Saudi Arabia’s residential real estate market is expected to maintain growth momentum despite rising prices and macroeconomic pressures, according to a new report by S&P Global Ratings.

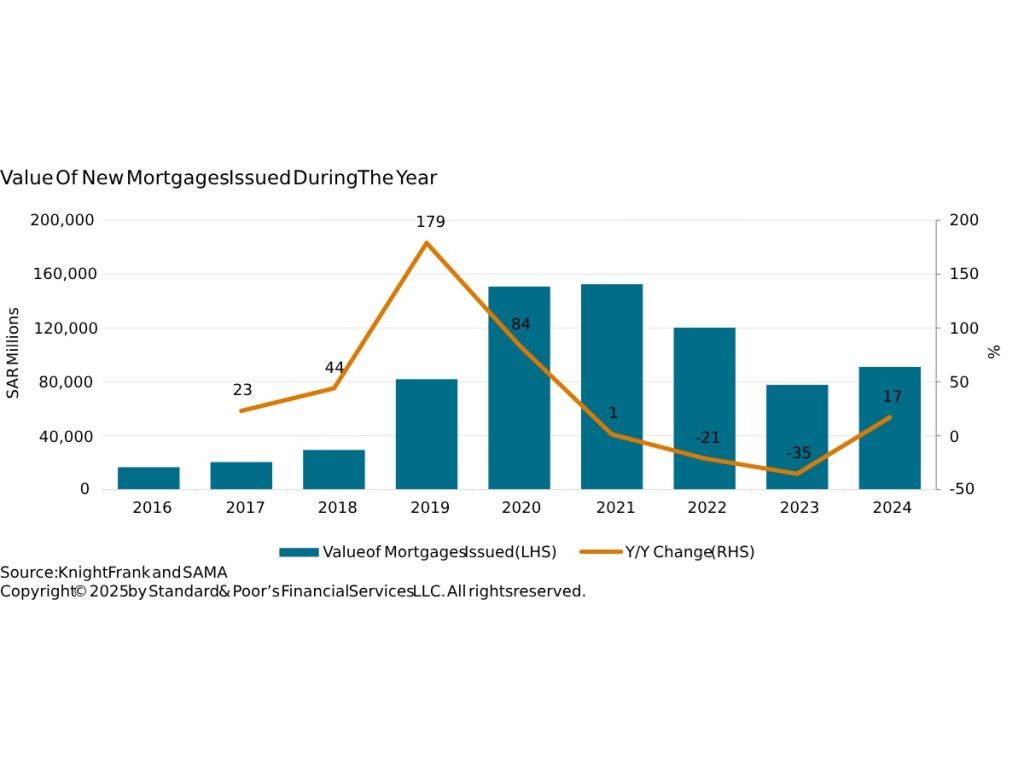

The report highlights a 17% increase in the value of new mortgages issued by Saudi banks in 2024, reaching SAR 91 billion ($24.3 billion), driven by lower interest rates and government support schemes. The Saudi Central Bank cut interest rates by 100 basis points in line with the US Federal Reserve, providing further stimulus for mortgage growth.

S&P attributes the sustained momentum in residential demand to Vision 2030-linked housing targets, population growth, and urban supply shortages. The government-backed Saudi Mortgage Guarantee Services Company (Dhamanat) has played a central role by offering guarantees to low-income nationals, while the rise of off-plan residential developments has expanded access to mortgage financing.

According to the report, mortgages now account for roughly $180 billion, or 23% of the total banking sector loan book, as of the end of 2024. This represents a structural shift from traditional personal and family-based home financing to bank-originated lending. Off-plan mortgages are becoming more common, though S&P warns that this could expose banks to execution risks by developers.

Despite the strong fundamentals, affordability remains a growing concern. Residential prices and rents in Riyadh, Jeddah and other major cities have continued to climb, prompting changes in consumer behaviour. Apartments are becoming more popular as alternatives to villas and townhouses. Buyers are also increasingly opting for off-plan purchases with mortgage plans, reflecting both price sensitivity and evolving preferences.

The government is also working with developers to increase housing stock. Total residential supply across five key cities—Riyadh, Jeddah, Dammam, Mecca, and Madinah—stood at 3.5 million units in 2024. Knight Frank forecasts this number to grow to nearly 3.9 million by 2028. Annual land allocations for affordable housing are expected to support this expansion and help mitigate price pressures.

S&P also noted that the premium residency visa program for foreign investors has yet to contribute meaningfully to demand. Under one visa category, a SAR 4 million minimum investment requirement has limited uptake, though the initiative could gain traction in 2025.

Transaction activity has shown a sharp uptick. Residential transactions surpassed 200,000 in 2024, up 38% year-on-year, while transaction values rose 35% to SAR 164.8 billion. S&P expects this trend to continue into 2025, particularly in Mecca and Madinah due to religious tourism and in Riyadh and Jeddah due to broader economic expansion.

Regulatory reforms introduced in 2024—including escrow account requirements, standardised contracts, and greater transparency—are expected to improve investor confidence and support further market institutionalisation. A new fee on idle land is also anticipated to encourage faster development and reduce speculative hoarding.

While high interest rates and global uncertainty remain risks, S&P maintains a positive outlook on the sector’s trajectory. The agency concludes that rising ownership costs will accelerate structural changes in Saudi Arabia’s residential real estate market, offering long-term opportunities for developers, banks, and institutional investors.