The UAE’s banking sector recorded a robust start to 2025, with net income across the country’s 10 largest listed banks rising 8.4% quarter-on-quarter to Dh22.2 billion, according to Alvarez & Marsal’s Q1 UAE Banking Pulse. The earnings momentum was supported by a sharp decline in impairment charges and a surge in non-interest income despite a decline in net interest income due to narrowing margins.

Fee and commission income rose 18% QoQ, offsetting a 2.1% drop in net interest income caused by softer yields on credit. The net interest margin (NIM) fell 15bps to 2.52%, with the yield on credit down nearly 100bps to 10.9%. This trend reflects the broader regional environment, where banks are adjusting to monetary easing cycles following two years of rate hikes.

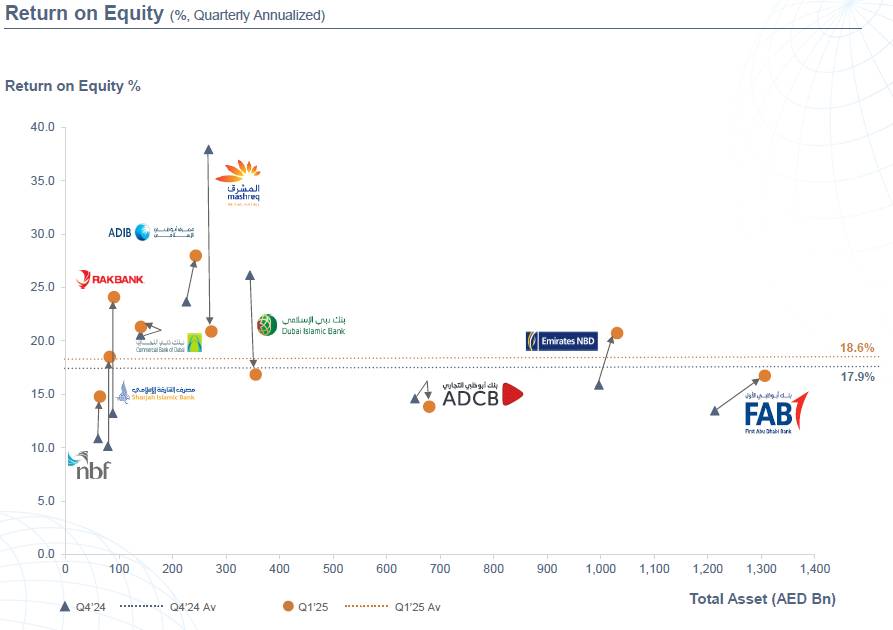

Despite topline pressures, profitability ratios improved. Return on equity (RoE) reached 18.6%, up from 17.9% in Q4 2024, while return on assets (RoA) edged up to 2.1%. This resilience is underpinned by cost discipline, as operating expenses fell 7.8% quarter-over-quarter, helping to push the cost-to-income (C/I) ratio down to 28.2%, the lowest in four quarters.

Lending rebounds, liquidity improves

Loan growth gained pace, rising 3.6% QoQ, led by a 5.1% increase in corporate and wholesale lending. This rebound contrasts with slower lending trends observed in other GCC markets during the same period, highlighting continued business activity in the UAE, particularly in sectors such as energy, infrastructure, and services.

On the funding side, deposits rose by 5.8% QoQ, driven by a 7.6% increase in current and savings account (CASA) balances. The loan-to-deposit ratio (LDR) decreased to 74.7%, improving system liquidity and providing banks with greater flexibility to manage funding costs as interest rates decline.

The improved deposit mix helped reduce the cost of funds by 52bps to 3.9%. With further rate cuts expected in H2 2025 across global markets, UAE banks are increasingly focused on defending margins through repricing strategies and balance sheet optimisation.

Asset quality strengthens further

The sector’s risk metrics also improved. The cost of risk (CoR) declined 45bps to 0.29%, while the coverage ratio rose to 110.5%, supported by higher recoveries and portfolio clean-ups. Stage 1 loans increased 3.9%, while exposures in Stage 2 and Stage 3 declined, reflecting a shift toward higher-quality lending.

The non-performing loan (NPL) ratio fell to 3.2%, among the lowest in the region, driven by proactive credit management and a healthier macroeconomic backdrop. The UAE’s GDP growth is projected at 3.9% in 2025, according to IMF forecasts, supported by non-oil sector expansion and increased public investment ahead of major events, such as COP29 and the Abu Dhabi World Expo 2030.

Consolidation returns to the fore

The first quarter also marked a return to strategic mergers and acquisitions (M&A) in the sector. Emirates NBD announced plans to fully acquire Emirates Islamic Bank, a move seen as consolidating its position in Islamic finance while preparing for regional expansion. The deal comes amid rising investor interest in cross-border banking scale, particularly in light of regulatory pressures to boost capital buffers and operational efficiencies.

Banks are also investing in digital transformation, cost automation, and embedded finance solutions. Several institutions, including Mashreq and ADCB, have launched new fintech partnerships and AI-driven tools to enhance client engagement and reduce overhead.

According to Sam Gidoomal, Managing Director and Head of Middle East Financial Services at A&M, the Q1 data reflect a shift in focus from topline growth to operational resilience. “This quarter underscores the banks’ ability to defend profitability and quality despite lower interest spreads and evolving regulatory dynamics,” he said.

Margin management and selective growth

Looking ahead, the key challenge for UAE banks will be maintaining profitability in a falling-rate environment. With the US Federal Reserve expected to begin a rate-cutting cycle in the second half of 2025, regional rates may follow suit, further pressuring interest income.

At the same time, structural tailwinds remain. The UAE’s position as a trade, tourism, and financial hub continues to attract capital and support loan demand. S&P Global recently reaffirmed stable outlooks for the country’s top-tier banks, citing strong capitalisation and funding bases.

Banks will likely remain selective in asset growth, focusing on high-yield segments such as SME lending, structured trade finance, and digital consumer banking, while managing risk through conservative provisioning and cost control.

UAE banks have entered 2025 with solid earnings, cleaner balance sheets, and improved efficiency. While margin compression poses ongoing risks, the sector appears well-positioned to navigate a changing rate environment through diversification, digitisation, and disciplined growth. As the cycle turns, maintaining this momentum will depend on how well banks balance yield protection with strategic investment and capital management.