The global economy is on a trajectory toward a soft landing, marked by a gradual inflation and sustained growth decline, but risks persist, according to the latest report from the International Monetary Fund (IMF).

In the second half of last year, global activity showcased resilience, supported by factors influencing demand and supply in significant economies. On the demand side, robust private and government spending sustained activity despite tight monetary conditions. Meanwhile, the supply side saw increased labour force participation, repaired supply chains, and lower energy and commodity prices, countering renewed geopolitical uncertainties.

This resilience will carry over, the Washington-based fund said.

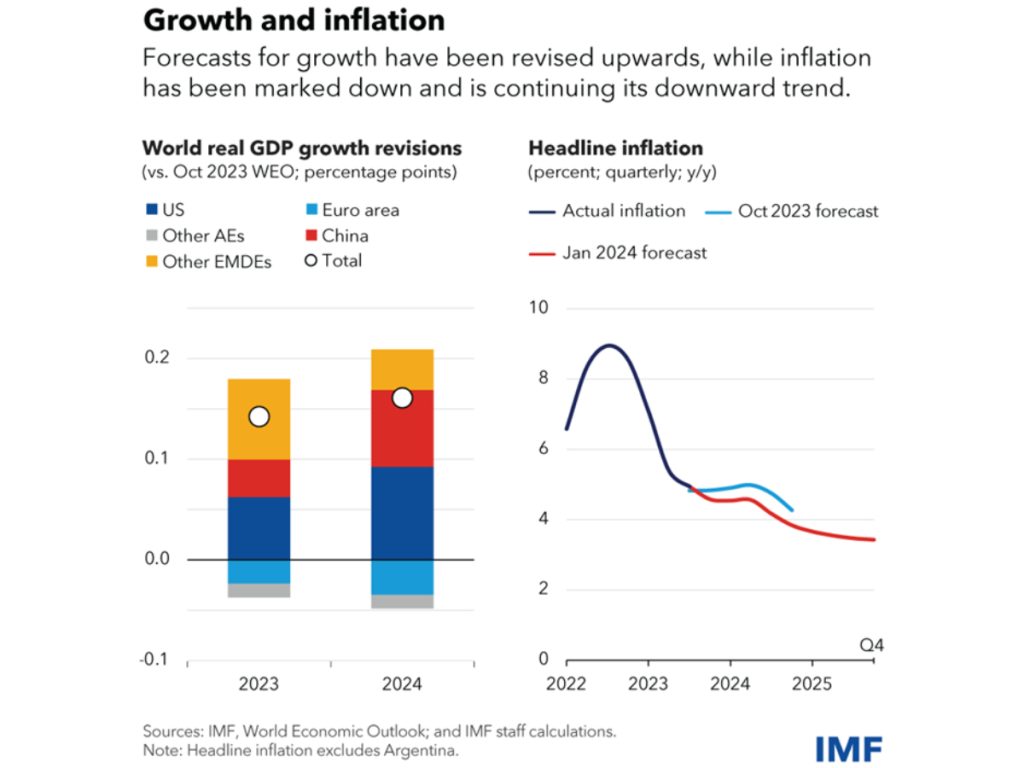

The IMF’s World Economic Outlook report, released on Tuesday, projects a steady global growth of 3.1% in 2024, indicating a 0.2 percentage point increase from October projections. The growth is expected to increase to 3.2% in the following year. However, the report notes significant divergences, anticipating slower growth in the US and China due to the ongoing effects of tight monetary policy and weaker consumption and investment, respectively. In contrast, the euro area is expected to experience a rebound in activity after a challenging 2023.

“Many other economies continue to show great resilience, with growth accelerating in Brazil, India, and Southeast Asia’s major economies,” said Pierre-Olivier Gourinchas, director of research at the fund

Inflation eases

Inflation is showing signs of easing, with global headline inflation expected to decline to 4.9% in 2024 (excluding Argentina), down by 0.4 percentage points from October projections. Core inflation, excluding volatile food and energy prices, is also downward. For advanced economies, headline and core inflation are projected to average around 2.6% in 2024, aligning closely with central banks’ inflation targets.

While the outlook has improved, the IMF highlights balanced risks. On the upside, disinflation could occur faster than anticipated, fiscal consolidation measures may face delays due to global elections, and advancements in Artificial Intelligence could spur investment and productivity growth. On the downside, geopolitical tensions could lead to new commodity and supply disruptions, core inflation might prove more persistent, and markets could be overly optimistic about early rate cuts.

