The International Monetary Fund has raised its 2025 growth forecast for the Middle East and Central Asia to 3.4%, up from 2.4% in 2024, driven by stronger output in Saudi Arabia and improved financial conditions. Growth in Saudi Arabia is now expected to reach 3.6% in 2025 and 3.9% in 2026, a 0.6 percentage point upgrade from April’s projection, supported by fiscal spending and stabilising oil output.

Across the wider region, a combination of front-loaded trade activity and relatively contained energy prices has helped sustain momentum despite ongoing uncertainty around tariffs and monetary policy. The IMF said regional economies have adjusted to a more volatile global environment by tapping fiscal buffers and attracting capital inflows as global financial conditions eased in recent months.

Oil prices, which had spiked following military tensions between Iran and Israel in June, have since moderated as the supply outlook stabilised. Energy prices are now expected to fall by 7% in 2025, though the IMF cautioned that any renewed disruption in the Middle East could reverse that trend.

The IMF kept its 2026 forecast for the Middle East and Central Asia steady at 3.5%, citing strong infrastructure investment, fiscal stimulus in some Gulf states, and ongoing reforms aimed at diversifying non-oil sectors.

Global outlook: Growth holds, but tariff and fiscal risks persist

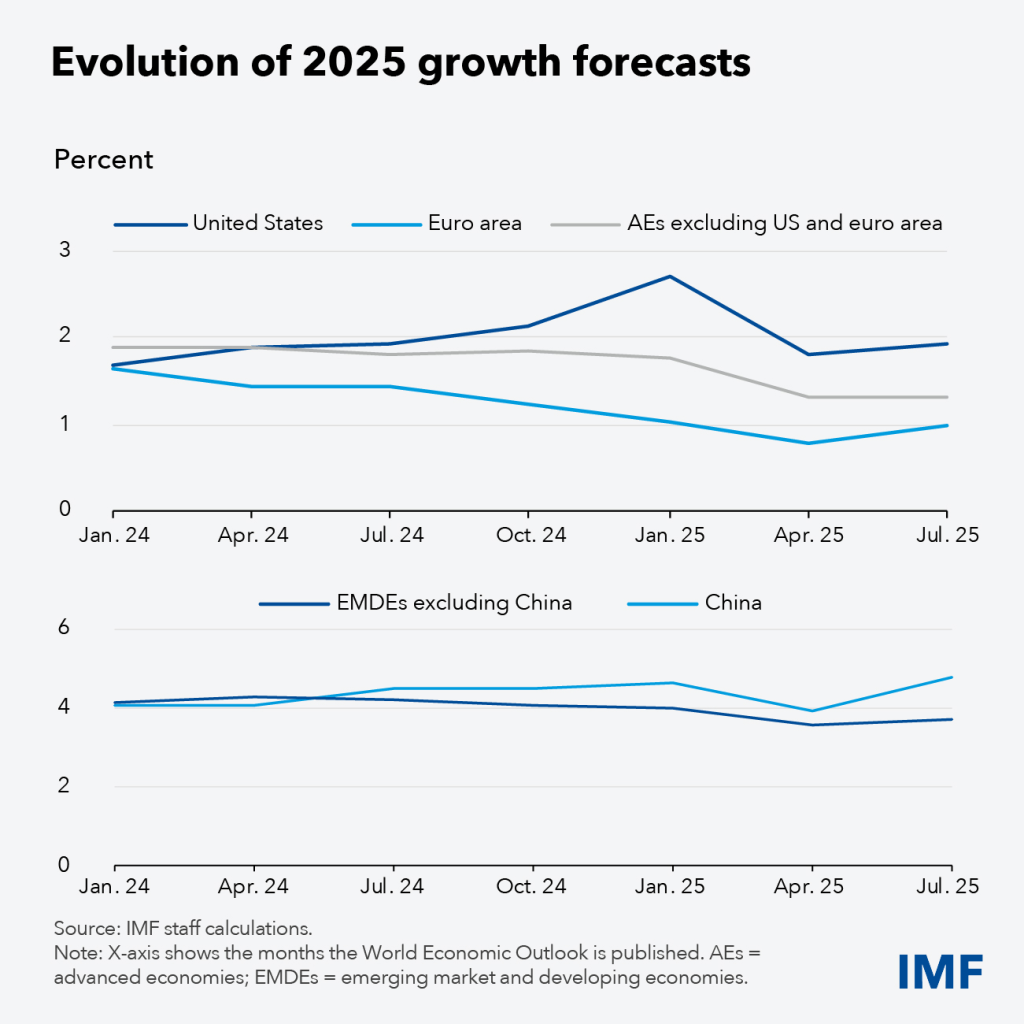

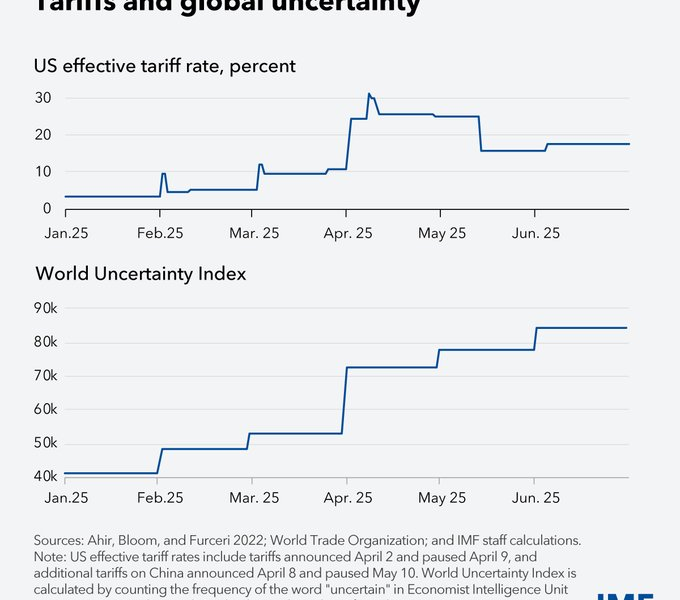

Globally, the IMF projects output growth of 3.0% in 2025 and 3.1% in 2026, slightly higher than its April forecasts. The upward revision is linked to better-than-expected financial conditions, a weaker US dollar, and lower-than-feared average US tariff rates following a temporary easing of trade tensions. The US and China reached a 90-day tariff pause in May, which is set to expire in August.

However, the IMF warns that this resilience may prove short-lived. The US economy contracted by 0.5% on an annualised basis in Q1 2025, while growth in global trade appears to have been artificially inflated by businesses front-loading imports ahead of anticipated tariff increases.

If tariffs return to their April levels, or rise further, as suggested by recent US policy communications, global growth could fall by 0.2 percentage points, the IMF said. The current US effective tariff rate stands at 17.3%, down from the 24.4% peak assumed in April. Rates on the rest of the world average 3.5%.

