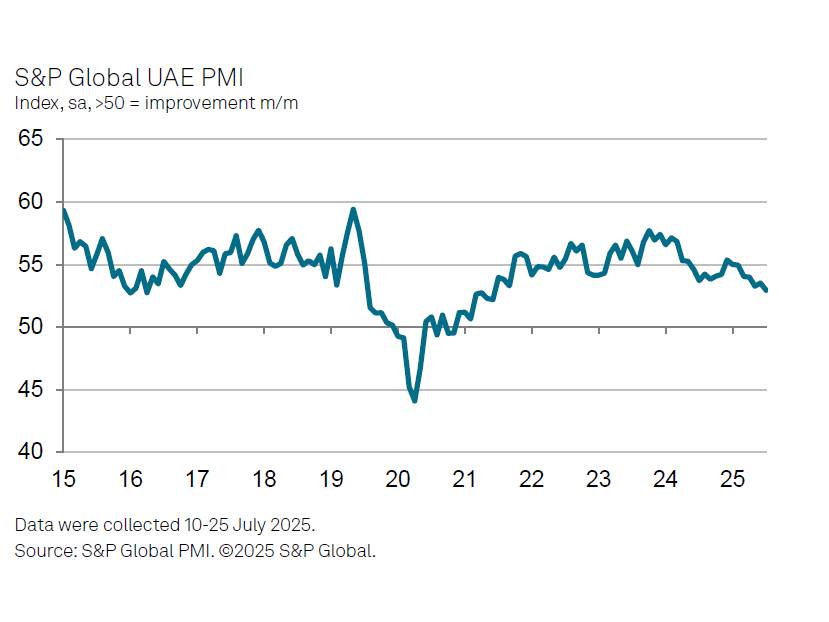

Non-oil business activity in the UAE expanded at its weakest pace in over four years in July, as regional geopolitical tensions and slowing demand curbed new orders, according to S&P Global’s monthly survey.

The UAE Purchasing Managers’ Index (PMI) fell to 52.9 in July from 53.5 in June, marking the lowest level since June 2021. While the index remained above the 50.0 threshold separating growth from contraction, the pace of expansion was softer than the long-run trend.

S&P Global said the pullback was driven by reduced momentum in new business volumes, with some companies citing client hesitancy linked to regional tensions and weaker tourism. The increase in new orders was the slowest since August 2021.

Employment growth also eased, with job creation at its weakest since March. Meanwhile, outstanding business rose for the first time since January, suggesting firms were struggling to keep up with workloads. Input purchasing growth slowed in line with weaker sales, and inventories declined for the third time in five months.

Average input costs rose at their fastest rate since April, reflecting higher prices for shipping, materials, wages and capital. Firms passed on some of the increase through higher output charges, reversing a brief decline seen in June.

Despite the softer reading, overall output continued to rise as firms worked through order backlogs. Some survey respondents pointed to improved client sales and technology investments as drivers of higher output.

Expectations for future activity remained positive, although sentiment dipped slightly on concerns about global uncertainty and intensifying competition.

David Owen, Senior Economist at S&P Global Market Intelligence, said: “Business conditions improved in July, but the rate of growth was the weakest since the middle of 2021. The latest data indicated the softest rise in incoming new work in almost four years.”

He added that some firms attributed the slowdown to geopolitical uncertainty, particularly regional tensions involving Iran and Israel, while others cited increased market competition.

Owen said a potential easing in regional tensions could support a rebound in demand, but warned that risks remain due to limited inventory growth, hiring constraints, and subdued business confidence.

Dubai PMI rises

In contrast to the wider UAE trend, Dubai’s non-oil private sector showed stronger momentum in July. The Dubai PMI rose to 53.5 from 51.8 in June, supported by a sharper rise in new orders. Output growth reached a five-month high, and firms continued hiring and building inventories.

Supplier performance improved, though some firms cited minor shipping disruptions. Input costs rose at the fastest pace since April, but selling price inflation slowed to its lowest in eight months.