Egypt’s non-oil private sector economy moved closer to stabilisation in May, as the headline S&P Global Egypt Purchasing Managers’ Index (PMI) rose to 49.5, up from 48.5 in April. The index remained below the 50.0 threshold that separates growth from contraction, signalling a third consecutive month of decline, but marked the slowest rate of deterioration in operating conditions since February.

The PMI, which aggregates data on output, new orders, employment, supplier delivery times and purchasing activity, remained above its long-run average of 48.2.

Output and new business volumes both declined in May but at a slower pace compared to the previous month. Surveyed firms cited weaker customer demand and lower order book volumes as key factors. The manufacturing sector reported signs of renewed growth, partially offsetting declines elsewhere.

Despite the slower contraction in activity, companies reduced their purchasing activity at the fastest rate since October 2023, aiming to streamline inventories. Input stocks rose only marginally during the month.

David Owen, Senior Economist at S&P Global Market Intelligence, said that while operating conditions continued to deteriorate, the slower rate of decline and renewed strength in manufacturing suggested some early signs of stabilisation. He added that rising input costs and exchange rate pressures were key risks affecting short-term business sentiment.

Employment fell for the fourth consecutive month, though job losses were modest. Most companies said they were not replacing staff who left voluntarily. Backlogs of work showed little change.

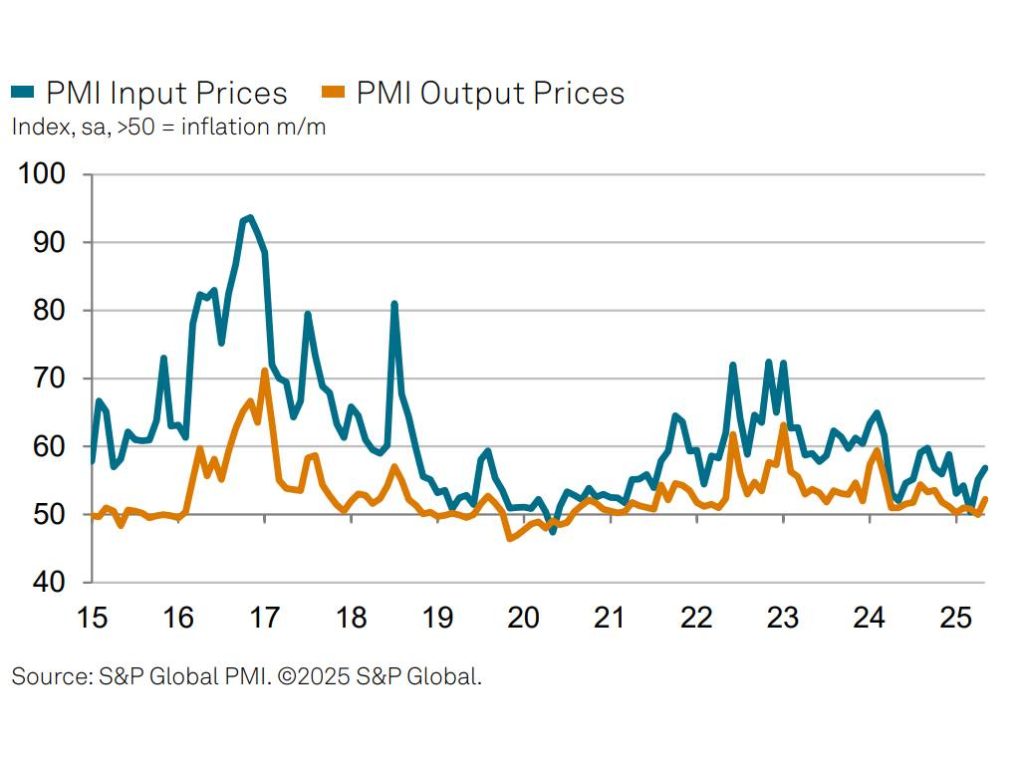

Input costs rose at the fastest rate so far in 2025, driven mainly by higher prices for fuel, cement, and paper. Firms cited currency volatility, particularly against the US dollar, as a major driver of increased supplier costs. Wage inflation remained subdued.

After remaining flat in April, selling prices increased in May at the fastest pace in seven months as firms passed part of the cost burden to customers.

Looking ahead, business confidence improved slightly but remained below historical averages. Firms noted that ongoing cost pressures and weak demand continued to limit optimism for future output growth.