Inflation globally is projected to decline to 4.2% in 2025 and 3.6% in 2026, broadly in line with previous projections. However, the IMF noted diverging inflation trends: in the US, inflation is expected to remain above target, partly due to the pass-through of tariffs, while inflation in Europe and Asia is expected to be more contained.

In advanced economies, 2025 growth is forecast at 1.5%, rising to 1.6% in 2026. In the US, growth is expected to slow to 1.9% in 2025 before rising to 2.0% the following year, supported by the fiscal stimulus embedded in the One Big Beautiful Bill Act. Euro area growth is forecast to accelerate slightly to 1.0% in 2025, led by investment and exports.

In emerging markets and developing economies, output is expected to grow by 4.1% in 2025 and 4.0% in 2026. China’s forecast has been revised up sharply to 4.8% for 2025 due to stronger-than-expected Q1 performance and a significant reduction in tariffs on exports to the US. India is projected to expand 6.4% in both 2025 and 2026.

Trade, currency, and risk landscape

World trade volume is expected to grow 2.6% in 2025, revised up by 0.9 percentage points, but is forecast to slow to 1.9% in 2026. The IMF attributes this shift to fading front-loaded trade activity and continued uncertainty around the global trade regime.

The US dollar has weakened since April, allowing some monetary easing in emerging markets. Still, the IMF warned that sustained fiscal deficits in major economies, particularly the US, could lead to steeper yield curves and tighter global financial conditions. Sovereign debt pressures in France, Brazil, and the US remain a concern.

Geopolitical risks are also a key factor in the IMF’s downside scenario. The Fund cited potential supply disruptions stemming from renewed tensions in the Middle East or Ukraine, which could raise commodity prices and complicate central bank policy paths.

The IMF maintains that clearer trade frameworks, coordinated fiscal policy, and structural reforms are essential to stabilise expectations and lift medium-term growth. Without this, the current resilience may give way to volatility, especially if tariff escalations or fiscal sustainability concerns resurface.