The Gulf Cooperation Council (GCC) economies are poised for stronger growth in 2025, driven by a combination of increased oil output, robust non-oil sector expansion and strategic diversification efforts. This optimistic outlook comes despite ongoing global economic headwinds, including geopolitical tensions and uncertainties in energy markets.

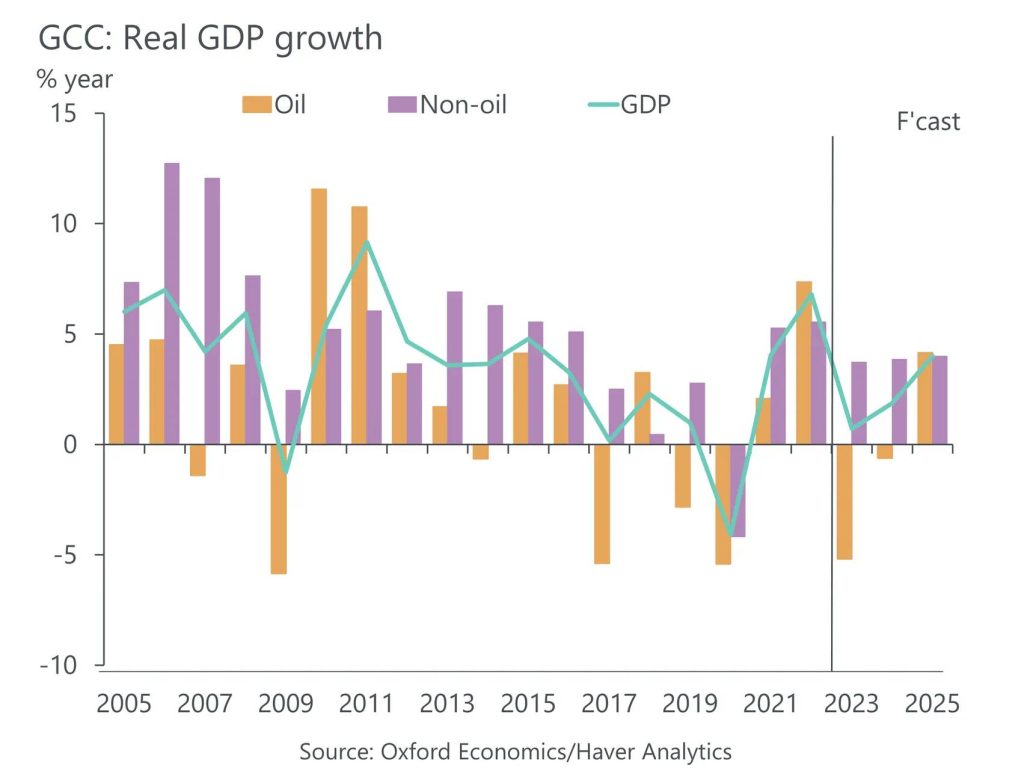

GCC economies are forecasted to grow by 4% in 2025, up from an estimated 1.9% in 2024. The surge will primarily be supported by the easing of OPEC+ oil production cuts and a steady performance in non-oil sectors. According to ICAEW’s Q4 2024 Economic Outlook Report, “growth in oil GDP will rise sharply to 4.2% next year as energy production ramps up after years of deep cuts.”

Non-oil sectors are expected to expand by 4.4%, reflecting the resilience of industries such as tourism, trade and finance. High-frequency indicators, such as purchasing managers’ indices (PMIs), remain firmly in expansionary territory, bolstered by increased domestic demand and foreign investment.