“Markets appear excessively optimistic about the prospects for early rate cuts,” said Gourinchas. “Should investors re-assess their view, long-term interest rates would increase, putting renewed pressure on governments to implement more rapid fiscal consolidation that could weigh on economic growth.”

Policy challenges

Policy challenges ahead involve taking stock and looking ahead, particularly in light of recent disinflation driven by declining commodity and energy prices. The report emphasises the role of monetary policy, which worked through channels such as convincing businesses and individuals that high inflation would not persist.

However, uncertainties remain, and central banks face the challenge of avoiding premature easing that could lead to a rebound in inflation. Signs of strain are evident in interest rate-sensitive sectors, and a pivot toward monetary normalisation is crucial.

“My sense is that the United States, where inflation appears more demand-driven, needs to focus on risks in the first category, while the euro area, where the surge in energy prices has played a disproportionate role, needs to manage more the second risk. In both cases, staying on the path toward a soft landing may not be easy,” said Gourinchas.

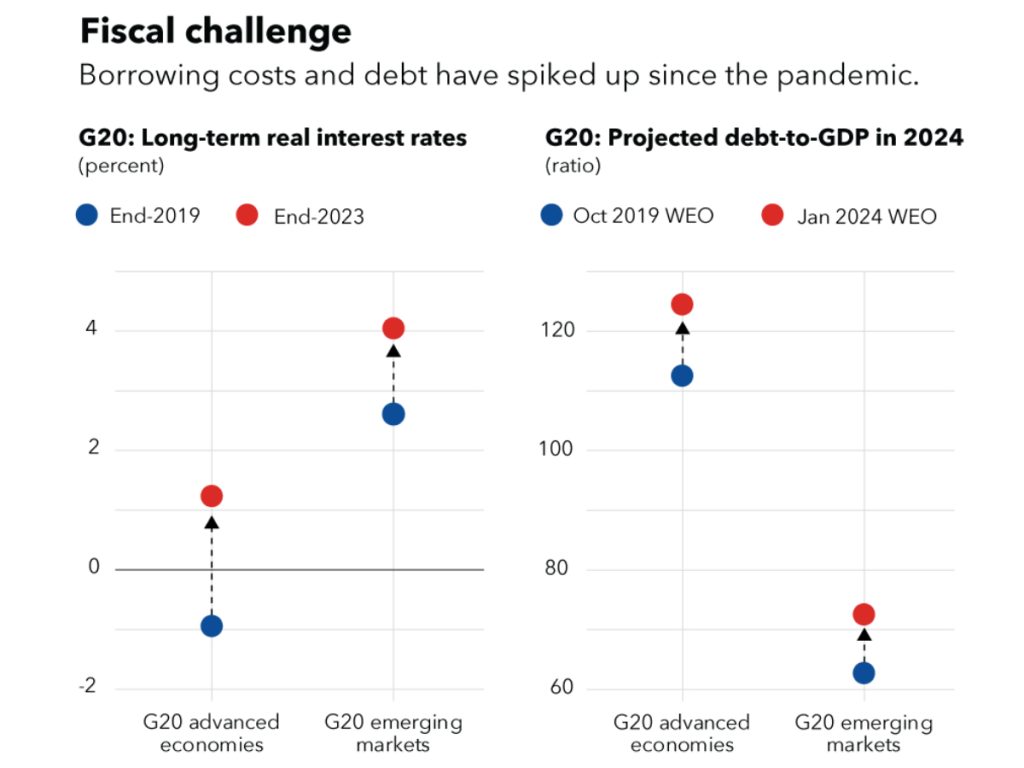

“The biggest challenge ahead of us is to tackle elevated fiscal risks,” he added. “Most countries came out of the pandemic and energy crisis with higher public debt levels and borrowing costs. Bringing down public debt and deficits will give space to deal with future shocks.”

The IMF underscores the need to address elevated fiscal risks, emphasising the importance of reducing public debt and deficits. Fiscal measures introduced to counter high energy prices should be phased out, and a steady fiscal consolidation, along with an improved and well-enforced fiscal framework, is recommended.

The report acknowledges emerging markets’ resilience but warns of potential capital outflows and currency volatility due to policy divergence. Strengthening buffers aligning with the Integrated Policy Framework is advised.

Looking beyond fiscal consolidation, the focus should return to medium-term growth. The IMF projects global growth of 3.2% in the next year, emphasising the need for a faster pace to address structural challenges like climate transition, sustainable development, and improved living standards. Reforms in governance, business regulation, and external sector policies are recommended to unleash latent productivity gains.