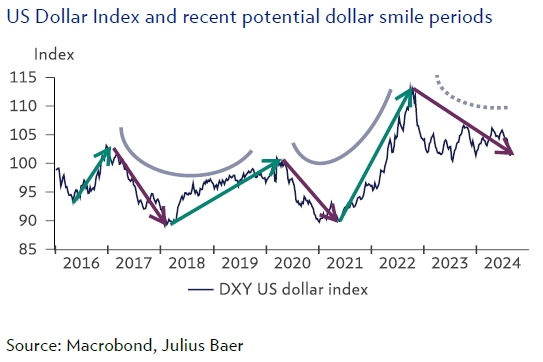

The “dollar smile” is an economic theory developed by economist Stephen Jen, which states that the US dollar tends to strengthen against other currencies in two scenarios: when the US economy is either extremely strong or when the globe is undergoing a recession. The period in between is the “smile”, in which the US economy weakens and underperforms the global economy or peer, but where global risk appetite also potentially stays robust, disfavouring the safe-haven USD.

Despite some analysts believing that the US economy is undergoing a “dollar smile”, ie. a period of decline despite global growth, Meier disagrees.

“Cyclical growth plays an important role in the theory, but growth differentials show that the US is currently not underperforming its peers significantly and is unlikely to do so in the future, according to our forecasts,” he noted. “Indeed, US rates are due to be cut soon, but we observe a waning of US growth superiority rather than an underperformance.”

As a result, the USD appears to be driven more by interest rates than by the smile.

“We continue to believe that a USD restrengthening is possible once some of the aggressive rate cut expectations are priced out again,” Meier said. “That said, we do not believe that the USD will regain its highs of late 2022, as there is plenty of resistance from overvaluation and lower rates.”

The bank further stressed that peer currencies may even remain stronger vs the USD, such as the GBP, the AUD, and the NZD, as rate cuts in those countries may not come as quickly as in the US. The GBP and NZD, in particular, could offer higher rates than the US towards the end of the year.