The global economy is entering a prolonged period of weak growth, with the World Bank’s June 2025 outlook projecting global GDP to rise by just 2.3% this year, marking the slowest pace since 2008, excluding full-blown recessions. The downturn is broad-based and reflects the rising cost of geopolitical fragmentation, trade protectionism, and policy inertia, especially in the world’s emerging markets and developing economies (EMDEs).

The World Bank report spotlights a troubling reversal in the post-globalisation trajectory of convergence between rich and poorer nations. EMDEs, once seen as growth engines, are struggling to reduce poverty, generate jobs, or narrow income gaps. By 2027, high-income economies are expected to return to their pre-pandemic trend in per capita GDP. EMDEs will remain 6% below that threshold, a shortfall that could take two decades to recoup in many fragile or conflict-affected economies.

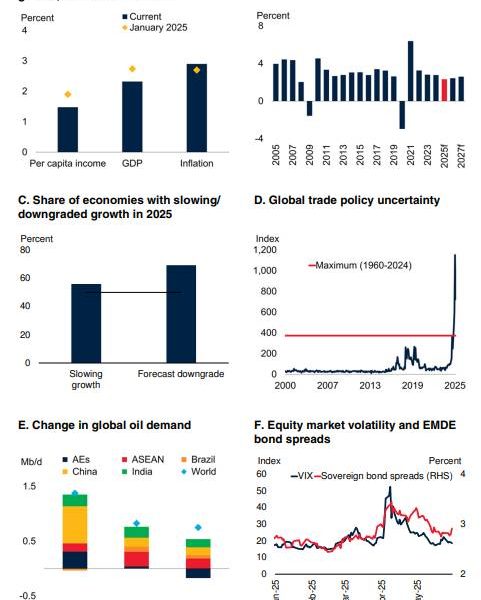

Trade fragmentation fuels slowdown

The most immediate drag comes from a surge in trade barriers, particularly the US-led tariff hikes that triggered retaliatory actions from trading partners, including China. Effective US tariff rates are now at their highest in nearly a century, disrupting supply chains and investor confidence. According to the World Bank, global trade volumes are forecast to grow by just 1.8% in 2025, down sharply from 3.4% in 2024.

Policy uncertainty, exacerbated by abrupt shifts in tariff implementation and retaliatory actions, is stalling both cross-border investment and capital flows. Global FDI into EMDEs, already at less than half its 2008 peak, is expected to remain subdued. World trade policy uncertainty, measured by the Caldara Index, is now at an all-time high.

Commodity exporters face demand slump

Commodity markets are feeling the brunt. Oil prices dropped sharply in April following an OPEC+ decision to raise output and weakening global demand projections. The World Bank now forecasts Brent crude to average $66 per barrel this year, down from $80 in 2024. Commodity exporters in regions such as Sub-Saharan Africa and the Middle East and North Africa (MENA) are facing lower revenues as external debt and fiscal pressures mount.

Even gold, historically a haven, has seen a spike driven not by investor optimism but by risk aversion. Prices are forecast to hit record annual averages, with flows into precious metals fuelled by fears of inflation, geopolitical risk, and financial instability.

Structural drag and policy paralysis in EMDEs

The most alarming trend, however, is structural. Growth in emerging markets and developing economies (EMDEs) is expected to slow to 3.8% in 2025. Many are hampered by weakening investment, deteriorating institutional quality, and fiscal fragility. Fiscal deficits in low-income countries now average nearly 6% of GDP, the highest in this century. Over half are either in or at high risk of debt distress.

The window for easy policy corrections, once open under ultra-low interest rates, is now closed. Policymakers in these economies face the dual challenge of defending currency stability while rebuilding fiscal space. With foreign aid declining, the emphasis must shift to domestic resource mobilisation. The World Bank urges reforms to broaden tax bases, reduce leakages, and reallocate subsidies from blanket schemes to targeted transfers.

Job creation imperative

Demographic shifts are adding further pressure. Sub-Saharan Africa’s working-age population is projected to double by 2050. South Asia is expected to add nearly 300 million workers, while the MENA region is expected to add over 100 million. Without coordinated reforms to enhance labour market flexibility, human capital development, and access to finance, these regions risk severe employment gaps.

According to UN population forecasts, the youth bulge could become a “lost generation” if job creation does not outpace population growth. This has implications not only for national economies but for global stability.

Multilateral action remains critical

The World Bank outlines three urgent global imperatives: de-escalating trade tensions, restoring fiscal discipline, and scaling job creation efforts. It argues that if current trade disputes were resolved with agreements halving current tariffs, global growth could be 0.2 percentage points higher on average in 2025–2026.

Yet, with global cooperation fraying and multilateral mechanisms like the WTO under pressure, policy convergence remains elusive. The longer the impasse persists, the more likely it becomes that trade will fragment along geopolitical blocs, reducing efficiencies and slowing global productivity.

Downside risks dominate

The downside risks outweigh the potential upsides. If trade restrictions escalate further, the report warns of an extended period of anaemic growth. A downside scenario modelled by the World Bank shows global GDP growth falling by 0.5 percentage points in 2025, enough to push some emerging markets and developing economies (EMDEs) into outright recession.

Even under a base-case scenario, many economies will struggle to restore pre-pandemic momentum. The recovery from recent shocks, including the pandemic, war in Ukraine, and climate-linked disasters, remains incomplete while new pressures are accumulating.

The World Bank’s latest forecast underscores a turning point for the global economy. The drivers that powered decades of convergence, liberalised trade, robust investment flows, and institutional reform are in retreat. Reclaiming that progress will require both domestic resolve and renewed international coordination. Without it, a generation of development gains risks being lost.