Gold rose 26% in the first half of 2025, outperforming all major asset classes and setting 26 all-time highs, driven by falling demand for US Treasuries, a weaker dollar, and persistent geopolitical tensions. Investors are now weighing whether the metal can maintain its momentum or if the second half of the year will bring a correction.

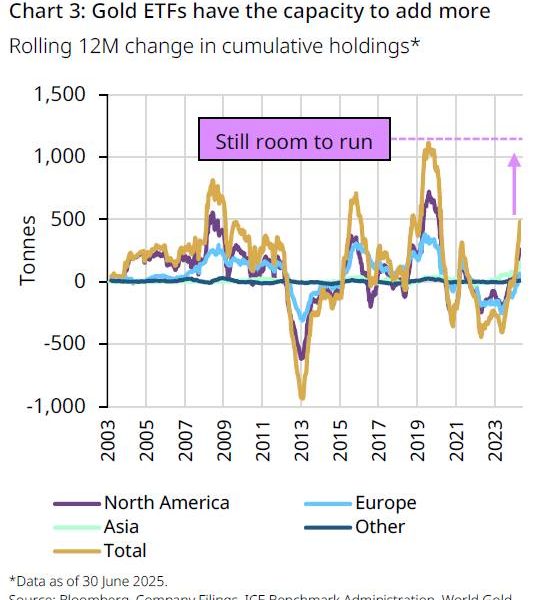

According to the World Gold Council’s mid-year outlook, gold’s H1 gains were underpinned by investor demand across exchange-traded funds (ETFs), over-the-counter markets and futures, with average daily trading volumes reaching $329 billion, the highest semi-annual level on record. Holdings in gold-backed ETFs grew by 397 tonnes in six months, lifting total assets under management to $383 billion, the highest since August 2022.

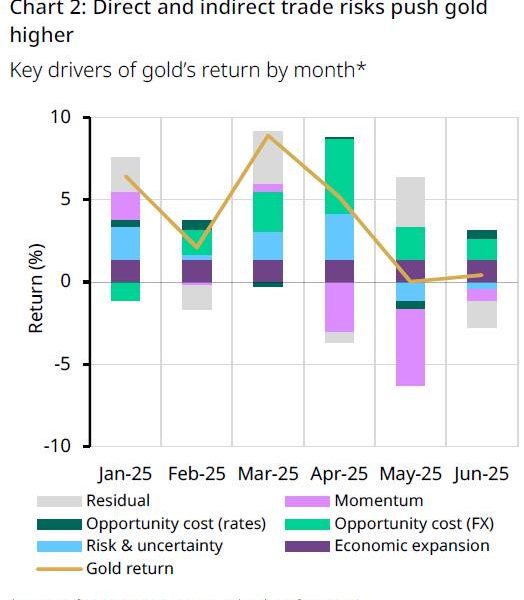

The US dollar experienced its weakest start to the year since 1973, while gold posted a strong performance across various currencies. Prices rose 41.9% in Turkish lira, 26% in Indian rupees and US dollars, and 23.8% in Chinese renminbi. According to the Council’s Gold Return Attribution Model, about 16% of gold’s H1 return was explained by macro drivers: 7% from opportunity cost (mainly dollar weakness), 4% from risk and uncertainty, and 5% from momentum linked to ETF flows.

What H2 2025 may look like

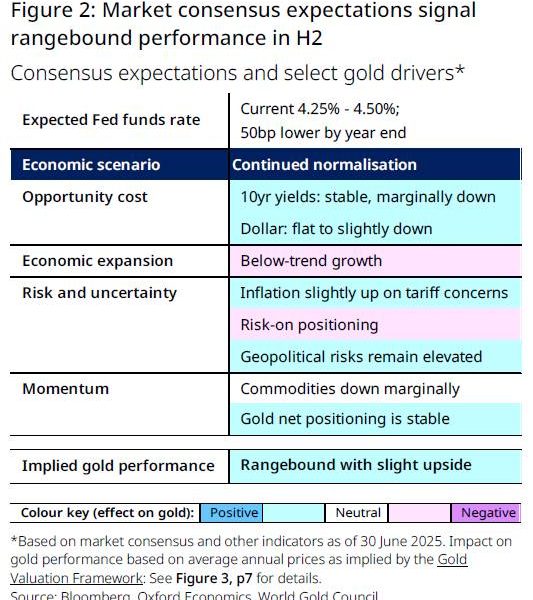

The baseline market consensus indicates below-trend growth, continued geopolitical tensions, and central bank rate cuts in the final quarter of the year. The World Gold Council expects gold to remain rangebound, with a potential upside of 0% to 5% in the second half of 2025, adding to its already strong annual performance.

However, gold’s trajectory remains dependent on broader macro conditions. In a downside scenario where conflict resolution leads to renewed risk appetite and rising Treasury yields, gold could retreat by 12% to 17%, giving back much of its H1 premium. This would likely trigger ETF outflows and dampen speculative demand.

On the other hand, if the global economy deteriorates further, driven by stagflation, a decline in consumer confidence, or renewed trade tensions, gold could climb another 10% to 15% in H2. Central bank diversification away from the dollar could also reinforce demand. The Council’s central bank survey shows that 73% of respondents expect a lower share of USD reserves over the next five years, with a greater allocation to gold.

ETF and futures positioning suggest there is further capacity for investment growth. ETF holdings, currently at 3,616 tonnes, are still below the 2020 peak of 3,925 tonnes. Net long positions in COMEX futures sit near 600 tonnes—well below the 1,200 tonne peaks seen during past crises, leaving room for additional investor inflows if risk intensifies.

Key support and resistance levels

Technical analysis indicates $3,000/oz as a likely support level, with opportunistic buying anticipated if gold retreats to this range. On the upside, gold has already broken past several resistance levels. The record high of $3,434/oz was set on June 13, 2025.

While the current environment continues to support gold’s safe-haven appeal, the outlook remains uncertain. Consensus expects a modest continuation of gains in the second half of the year. However, deviations from the baseline, either toward deeper economic weakness or a clearer resolution of global trade tensions, will determine how much higher or lower gold moves before the year ends.