The year 2024 has opened with cautious optimism for the oil and gas industry. Financially, the rises in global production and easing inflation rates are predicted to offset concerns surrounding supply chains and political tensions. But what do the numbers look like?

The determining factor in the year ahead will be the prolonged production cuts announced by OPEC+. The group agreed in November to enforce voluntary output cuts of 2.2 million barrels per day (bpd). Saudi Arabia, the UAE, Iraq, Kuwait, Algeria and Oman also announced additional cuts for 2024, to prevent an oversupply in the face of record oil production by the US. So far, they seem successful.

Forecasting oil demand

When it comes to forecasting global oil demand, OPEC+ and the International Energy (IEA), have provided diverging outlooks. OPEC’s January report said it will grow by a “healthy” 2.2 million bpd in 2024, with a Middle East growth rate of 0.38 million bpd. In contrast, the IEA expects growth in global liquid fuels consumption to reach 1.24 million bpd, in 2024 – up 180,000 bpd from its previous projection. The IEA has also predicted the share of the Middle East in global oil production will increase steadily, resulting in higher export earnings by mid-century.

To keep up with the growing demand, the region’s oil and gas spending is set to hit $214 billion, Vijay Valecha, Chief Investment Officer at Century Financial, tells Finance Middle East. Aramco alone forecasts its capital expenditure for 2023 to reach between $45 and $55 billion. In this context, he said, “the financial performance of the oil and gas industry in the Middle East can be expected to improve”.

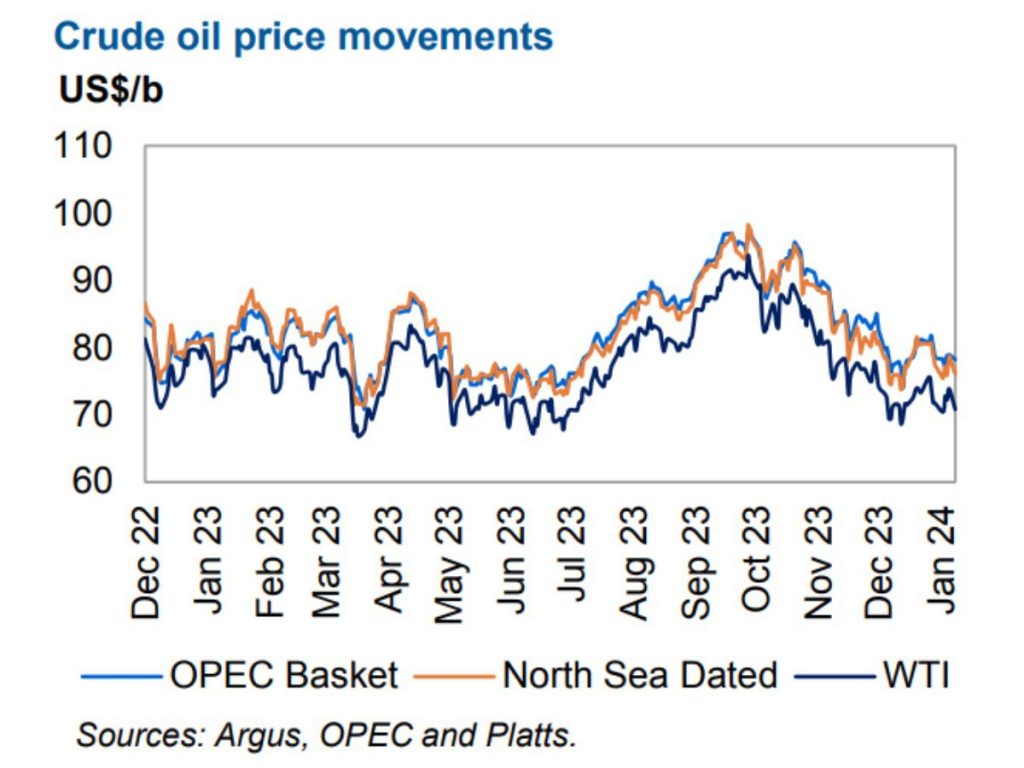

Will prices increase?