Oil sector

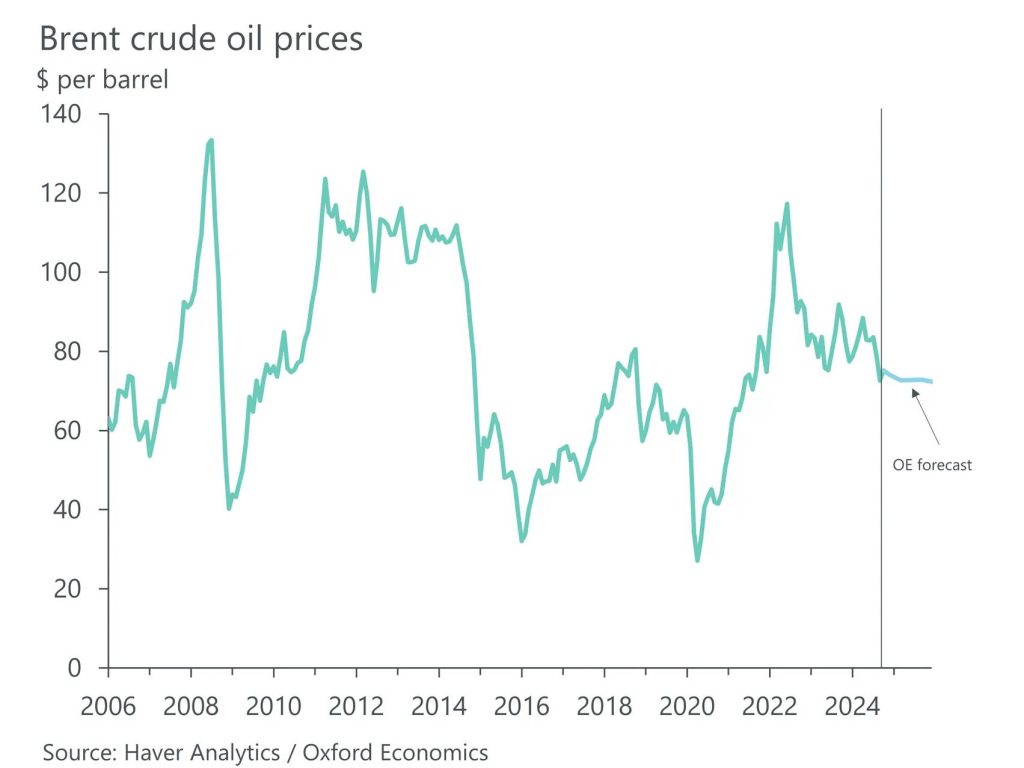

OPEC+ nations, including key GCC players, have agreed to extend production limits until early 2025. While this has capped oil revenue in the short term, it ensures price stability amid volatile demand. Brent crude prices are forecasted to average $72.6 per barrel in 2025, down from earlier projections of $77.5.

The gradual unwinding of these cuts is expected to fuel economic growth across the region. Saudi Arabia, for instance, anticipates a 3.4% rise in oil output next year. However, the report cautions that “any surge in oil prices above $75 is likely to be transitory given the soft global demand outlook.”

Country-specific insights

Saudi Arabia

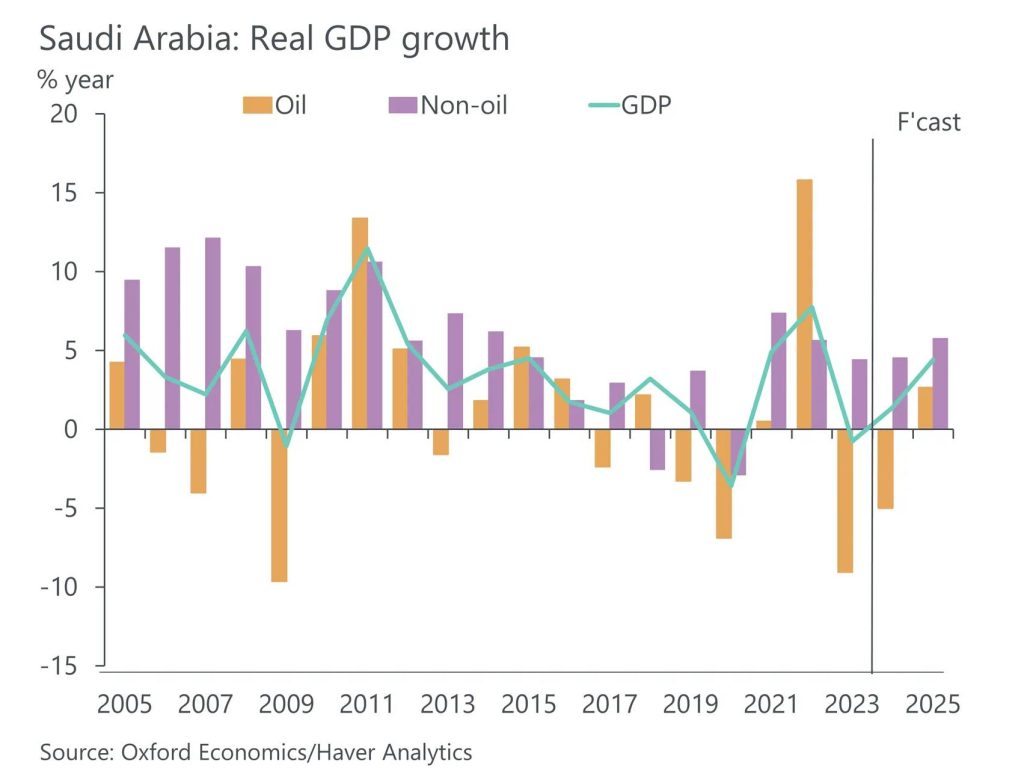

Saudi Arabia’s economy is projected to grow by 4.4% in 2025, following 1.4% growth in 2024. This will be driven by a rebound in oil production and robust investment in non-energy sectors such as tourism and construction. Diversification efforts under Vision 2030 remain central to the Kingdom’s strategy. The report highlights significant investments in flagship projects, including $800 billion allocated to the tourism sector over the next decade.

While fiscal deficits persist, Saudi Arabia’s low government debt ensures borrowing flexibility. The Public Investment Fund continues to play a strategic role, while initiatives like a 30-year tax incentive for global firms establishing regional headquarters aim to attract foreign direct investment (FDI).

United Arab Emirates

The UAE is set to achieve 4.5% GDP growth in 2025, supported by increased oil production and thriving sectors like tourism and real estate. In 2024, the non-oil economy grew by 4.5%, with tourism arrivals in Dubai up 6.3% year-over-year and record-breaking property transactions. The UAE’s Comprehensive Economic Partnership Agreements with countries like Australia and Vietnam are enhancing trade opportunities.

Renewable energy is another priority, with capacity surging by 70% last year. Ahead of COP29, the UAE unveiled ambitious climate goals, aiming for a 47% reduction in carbon emissions by 2035 compared to 2019 levels. These efforts align with the UAE’s broader strategy to lead the region in sustainability initiatives.

Fiscal and inflation trends

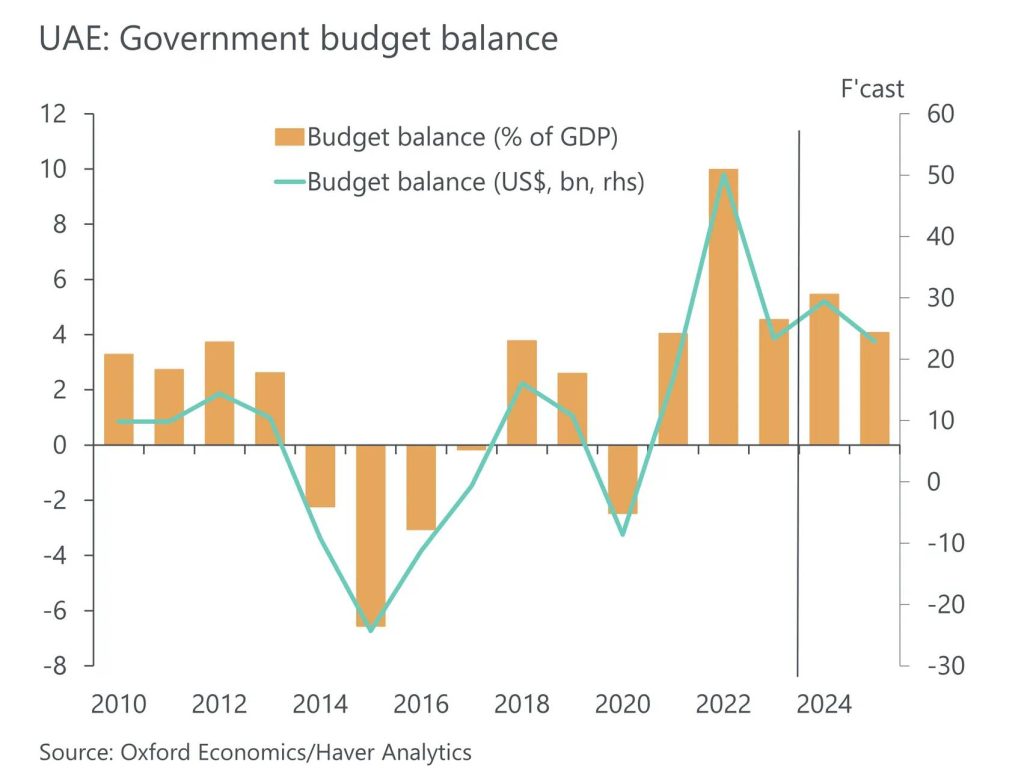

GCC countries face mixed fiscal dynamics. While Qatar and the UAE maintain budget surpluses, Saudi Arabia is expected to run deficits into the foreseeable future. Inflation across the region remains low, averaging 1.8% in 2024, but Saudi Arabia experienced a spike to 1.9%, driven primarily by housing rent increases in Riyadh.

Central banks across the GCC continue to follow the US Federal Reserve’s monetary policy. With interest rates easing, further reductions are expected in 2025, providing support to private-sector investment and real estate.

Geopolitical risks

The report highlights several external risks that could weigh on the GCC outlook. Geopolitical tensions, particularly in Iran, Lebanon and Iraq, remain significant challenges. For instance, Lebanon’s GDP growth forecast for 2025 has been cut to 0.8%, reflecting ongoing conflict and political instability. Iraq is also expected to see slower growth due to extended oil production cuts.

The broader global environment, including US-China trade tensions and potential tariff policies, adds another layer of uncertainty. While the GCC is unlikely to be directly targeted by US tariffs, the fragmentation of global trade could hinder diversification efforts.

Investment and diversification

The GCC continues to attract substantial foreign investment, with the UAE leading globally in FDI flows relative to its economy. Saudi Arabia also witnessed strong momentum in IPOs, raising $2.6 billion in the first nine months of 2024. The secondary offering of Aramco shares further emphasises the region’s ability to draw international capital.

However, challenges remain in achieving diversification targets. The report notes that Saudi Arabia has made limited progress toward its Vision 2030 goal of non-oil exports comprising 50% of non-oil GDP.

While the near-term outlook is positive, achieving long-term goals will require addressing both global uncertainties and internal structural hurdles.