Financial predictions can resemble the Wild West, and the energy sector is no exception. The escalation of geopolitical tensions has brought forth fear of rising oil prices. Nonetheless, the market seems to have avoided the worst, with supply and demand pressures balancing each other out.

In 2023, the average annual price of Brent crude oil stood at $82.49 per barrel, $20 lower than the 2022 average. For 2024, the US Energy Information Administration (eia) estimated an $82 per barrel average Brent crude oil price and Saxo Bank placed it at $80 over Q1. The IEA predicted an $83 average and Citigroup set its forecast at $75 per barrel. Overall, the consensus remains within the $70 to $100 range, consistently above the $64 average of 2019.

Ole Hansen, Head of Commodities Strategy at Saxo Bank said this is because no single trigger has been “strong enough to change the dynamics of a market that has divided its focus between growth worries, not least in China and the US, as well as rising non-OPEC+ production on one hand and OPEC+ cuts and geopolitical risks on the other”.

Albeit, analysts are watching the region carefully. Daniel Takieddine, CEO MENA at BDSwiss, said the industry “could come under pressure if energy prices continue to slide in 2024”, and warned that an additional round of losses “could squeeze energy companies’ profits during the coming quarters.”

Mergers and acquisitions

Another unknown is whether we will see a continuation of the buying spree that characterised 2023. Last year, US industry acquisitions amounted to $250 billion, with some standouts being Exxon’s $4.9 billion acquisition of Denbury, Chevron’s purchase PDC Energy for $6.2 billion, and Occidental’s $12 billion offer for CrownRock. A Federal Reserve Bank of Dallas survey indicated over 75% of energy executives expect deals worth over $50 billion to arise in the next two years.

The Middle East region has not shared this tendency towards consolidation. This is due to the consistent production rates of its oil fields, as well as the fact that state-owned companies do not rely as heavily on rig count as an industry activity indicator. The MENA region recorded 29 deals in Q3 of 2023, worth $3.2 billion, according to GlobalData. The $400m acquisition of Fairfield Chemical Carriers was the largest disclosed deal of the quarter, while ADNOC’s 50% acquisition of Egypt’s TotalEnergies was the outstanding transaction of the first half of 2023.

The future of oil

Is oil on its way out? In the words of Dr Sreejith Balasubramanian, Associate Professor at Middlesex University, the industry is “navigating a complex mix of geopolitical risks, supply-demand shifts, and economic changes”. The IEA believes this will result in the industry reaching peak demand – 102 million bpd – before the end of the decade, before entering a period of gradual decline driven by the transition towards renewable energies. In this scenario, the Middle East would witness a reduction of over $80 billion in energy export revenues by 2030 and over $300 billion by 2050.

OPEC disagrees. The organisation’s World Oil Outlook 2023 sees global oil demand at 116 million bpd in 2045 and stresses the impossibility of oil and gas being completely removed from the global energy mix within seven years. This would mean increasing electricity generation globally from the current 29% to over 60% in 2030, something Valecha described as a “substantial gap.” Haitham Al Ghais, OPEC’s Secretary General added in a statement that “peak oil demand is not showing up in any reliable and robust short- and medium-term forecasts”.

On the way to net zero

Middle East countries, and oil-producing nations in particular, are expected to see economic growth in the years ahead. The World Bank has forecasted a 3.5% rise in MENA countries for 2024 and 2025, and 598 oil and gas projects are planned to commence operations in the region before 2026.

Nonetheless, the push towards net zero remains. Bahrain, Kuwait, Oman, Saudi Arabia, and the UAE have all set net-zero targets, and oil companies are following suit. Last December, about 30 national oil companies pledged to reach net zero by 2050 as part of the COP28 commitment to transition the global economy away from fossil fuels. To achieve this goal, ADNOC pledged to invest $23 billion in decarbonisation initiatives, while Aramco created one of the largest sustainability-focused venture capital funds, worth $1.5 billion.

The oil sector is undergoing a transformation, but one that can reap great rewards. In the view of Dr Jelena Janjusevic, Associate Professor at Heriot-Watt University Dubai, “the industry’s future beyond 2024 will depend on its ability to adapt to rapidly changing global conditions.”